Partnership Accounting – Key Facts for UK Businesses

- David Rawlinson

- Jan 26

- 11 min read

Running a business with a partner in Garforth means more than just sharing ambitions—it means sharing legal responsibility and financial decisions that carry real consequences. For small business owners and sole traders, partnership accounting defines how profits, liabilities, and tax duties are managed, shaping both trust and compliance. This guide breaks down the fundamental principles of partnership accounting, explaining what makes it different from running a limited company and offering practical steps to keep every partner protected and your books HMRC-ready.

Table of Contents

Key Takeaways

Point | Details |

Understanding Partnership Accounting | Accurate financial records and compliance with tax regulations are essential for partnerships to avoid disputes and ensure smooth operations. |

Choosing the Right Partnership Type | Selecting the appropriate partnership structure affects liability, tax obligations, and accounting complexities, so it requires careful consideration. |

Maintaining Accurate Partner Accounts | Implementing separate capital and current accounts for each partner is vital for transparency and to prevent disputes related to profit sharing. |

Compliance with Legal Framework | Familiarity with the Partnership Act 1890 and tax obligations is crucial to protect both partners and the business from potential liabilities. |

What Is Partnership Accounting in the UK?

Partnership accounting sits at the heart of how many small businesses in Garforth and across the UK manage their finances. At its core, partnership accounting involves managing finances for unincorporated businesses where two or more people run a business together with the intention to make a profit. Unlike a limited company, a partnership is treated as a separate entity for reporting purposes, but it retains a fundamentally different legal structure that affects everything from taxation to liability.

What makes partnership accounting distinct is how it handles the distribution of profits and the partners’ financial interests. Each partner contributes capital, shares in profits according to their agreement, and holds unlimited liability for the business’s debts. The partnership agreement acts as the rulebook here, spelling out exactly how profits get divided, what each partner contributes, and what happens if someone wants to leave. Whilst a formal partnership agreement isn’t legally mandatory, operating without one is like running a business with no insurance. It creates unnecessary risk and confusion. When you set up your accounting records, you’ll need to track profit sharing ratios and appropriations of profit separately from the actual profit for the year. This distinction matters because it affects how money flows to each partner’s capital account and how HMRC views your tax position.

For small business owners in your position, understanding partnership accounting means grasping two fundamental responsibilities. First, you need accurate financial records that reflect your business’s true position, showing income, expenses, and crucially, how profits are allocated between partners. Second, you need to file partnership tax returns with HMRC, which requires detailed schedules showing each partner’s share of profits and their tax obligations. This is where having proper accounting structures becomes essential. Many sole traders exploring partnerships or existing partners reviewing their arrangement find that professional accountants for SMEs can simplify these obligations significantly, ensuring your records remain compliant and your partnership operates smoothly.

Pro tip: Create a formal partnership agreement from the outset, even if you’re just starting out with a friend or colleague, and keep your accounting records meticulously organised with separate partner capital accounts to avoid disputes down the line.

