UK payroll legislation: 15% NIC rise compliance guide

- David Rawlinson

- 12 hours ago

- 10 min read

Many UK business owners believe payroll legislation is too complex to manage without costly consultants. The truth is that understanding the core obligations around PAYE, National Insurance, minimum wage, and statutory payments can demystify compliance. Recent 2026 changes, including the employer NIC rate increase to 15% and new thresholds, make it essential for financial decision-makers to grasp these rules. This guide clarifies key elements and practical steps for effective payroll management and compliance.

Table of Contents

Key Takeaways

Point | Details |

PAYE registration | Employers must register with HMRC before the first payday. |

RTI submissions | Real Time Information submissions to HMRC are mandatory on every payday. |

Record keeping three years | Payroll records must be kept for at least three years. |

NIC rate rise 2026 | In 2026 the employer NIC rate rose to fifteen percent along with new thresholds. |

Payroll software benefits | Payroll software helps reduce administrative burden and supports compliance. |

Overview of UK payroll legislation

Payroll legislation in the UK comprises multiple statutes governing employer obligations for PAYE, National Insurance, minimum wage, pensions, statutory payments, and record keeping. This framework has evolved through decades of employment law, with key regulations including the Income Tax (PAYE) Regulations 2003 and Social Security Contributions Regulations 2001. HM Revenue & Customs (HMRC) administers most payroll obligations and enforces compliance through audits, penalties, and guidance.

Employers face five core duties under this legislative framework:

Registering as an employer with HMRC before the first payday

Calculating and deducting income tax and National Insurance contributions correctly

Reporting payroll information through Real Time Information submissions

Paying deducted amounts to HMRC by statutory deadlines

Maintaining comprehensive payroll records for inspection and employee queries

The complexity arises because these obligations intersect with multiple areas of employment law. For instance, payroll management for UK businesses requires coordinating tax deductions with pension auto-enrolment, statutory sick pay calculations, and minimum wage compliance. Each element has distinct rules, thresholds, and reporting requirements that change annually.

“Payroll legislation represents one of the most administratively demanding aspects of running a UK business, requiring continuous attention to regulatory updates and precise calculation methods.”

The HMRC employer PAYE guide provides detailed technical specifications for each obligation. Business owners must understand that compliance is not optional. Failing to meet these duties triggers automatic penalties, interest charges on late payments, and potential criminal prosecution in cases of deliberate fraud. The legislation protects both employees and the public revenue system by ensuring consistent, transparent wage treatment across all UK employers.

Small business owners often underestimate the time investment required for proper payroll administration. Even with just a handful of employees, the monthly cycle of calculations, submissions, and payments demands systematic processes. Larger organisations face additional complexity around benefits administration, company car taxation, and employee share schemes. Understanding the legislative foundation helps business owners recognise which tasks require professional support and which they can manage internally with appropriate tools.

Core payroll process and employer obligations

Core mechanics involve registering as an employer, calculating gross pay deductions via PAYE (Income Tax at 20 to 45%, NICs), RTI submissions via FPS on or before payday, payments to HMRC by 22nd next month, and maintaining 3 year records. This seven step workflow forms the backbone of compliant payroll operations:

Employer registration: Apply for PAYE scheme with HMRC before first employee payment, receiving unique reference numbers

Employee onboarding: Collect P45 forms or starter checklist information, verify National Insurance numbers, assess tax codes

Gross pay calculation: Determine wages including overtime, bonuses, and benefits, then calculate deductions

Real Time Information submission: File Full Payment Submission (FPS) to HMRC on or before each payday with employee payment details

HMRC payment: Transfer deducted tax and NIC to HMRC by 22nd of following month (19th for cheque payments)

Statutory payments management: Process SSP, SMP, SPP, and other statutory payments, reclaiming eligible amounts

Record maintenance: Keep comprehensive payroll records for minimum three years covering all calculations and submissions

PAYE deducts income tax at progressive rates depending on earnings bands. The basic rate of 20% applies to income between £12,571 and £50,270, the higher rate of 40% covers £50,271 to £125,140, and the additional rate of 45% applies above £125,140. These thresholds interact with personal allowances and tax code adjustments that reflect individual circumstances.

