Business structure types explained: A clear guide for UK SMEs

- David Rawlinson

- Mar 30

- 9 min read

Choosing the wrong business structure is one of the most expensive mistakes a UK business owner can make, yet it happens constantly. Pick the wrong setup and you could face unexpected tax bills, personal liability for business debts, or a compliance headache that costs you time and money to untangle. The UK Government outlines four principal structures for small businesses: sole trader, general partnership, limited liability partnership (LLP), and private limited company (Ltd). This guide walks you through each one in plain English, covering what they mean for your taxes, your legal protection, and your day-to-day compliance obligations.

Table of Contents

Key Takeaways

Point | Details |

Choose the right fit | The structure affects your liability, taxes and compliance burden, so fit it to your goals and risk profile. |

Tax efficiency changes | Limited companies become more tax efficient for profits above £30k to £40k compared to sole trader. |

Compliance varies widely | Sole traders have minimal filings, while limited companies and LLPs require more complex accounts and annual returns. |

Switching is possible but complex | You can change structure later, but watch for tax traps and seek advice before making any move. |

What are the main business structure types in the UK?

Before you register anything, it helps to understand the landscape. The UK Government recognises three broad categories for SMEs: sole trader, partnership (general or LLP), and private limited company. Each sits at a different point on the spectrum of simplicity versus protection.

The numbers tell an interesting story. Over 50% of UK businesses are sole traders, yet limited companies account for roughly 75% of formal Companies House registrations. That gap exists because many sole traders never formally register beyond HMRC, while Ltd companies must register by law.

Here is a quick overview of the key characteristics:

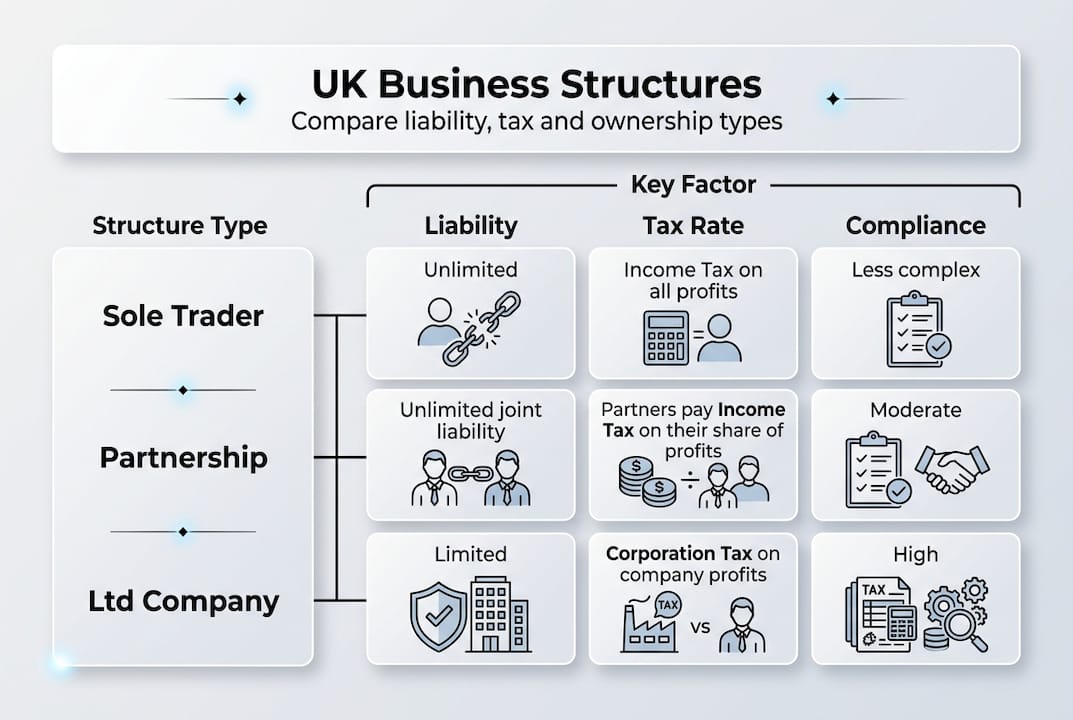

Structure | Legal status | Liability | Tax mechanism |

Sole trader | Not separate from owner | Unlimited personal | Income Tax via Self Assessment |

General partnership | Not separate | Unlimited personal | Income Tax on profit share |

LLP | Separate legal entity | Limited to capital | Income Tax on profit share |

Private Ltd (Ltd) | Separate legal entity | Limited to share capital | Corporation Tax + Income Tax/Dividend Tax |

Key points to keep in mind before diving deeper:

Simplicity favours sole traders and general partnerships.