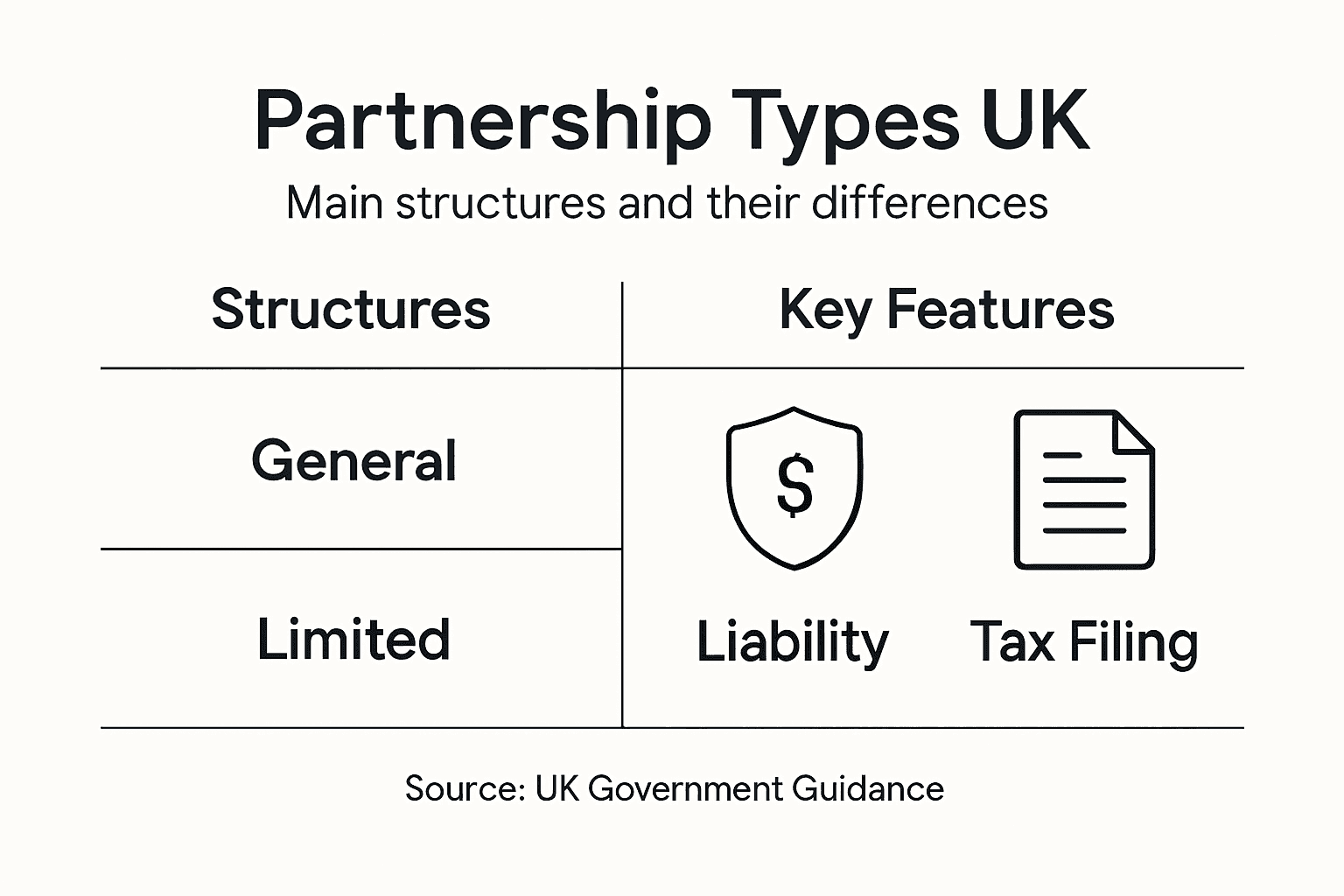

Types of Partnerships and Key Differences

Not all partnerships are created equal. The type of partnership you establish fundamentally shapes how you operate, what liability you face, and how your accounting records need to be structured. In the UK, partnerships are governed by the Partnership Act 1890, which sets out the legal framework for how partnerships function. Understanding the differences between partnership types is crucial before you commit to a structure, especially when it comes to personal liability and how profits get reported to HMRC.

The main partnership types you’ll encounter are general partnerships and limited partnerships, each with distinct characteristics that affect your accounting and personal risk. A general partnership is the most common setup, where all partners share management responsibilities and carry unlimited personal liability for the business’s debts and obligations. This means if the partnership faces financial trouble, creditors can pursue your personal assets. In contrast, a limited partnership includes both general partners who have unlimited liability and limited partners who only risk their investment amount. Limited partners cannot take part in day to day management, but their personal assets remain protected. Then there’s the Limited Liability Partnership (LLP), a hybrid structure that combines limited liability protection with partnership flexibility, allowing all partners to enjoy limited liability whilst maintaining management control. For most small business owners in Garforth exploring partnerships, understanding your liability exposure is the first critical decision.

Each structure has different accounting implications that ripple through your financial records and tax filings. General partnerships report all partners’ shares of profit and loss on individual tax returns, whilst limited partnerships require additional schedules tracking limited partners separately. LLPs file corporation tax returns and must maintain more formal accounting records similar to companies. The Partnership Act 1890 provides the baseline rules, but your partnership agreement can modify these, affecting how profits are allocated, how decisions are made, and what happens when partners join or leave. Changes in partnership such as admitting new partners or managing partner retirement require adjustments to your accounting records and potentially your profit sharing ratios. Getting this structure right from the start saves considerable headache later.

Here is a concise comparison of partnership types and their key accounting implications:

Partnership Type | Liability Structure | Tax Filing Requirement | Accounting Complexity |

General Partnership | Unlimited for all partners | Individual tax returns | Moderate, separate accounts |

Limited Partnership | General: unlimited; Limited: capped | Additional schedules for partners | Higher, due to role split |

Limited Liability Partnership (LLP) | Limited for all partners | Corporation tax return | Most complex, like companies |

Pro tip: Choose your partnership type based on liability protection needs and long term growth plans, then document everything in a detailed partnership agreement that covers profit sharing, partner contributions, and procedures for admitting or removing partners.