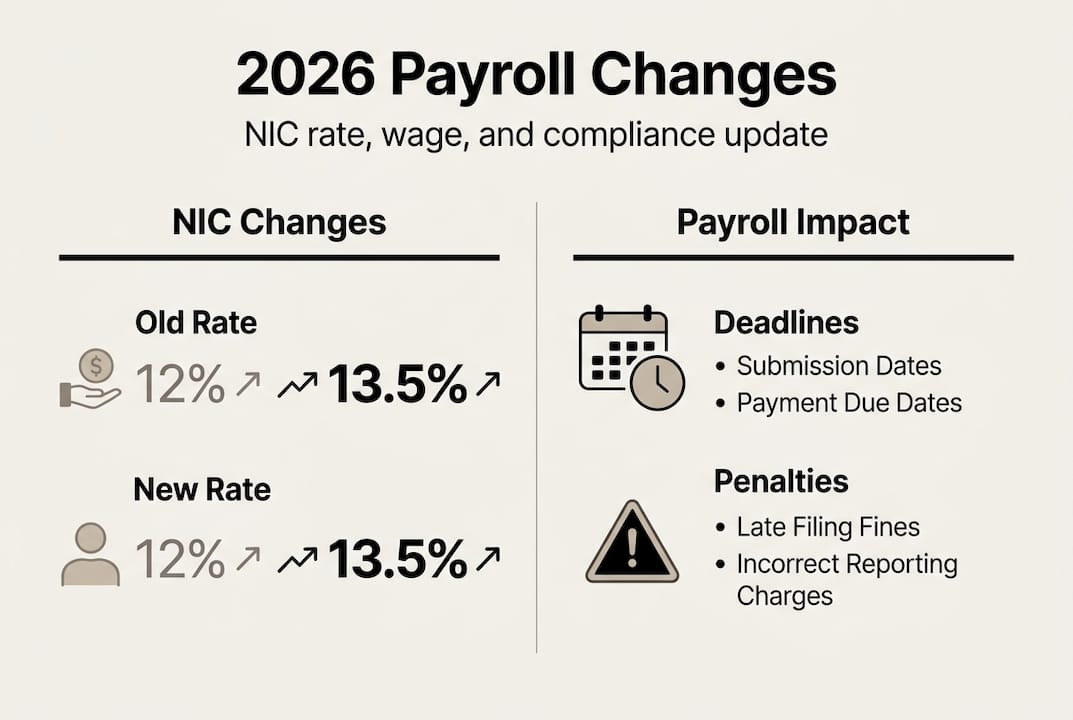

National Insurance contributions represent the second major deduction. Employees pay Class 1 NICs at 12% on earnings between £242 and £967 weekly (2026 rates), then 2% on amounts above. Employers pay separate Class 1 contributions at approximately 15% on earnings above £5,000 annually per employee under 2026 rules. This employer NIC represents a significant cost that many business owners overlook when budgeting for new hires.

The payroll processing workflow for UK compliance emphasises timeliness in RTI submissions. HMRC expects FPS data on or before the payment date for each pay period. Late submissions trigger automatic penalties starting at £100 per month for small employers, scaling up based on employee numbers. These penalties accumulate quickly, making prompt filing essential.

Payments to HMRC must clear by the 22nd of the month following the tax month. For example, April payroll deductions must reach HMRC by 22nd May. Electronic payments require three working days for processing, so employers should initiate transfers by 19th to ensure timely receipt. The payroll management checklist for essential UK steps helps track these deadlines systematically.

Employers must retain payroll records for at least three years from the end of the tax year they relate to. These records include gross pay calculations, tax and NIC deductions, FPS submissions, payment dates, and employee details. HMRC can request these records during compliance checks, and missing documentation results in penalties and potential tax assessments based on estimates.

Pro tip: Use payroll software to automate RTI submissions and calculations to reduce errors and stay compliant. Modern systems integrate with HMRC systems, calculate deductions automatically, and generate required reports with minimal manual intervention.

2026 payroll legislation updates and edge cases

Key 2026 changes include employer NIC rate increase to 15% with a £5,000 threshold, increases in NMW/NLW rates (e.g., £11.44 per hour for age 21 plus), SSP payable from day 1, holiday pay accrual at 12.07% for irregular hours, and mandatory payrolling of benefits. These updates significantly impact payroll costs and administrative processes for UK businesses.