Protection favours LLPs and Ltd companies.

Tax efficiency at scale generally favours Ltd companies.

Compliance burden increases as you move from sole trader to Ltd.

For a broader look at staying on the right side of HMRC, our UK SME compliance checklist is a useful companion. Understanding corporate finance basics also helps when weighing up growth options.

With a landscape overview in mind, let’s look at each structure individually, starting with the simplest UK option.

Sole trader: Easy start, but personal risk

A sole trader is simply a self-employed individual running a business in their own name. Think of a local plumber, a freelance graphic designer, or a market stall owner. There is no legal separation between you and the business.

The HMRC registration process is straightforward: register for Self Assessment by 5 October after the end of the tax year in which you started trading. Miss that deadline and penalties follow. Once registered, you pay Income Tax on profits at 20%, 40%, or 45% depending on your earnings, plus Class 2 and Class 4 National Insurance contributions.

Here is what the compliance journey looks like for a new sole trader:

Register with HMRC for Self Assessment by 5 October.

Keep records of all income and expenses throughout the year.

Register for VAT if your taxable turnover exceeds £90,000.

Submit your Self Assessment tax return by 31 January each year.

Pay any tax owed by 31 January, with a payment on account due 31 July.

The critical risk is unlimited liability. If your business runs into debt or faces a legal claim, creditors can pursue your personal assets, including your home and savings. That is a serious exposure for anyone operating in a sector with meaningful financial or legal risk.

“The sole trader structure suits those starting out with low overheads, minimal risk, and a desire for full control. But as income and risk grow, the case for incorporation strengthens considerably.”

Our micro-entity bookkeeping tips are particularly relevant here, as good records are your first line of defence at tax time.

Pro Tip: If your annual profits are consistently above £30,000 or you work in a sector with liability exposure (such as construction or consultancy), it is worth modelling the tax and protection benefits of moving to a Ltd company. The saving can be substantial.

After understanding the simplest route, we move to how partnerships open up multi-owner possibilities and variations.

Partnerships: Teamwork options for shared ventures

When two or more people go into business together, a partnership is the natural starting point. But not all partnerships are equal, and the difference matters enormously for your personal risk.

A general partnership means all partners share unlimited liability for the business’s debts. Each partner pays Income Tax on their share of profits via Self Assessment. There is no requirement to register at Companies House, but a nominated partner must register the partnership with HMRC.

An LLP, by contrast, is a separate legal entity registered at Companies House. Partners (called members) have limited liability, meaning their personal assets are generally protected. Tax treatment remains transparent, so each member pays Income Tax on their profit share rather than the partnership paying Corporation Tax.

Here is a side-by-side comparison:

Feature | General partnership | LLP |

Legal entity | No | Yes |

Liability | Unlimited | Limited to capital contributed |

Registration | HMRC only | Companies House + HMRC |

Annual accounts filing | No | Yes (Companies House) |

Tax | Income Tax per partner | Income Tax per member |

Best for | Trusted, low-risk teams | Professional services, higher-risk ventures |

Key considerations for both structures:

A written partnership agreement is strongly advised, even if not legally required.

Without one, the Partnership Act 1890 governs disputes, which may not reflect your intentions.

Profit-sharing ratios, decision-making rights, and exit terms should all be documented.

For a deeper look at the numbers side, our partnership accounting essentials guide covers the bookkeeping and tax filing requirements in detail. If you are weighing up whether an LLP is right for your situation, professional financial advice can help you model the outcomes.

Pro Tip: If your partnership operates in a sector where a single claim could be financially devastating (legal, medical, or financial services, for example), forming an LLP rather than a general partnership could protect your personal assets at relatively low additional cost.

With partnerships covered, the next logical option for many growing ventures is the limited company, which brings limited liability and more formal obligations.

Private limited company (Ltd): Protection and growth benefits

A private limited company is a separate legal entity from its owners. That single fact changes everything. The company can own assets, enter contracts, and incur debts in its own name. If it fails, shareholders generally lose only what they invested, not their personal savings or home.

Setting up a Ltd involves registering at Companies House, appointing at least one director, and issuing shares. The ongoing admin is more demanding than a sole trader setup:

File a confirmation statement at Companies House each year.

Prepare and file annual statutory accounts.

Submit a Corporation Tax return to HMRC.

Run payroll for any directors taking a salary.

File a Self Assessment return if you receive dividends or other income.

On the tax side, the company pays Corporation Tax on its profits: 19% on profits up to £50,000 and 25% on profits over £250,000, with marginal relief in between. Directors typically take a low salary (to minimise National Insurance) and top up with dividends, which are taxed at lower rates than income.

