Cash basis accounting: a practical guide for UK owners

- David Rawlinson

- Apr 17

- 8 min read

TL;DR:

Cash basis accounting records income and expenses only when cash moves, simplifying bookkeeping.

It is now broadly available to unincorporated UK businesses with improved rules since 2024/25.

While easier and better aligned with cash flow, it can obscure true liabilities and isn’t suitable for limited companies.

Most business owners assume cash basis accounting is simply the ‘easy option’ for people who don’t want to deal with complex bookkeeping. That assumption misses something important. With 47–82% of UK SMEs reporting cash flow difficulties, and HMRC having overhauled the rules from 2024/25 onwards, cash basis accounting has become a genuinely strategic choice, not just a shortcut. This guide cuts through the confusion, explains what the method actually means, and helps you decide whether it fits your business, your payment cycles, and your compliance obligations.

Table of Contents

Key Takeaways

Point | Details |

Cash basis defined | Cash basis records income and outgoings when money is received or paid, not when invoiced. |

Recent HMRC rule changes | Since 2024, bigger deductions and loss offset options make cash basis more valuable for SMEs. |

Know your cash flow | Choosing the right accounting method should be driven by your real-world cash movement and compliance needs. |

Switching requires care | Transitioning from accruals needs special adjustments and extra attention to accuracy. |

What is cash basis accounting?

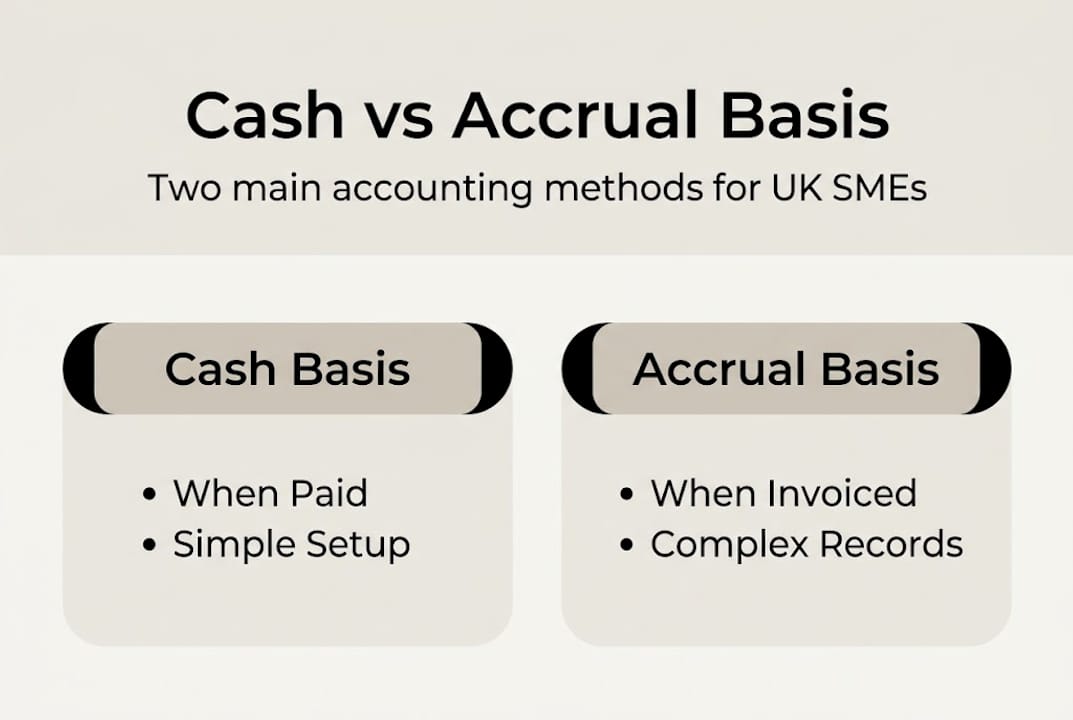

Cash basis accounting records income when money lands in your bank account and expenses when you actually pay them. That’s it. You don’t record anything when you raise an invoice or receive a bill. The transaction only exists, for tax purposes, when cash moves.