The employer National Insurance contribution increase from 13.8% to 15% represents one of the most substantial cost changes in recent years. Simultaneously, the secondary threshold dropped from £9,100 to £5,000 annually, meaning employers now pay NIC on lower earnings. For a business with ten employees each earning £30,000, this change adds approximately £3,000 to annual employment costs. Financial planning must account for this increased burden when budgeting for staffing.

National Minimum Wage and National Living Wage rates increased across all age bands:

Age group | Previous rate | 2026 rate | Increase |

21 and over (NLW) | £11.00 | £11.44 | £0.44 |

18 to 20 | £8.60 | £9.00 | £0.40 |

Under 18 | £6.40 | £6.75 | £0.35 |

Apprentice | £6.40 | £6.75 | £0.35 |

These increases require immediate payroll adjustments to avoid underpayment penalties. HMRC conducts regular minimum wage enforcement, and violations result in arrears payments, financial penalties up to 200% of underpayment, and potential public naming of non-compliant employers.

Statutory Sick Pay (SSP) now begins from day one of absence rather than day four under previous rules. This change increases employer costs for short-term sickness, particularly in industries with frequent brief absences. The weekly SSP rate for 2026 is £116.75, payable for up to 28 weeks. Employers with annual NIC liabilities below £45,000 can reclaim SSP through the Statutory Payment Recovery scheme.

Holiday pay for workers with irregular or variable hours shifted to a 12.07% accrual method. This percentage represents 5.6 weeks of holiday divided by 46.4 working weeks, providing a consistent calculation method. Rolling up holiday pay (paying it with regular wages rather than separately during leave) is now explicitly permitted, simplifying administration for casual and zero-hours workers. The payroll management tips for UK business owners explains implementation strategies.

Payrolling benefits became mandatory from April 2026, ending the previous P11D paper reporting option. Employers must now report benefits like company cars, medical insurance, and gym memberships through payroll software in real time. This change aligns benefit taxation with regular pay, spreading tax liability across the year rather than creating large bills when P11D forms are processed.

Edge cases require careful attention:

Accidental overpayments can be recovered under Employment Rights Act 1996, section 14(1), but employers must act promptly and communicate clearly

Off-payroll working rules (IR35) require CEST tool assessments for contractors to determine employment status

Directors’ NIC calculations use annual earnings periods regardless of payment frequency

Employees working abroad may trigger complex tax residence and social security coordination issues

Pro tip: Understanding these updates helps avoid common pitfalls in holiday pay and NIC accounting. Regular training for payroll staff ensures changes are implemented correctly from their effective dates.

The UK low pay commission 2025 report provides detailed analysis of minimum wage impacts and future trajectory. Business owners should monitor these reports to anticipate future cost increases and adjust pricing or efficiency strategies accordingly.

Practical guide to managing payroll compliance

Employers find the compliance burden high due to continuous administrative demands like RTI and CEST, but payroll software and strategic processes mitigate these challenges. Effective compliance management requires combining technology, training, and systematic procedures to handle the complexity of UK payroll legislation.

Dedicated payroll software automates the most error-prone tasks. Modern systems integrate directly with HMRC’s RTI gateway, submitting FPS data electronically and receiving instant confirmation. They calculate tax and NIC automatically based on current rates and thresholds, eliminating manual arithmetic errors. Software also generates reports for management review, tracks statutory payment entitlements, and maintains the required audit trail. Cloud-based solutions offer additional benefits like automatic updates for legislative changes and remote access for business owners.

Best practices for payroll compliance include:

Conducting regular staff training on legislative updates and system changes

Implementing double-check procedures for statutory pay calculations before processing

Maintaining clear employee classification records to support employment status decisions

Scheduling payroll tasks well in advance of deadlines to allow time for corrections

Keeping comprehensive documentation of all decisions and calculations

Establishing clear communication channels for employee payroll queries

Employee classification represents a critical compliance area. Misclassifying workers as self-employed when they meet employment tests triggers back-dated PAYE and NIC liabilities, plus penalties. The CEST (Check Employment Status for Tax) tool provides HMRC’s assessment framework, but business owners should understand the underlying principles of control, substitution, and mutuality of obligation that determine employment status.