Profit Sharing and Partner Accounts Explained

Profit sharing sits at the financial heart of any partnership. It’s the mechanism that determines how much money each partner actually takes home, and getting it wrong creates tension fast. Profit sharing is based on the profit or loss sharing ratio detailed in your partnership agreement, but the actual calculation involves several layers. Before profits are distributed to partners, the partnership typically makes appropriations like interest on capital, partner salaries, or bonuses. Only the residual profit after these appropriations are deducted gets divided among partners according to their agreed ratio. This distinction matters enormously because it affects how much each partner receives and how your accounting records reflect their individual financial positions.

Understanding partner accounts is essential for accurate financial tracking. Your partnership maintains three key account types for each partner. Capital accounts record the initial investment each partner puts into the business, which typically remains relatively static unless there’s a major change in partnership structure. Current accounts are where the action happens: they track your day to day transactions with the partnership, including drawings (money you take out), salary allocations, interest on capital, and your share of profits. Appropriation accounts sit between net profit and partner distributions, showing exactly how profits get adjusted before they reach individual partners. For example, if your partnership agreement says partners get 5% interest on their capital balances before profit sharing, that interest gets recorded in the appropriation account, reducing the amount available for distribution according to profit sharing ratios. This transparent tracking ensures every partner sees exactly how their account balance changed from period to period.

Many small business partnerships fail to maintain separate current accounts for each partner, which creates nightmares during disputes or when partners leave. When you don’t track these accounts properly, you lose the audit trail showing who drew what, who earned how much in salary, and whose profit share calculation was correct. Capital accounts track investments while current accounts record drawings, salaries, and interest, meaning you need both running simultaneously to maintain transparency. If your partnership changes, such as admitting a new partner or revaluing assets, these adjustments also flow through the accounts, sometimes affecting historical capital account balances. The complexity scales quickly, which is why many partnerships in Garforth benefit from professional bookkeeping support to ensure accuracy and compliance with partner agreements.

Below is a summary showing the roles of partner accounts in UK partnerships:

Account Type | Main Purpose | Example Entry |

Capital Account | Records partner investments | Initial cash or asset deposits |

Current Account | Tracks ongoing partner activity | Salaries, drawings, profit share |

Appropriation Account | Allocates adjustments before profit sharing | Interest on capital, bonuses |

Pro tip: Set up separate current and capital accounts for each partner from day one, document your exact profit sharing ratio and any appropriations in writing, and reconcile these accounts quarterly to catch errors early before they snowball into disputes.

Legal Framework and Tax Compliance Essentials

Your partnership doesn’t operate in a legal vacuum. The moment you form a partnership, you’re bound by specific legal requirements and tax obligations that govern how you conduct business, report finances, and handle liability. UK partnership accounting must comply with the Partnership Act 1890 and applicable accounting standards, which establish the foundational rules for how partnerships function. These aren’t optional guidelines. They’re the legal bedrock that protects both your partnership and your creditors. The Partnership Act 1890 remains remarkably relevant today, setting out rights and duties of partners, profit sharing rules, and procedures for dissolution. Beyond this century old legislation, your partnership must also comply with modern accounting standards and HMRC requirements that have evolved significantly. Understanding these layers of compliance prevents costly mistakes and protects your business from regulatory scrutiny.

Tax compliance is where the rubber meets the road for most partnerships. Your partnership itself must submit a Self Assessment tax return to HMRC, reporting the partnership’s total profit or loss for the tax year. However, this isn’t where the tax obligation ends. Each partner must also report their individual share of partnership income on their personal Self Assessment tax return, paying income tax and National Insurance contributions on their share of profits. This dual reporting system means you need meticulous records showing exactly how much profit each partner earned, what salary or interest they received, and what drawings they took. When your partnership records profit sharing and appropriations incorrectly, the discrepancy between partnership records and personal tax filings creates problems with HMRC. The tax authorities closely scrutinise partnership returns because profit shifting and income manipulation sometimes occur across partnership structures. Getting this right requires accurate partner accounts and clear documentation of your profit sharing agreement.

Personal liability for partnership debts is the element that keeps many business owners awake at night. In a general partnership, partners are personally liable for debts if the partnership cannot meet obligations, meaning creditors can pursue your personal assets if the partnership fails financially. This joint and several liability extends to all partners, even if only one partner incurred the debt. Changes in partnership composition also trigger legal and accounting requirements. When a new partner joins, the partnership agreement typically needs updating, profit sharing ratios may change, and accounting adjustments for goodwill or asset revaluation often follow. When a partner retires, similar complications arise around their capital account settlement and how remaining partners absorb their profit share. Each of these transitions requires careful documentation and often professional guidance to ensure compliance with both partnership law and tax requirements. Why file tax returns carefully matters for partnerships because inaccurate filings expose all partners to personal liability and penalties.