This is fundamentally different from accrual accounting explained, where income is recognised when it is earned and expenses when they are incurred, regardless of when payment arrives. Accrual accounting gives a fuller picture of profitability over time, but it can also mean paying tax on money you haven’t yet received.

Feature | Cash basis | Accrual basis |

Income recorded | When received | When invoiced |

Expenses recorded | When paid | When incurred |

Complexity | Lower | Higher |

Tax timing | Aligned to cash | May lead ahead of cash |

Best suited to | Sole traders, small SMEs | Larger or complex businesses |

For 2026, most unincorporated UK businesses, including sole traders and partnerships, can use cash basis as their default. HMRC has removed previous turnover thresholds, making eligibility much broader than it once was. You can review the full rules in the HMRC guidance on calculating taxable profits.

The 2024/25 changes also brought two significant improvements. First, the old £500 cap on interest deductions no longer applies. Second, more flexible loss rules mean you can now offset or carry back losses in a way that was previously restricted under the cash basis. These updates make the method considerably more attractive than it was even two years ago.

Key eligibility points to know:

Unincorporated businesses (sole traders, most partnerships) are generally eligible

Limited companies cannot use cash basis for income tax purposes

There is no turnover threshold to worry about from 2024/25 onwards

You can opt out of cash basis if accruals better suits your situation

Pro Tip: If you’re unsure whether your business structure qualifies, check your trading status first. A sole trader and a limited company face very different rules, and using the wrong method could cause compliance headaches down the line.

Key benefits of cash basis accounting for UK SMEs

The most immediate benefit is simplicity. You record what you receive and what you pay. There are no debtors ledgers to maintain, no accruals journals, and no need to estimate income you haven’t yet collected. For a business owner who is already stretched thin, that reduction in administrative burden is real and meaningful.

Beyond simplicity, cash basis keeps your taxable profit closely aligned with your actual cash position. This matters enormously when SME cash flow struggles affect between 47% and 82% of UK businesses. Under accrual accounting, you could owe tax on £50,000 of invoiced income even if £20,000 of that remains unpaid at year end. Under cash basis, you only pay tax on what has actually arrived.

“Under cash basis, your tax bill reflects your real-world cash position, not a theoretical profit figure based on invoices that may never be paid.”

This is particularly valuable when clients pay late, which is a persistent problem across UK industries. Rather than scrambling to fund a tax bill on phantom income, your liability stays grounded in reality.

Other practical benefits include:

Faster self-assessment completion: Fewer adjustments mean less time preparing your tax return

Reduced risk of errors: Simpler records lower the chance of mistakes that trigger HMRC queries

Better cash flow visibility: Your accounts reflect what you actually have, making budgeting more straightforward

Lower accountancy costs: Simpler bookkeeping often means less time spent by your accountant, which can reduce fees

For businesses managing their own books, good cash flow management for SMEs becomes far easier when your accounting method mirrors your actual bank movements.

Pro Tip: If your business regularly has a gap of 30 to 90 days between invoicing and receiving payment, cash basis could meaningfully reduce your tax liability in years where collections are slow. Run a quick comparison using last year’s figures to see the difference.

Common challenges and limitations of the cash basis

Cash basis is not a universal solution. Understanding where it falls short is just as important as knowing its strengths.

The most significant limitation is that it can obscure your true financial position. If you have substantial unpaid supplier bills at year end, cash basis won’t reflect those obligations in your profit calculation. Your accounts might show a healthy surplus while in reality you owe thousands to creditors. This can create a misleading picture when you’re trying to plan ahead or apply for finance.

Limited companies cannot use cash basis at all. If your business is incorporated, this conversation doesn’t apply to your income tax position, though it’s worth reviewing tax tips for small business owners for other ways to manage your liability.

Switching from accruals to cash basis also requires careful handling. You’ll need to make one-off adjustments to avoid either double-counting income or missing expenses entirely. This is not complicated with proper guidance, but it does require attention.