The funding potential is another major advantage. Ltd companies can access SEIS and EIS investment schemes, making them far more attractive to external investors than sole trader or partnership structures.

For a full breakdown of your ongoing obligations, our Ltd company compliance steps guide and annual confirmation statement guide are essential reading.

Now that each option is clear, how do you decide which structure matches your needs best?

Comparing structures: Liability, tax and compliance side by side

Here is where the decision becomes practical. The table below puts all three main structures head to head:

Factor | Sole trader | Partnership/LLP | Private Ltd |

Personal liability | Unlimited | Unlimited (GP) / Limited (LLP) | Limited |

Tax on profits | Income Tax 20-45% | Income Tax 20-45% | Corporation Tax 19-25% |

NI contributions | Class 2 + 4 | Class 2 + 4 per partner | Employer/Employee NI on salary |

Companies House filing | No | LLP only | Yes |

Annual accounts | No | LLP only | Yes |

Setup cost | Minimal | Low to moderate | Moderate |

Investor-ready | No | Rarely | Yes |

The profit threshold question is one we get asked constantly. Tax efficiency generally tips in favour of a Ltd company once profits exceed roughly £30,000 to £50,000, because the combination of Corporation Tax and dividend extraction beats the Income Tax rates a sole trader pays at higher earnings.

Compliance is the other side of the coin. Sole traders face the lightest burden: one Self Assessment return per year. Ltd companies and LLPs must file at Companies House, prepare statutory accounts, and submit Corporation Tax returns, which is why most directors work with an accountant.

“The right structure is not always the most tax-efficient one on paper. It is the one that fits your risk appetite, your growth plans, and your capacity to manage compliance.”

Useful next steps once you have made your decision:

Use our SME accounting checklist to confirm you have covered every compliance base.

Review our guide on setting up business finances to get your accounts in order from day one.

Before wrapping up, it is vital to address changing structures and how all this fits with long-term planning.

Changing your structure and special cases

Switching structures is possible, but it is rarely as simple as ticking a box. There are real tax consequences to consider, and getting it wrong can be costly.

Here is what to think through before making a change:

Sole trader to Ltd: You may need to transfer assets into the company, which can trigger Capital Gains Tax (CGT) if those assets have increased in value.

Ltd to sole trader (disincorporation): This is complex and often expensive. HMRC may treat asset transfers as disposals, creating a tax charge.

General partnership to LLP: Requires registration at Companies House and a formal members’ agreement.

Non-residents: Non-residents can form a UK Ltd or LLP, but face additional compliance requirements around tax residency and reporting.

Special cases worth noting include Community Interest Companies (CICs), which are designed for social enterprises and carry their own regulatory framework. High-risk ventures, such as those in construction or financial services, almost always benefit from Ltd or LLP status for liability protection.

Pro Tip: Before changing your structure, ask your accountant to model the full tax impact, including CGT on asset transfers, the cost of winding down the old entity, and the ongoing compliance costs of the new one. The numbers sometimes surprise people.

Our guide on the importance of tax compliance is a good reference point if you are navigating a structural change and want to stay on the right side of HMRC.

Expert help for choosing and setting up your structure

Getting your business structure right from the start saves you money, reduces risk, and means far less paperwork further down the line. But the decision involves tax modelling, liability assessment, and compliance planning that can be genuinely complex.

At Concorde Company Solutions, we work with sole traders, partnerships, and limited companies across the UK, helping them choose the right structure, handle their compliance obligations, and keep their finances in order. Whether you need support with UK payroll solutions, statutory accounts, or a full review of your current setup, we are here to help. Visit Concorde Company Solutions to find out how we can support your business from day one and beyond.

Frequently asked questions

What is the simplest business structure in the UK?

The sole trader setup is the simplest, requiring only HMRC registration for Self Assessment with minimal ongoing admin, though it comes with full personal liability for all business debts.

How is tax paid by a limited company and its owners?

A limited company pays Corporation Tax on its profits, while directors pay Income Tax and National Insurance on any salary they draw, plus Dividend Tax on any dividends received from the company.

Are there tax advantages to changing from sole trader to Ltd?

Yes, tax efficiency improves significantly once profits exceed £30,000 to £40,000, as limited companies benefit from lower Corporation Tax rates and the option to extract profits as dividends rather than salary.

Can non-residents form a limited company in the UK?

Non-residents can form a UK Ltd or LLP, but they should seek specialist advice to navigate the additional compliance and tax residency rules that apply to overseas directors and members.

Recommended

Comments