Accurate record-keeping extends beyond the minimum three-year legal requirement for many businesses. Retaining records for six years aligns with general accounting standards and provides protection against extended HMRC enquiries. Digital record-keeping offers advantages in searchability, backup security, and space efficiency compared to paper systems.

Pro tip: Outsourcing or using payroll services can further reduce risks and workload for SME owners. Professional payroll providers maintain expertise in current legislation, invest in robust systems, and carry professional indemnity insurance covering compliance errors. The role of payroll services in the UK explores these benefits in detail.

Effective communication with employees about pay and deductions minimises disputes and improves trust. Payslips must clearly show gross pay, all deductions with descriptions, and net pay. Providing explanatory notes about tax code changes, NIC calculations, or pension contributions helps employees understand their pay. Establishing a clear process for payroll queries ensures issues are resolved quickly before they escalate.

“Proactive compliance management transforms payroll from a source of anxiety into a routine administrative function that supports business growth and employee satisfaction.”

The streamline payroll for UK SMBs in 2026 guide offers specific strategies for small businesses with limited administrative resources. These include batching payroll tasks, using templates for common scenarios, and establishing monthly compliance checklists that ensure nothing is overlooked.

Regular compliance reviews help identify potential issues before they become problems. Quarterly internal audits should verify that RTI submissions match payment records, HMRC payments have cleared correctly, statutory payment calculations follow current rates, and employee records remain current. These reviews take minimal time but provide significant protection against accumulating errors.

The payroll compliance challenges analysis highlights that businesses investing in proper systems and training experience fewer HMRC enquiries and penalties. This investment pays for itself through avoided fines, reduced stress, and improved employee relations.

How Concorde Company Solutions can support your payroll needs

Navigating the complexities of UK payroll legislation requires expertise, time, and robust systems that many business owners struggle to maintain alongside their core operations. Concorde Company Solutions offers specialised payroll services tailored to UK SMEs, ensuring compliance with current legislation whilst reducing your administrative burden.

Our payroll services handle PAYE calculations, National Insurance contributions, Real Time Information submissions, and statutory payment management with precision. We stay current with legislative changes like the 2026 NIC increases and minimum wage adjustments, implementing updates immediately so you never fall behind. Our team manages the entire payroll cycle from calculation through to HMRC payment, maintaining the comprehensive records required for compliance.

For businesses seeking to streamline payroll for SMBs, our solutions integrate with your existing accounting systems and provide transparent reporting. You maintain full visibility whilst we handle the technical complexity. Our payroll services for SMEs are designed to scale with your business, supporting growth without increasing your administrative workload. Contact us to discuss how we can simplify your payroll compliance and free your time for strategic business development.

Frequently asked questions

What is payroll legislation in the UK?

Payroll legislation is the set of laws governing how employers must deduct taxes, pay National Insurance, comply with minimum wage requirements, and handle employee wages. These rules are enforced by HMRC and cover registration, calculation, reporting, payment, and record-keeping obligations.

What does RTI filing mean for employers?

RTI filing means submitting payroll data to HMRC every pay cycle through Full Payment Submission reports on or before payday. This real-time reporting maintains transparency and allows HMRC to track tax and NIC collections accurately throughout the year.

What are the current National Minimum Wage rates?

Employers must pay the National Minimum Wage and National Living Wage, which change yearly based on government reviews. For 2026, the National Living Wage for workers aged 21 and over is £11.44 per hour, with lower rates for younger workers and apprentices.

What statutory payments must employers provide?

Statutory payments include Statutory Sick Pay (£116.75 weekly from day one of absence), Statutory Maternity Pay, Statutory Paternity Pay, Statutory Adoption Pay, and Statutory Parental Bereavement Pay. These are legally mandated minimum payments for qualifying employees during specific circumstances.

How long must employers keep payroll records?

Payroll record-keeping for at least three years is legally required to support HMRC audits and employee queries. Records must include gross pay calculations, tax and NIC deductions, RTI submissions, payment dates, and comprehensive employee details for all processed payroll periods.

Recommended

Comments