Pro tip: Maintain a written partnership agreement compliant with the Partnership Act 1890, keep separate partner accounts with quarterly reconciliations, and file your partnership tax return on time each year with supporting documentation showing each partner’s share of profit, salary, and interest calculations.

Common Pitfalls and How to Avoid Them

Partnership accounting trips up even experienced business owners because the rules seem straightforward until you actually apply them. The most dangerous mistakes happen quietly, buried in spreadsheets where nobody notices until tax time arrives or a partner dispute erupts. One of the biggest pitfalls is misunderstanding how profit sharing actually works. Partners often assume their profit sharing ratio applies directly to the net profit figure shown in the profit and loss statement, but that’s incorrect. Profit sharing rules require applying the ratio only to residual profit after all appropriations have been deducted. This means partner salaries, interest on capital, and bonuses come out first, reducing the pool available for distribution. If you skip this step and distribute based on the raw profit figure, you’re either overpaying some partners or underpaying others, and you’ve created an accounting error that cascades through your records.

Another frequent mistake is inconsistent handling of appropriations across accounting periods. Your partnership agreement specifies which appropriations apply and when. Perhaps partners receive 4% interest on their capital balance, or maybe certain partners draw a fixed salary. If you calculate these correctly in year one but forget them in year two, your partner accounts become inconsistent and your records lose credibility. When disputes arise, HMRC scrutinises these calculations closely because inconsistency suggests either carelessness or intentional manipulation. The fix is straightforward: create a standard appropriation schedule that documents exactly what each partner receives outside of profit sharing, then apply it consistently every period. Write it down. Reference it in your partnership agreement. Stick to it. This removes ambiguity and prevents arguments later.

Ignoring adjustments for partnership changes creates perhaps the most expensive pitfall. When partners join or leave, when you revalue assets, or when goodwill emerges, these events require accounting adjustments that affect partner capital accounts and sometimes profit sharing ratios. Many partnerships pretend these changes don’t require accounting entries, which distorts each partner’s true equity position. For example, if a new partner invests capital at a time when the partnership’s assets are worth more than their book value, the existing partners’ goodwill needs accounting treatment. Failing to record this means the new partner’s equity calculation is wrong from day one. Similarly, when a partner retires and takes their capital balance in cash, you need to carefully track which assets get sold to fund that withdrawal and how the loss or gain affects remaining partners. These transitions need careful documentation and often professional guidance to handle correctly. Failure to comply with appropriation principles may lead to misstatement of partners’ accounts and disputes that damage working relationships.

Pro tip: Create a written appropriation schedule showing each partner’s salary, interest rate, and profit sharing ratio, then review it annually before year end to catch any partnership changes that require accounting adjustments, and document every change in writing with partner agreement.

Simplify Your Partnership Accounting with Expert Support

Navigating the complexities of partnership accounting in the UK can be challenging, especially when managing partner accounts, profit sharing ratios or compliance with the Partnership Act 1890. If you are struggling to keep accurate financial records, ensure timely tax filings or avoid disputes over profit distribution, you are not alone. Clear documentation, precise partner account management, and compliance with HMRC rules are crucial to protect your business and personal assets.

Take control of your partnership finances today by partnering with professionals who truly understand your unique needs. At Concorde Company Solutions based in Garforth, Leeds, we specialise in bookkeeping services and company tax returns tailored for small to medium-sized businesses and partnerships. Our transparent pricing and personalised support empower you to maintain accurate accounts, meet all regulatory responsibilities, and focus on growing your business. Don’t wait for tax season or a partner dispute to highlight accounting gaps—visit our website now and get the expert guidance your UK partnership deserves.

Frequently Asked Questions

What is partnership accounting?

Partnership accounting is the management of financial records for unincorporated businesses where two or more individuals operate a business for profit. It outlines how profits, liabilities, and financial responsibilities are shared among partners.

What types of partnerships exist?

The main types of partnerships include general partnerships, limited partnerships, and limited liability partnerships (LLPs). Each has distinct legal and financial implications, particularly concerning liability and profit sharing.

How are profits distributed in a partnership?

Profits in a partnership are shared based on the profit-sharing ratio specified in the partnership agreement. Before distribution, appropriations such as partner salaries and interest on capital are deducted from the total profits.

What are the key responsibilities for partnership tax compliance?

Partnerships must submit a Self Assessment tax return to HMRC, reporting the total profit or loss for the year. Additionally, each partner must declare their share of the partnership’s income on their personal tax returns to ensure accurate tax payments.

Recommended

Informative article with clear points explained. I’ve been reading similar posts on Companies999 while comparing accountants birmingham and this adds good value.