Common limitations to weigh up:

Not suitable for limited companies for income tax purposes

May understate liabilities if you have large unpaid bills

Switching adjustments can be complex without professional support

Less useful for financial analysis if you need to track profitability over time

May not suit businesses with significant stock or work in progress

One important update: from 2024/25, losses under cash basis can now be offset against other income or carried back, just as they can under accruals. Previously, this was a major drawback of the method. That restriction has now been removed, which addresses one of the most common objections.

For a broader view of staying compliant, the accounting compliance guide covers the key obligations UK businesses need to track. You can also cross-reference with official HMRC cash basis guidance to confirm your specific situation.

How to switch to cash basis accounting (and what to watch out for)

Switching to cash basis is not as daunting as it sounds, but it does require a structured approach. Rushing the transition without making the right adjustments is where most problems arise.

Here is a practical step-by-step process:

Confirm eligibility: Check that your business is unincorporated and that cash basis suits your trading model.

Review your current records: Identify all outstanding debtors (money owed to you) and creditors (money you owe) at the point of switching.

Make opening adjustments: Switching from accruals requires one-off adjustments for opening debtors, creditors, and any unrelieved capital expenditure to avoid double-counting.

Update your bookkeeping system: Configure your software or records to capture only actual payments and receipts going forward.

Notify via self-assessment: You elect to use cash basis on your self-assessment tax return. There is no separate HMRC form to complete.

Review capital expenditure treatment: Under cash basis, most capital items are deducted when paid rather than through capital allowances. Understand how this affects your current assets.

Switching step | Action required | Common pitfall |

Opening debtors | Exclude from cash basis income | Double-counting if not removed |

Opening creditors | Exclude from cash basis expenses | Claiming twice if not adjusted |

Capital allowances | Review unrelieved expenditure | Missing deductions on transition |

Bookkeeping update | Reconfigure records | Mixing cash and accrual entries |

Once you’ve switched, keep a clear record of the transition adjustments in case HMRC ever queries your return. Knowing how to calculate business taxes correctly after the switch is essential, and being aware of your tax deadlines for small businesses will help you plan the timing of the change effectively.

For further detail on the technical rules around switching, the ICAEW cash basis changes article is one of the most thorough resources available.

Pro Tip: If you’re switching mid-way through a trading year, consider whether it’s cleaner to make the change at the start of a new tax year. This simplifies the opening adjustments and reduces the risk of errors in your first cash basis return.

Why the real choice isn’t ‘cash vs. accruals’ but understanding your business’s cash reality

Here’s the perspective we share with clients that most articles won’t tell you. The debate about cash basis versus accruals is often framed as a technical question when it is really a practical one. The method you choose should mirror how money actually moves through your business, not what sounds simpler on paper.

We’ve seen business owners choose cash basis because it seemed less work, only to find their accounts gave them no useful information about whether they were genuinely profitable. And we’ve seen others stick with accruals out of habit, paying tax on income they hadn’t collected and creating unnecessary cash pressure.

With cash flow concerns remaining the dominant theme for UK SME decision-making, the smartest move is to treat your accounting method as a diagnostic tool. It should surface problems, not smooth them over. If you’re not sure which method gives you the clearest view of your business, that’s the conversation to have with your accountant. Knowing how to budget for tax accurately depends entirely on having accounts that reflect your real cash position.

Get expert support for your accounting and payroll needs

Choosing the right accounting method is only the beginning. Staying compliant, managing payroll, and keeping your records accurate throughout the year is where the real work happens.

At Concorde Company Solutions, we work with sole traders and small businesses across the UK to make cash basis accounting straightforward and fully compliant with HMRC requirements. Whether you need help switching from accruals, setting up your bookkeeping correctly, or managing your payroll solutions alongside your accounts, we’re here to take the complexity off your plate. Visit our business support services page to find out how we can support you, or get in touch directly for a conversation about your specific situation.

Frequently asked questions

Who is eligible to use cash basis accounting in the UK?

Most unincorporated businesses and sole traders can use cash basis, and eligibility has broadened significantly since the 2024 rule changes removed the previous turnover threshold. Limited companies are not eligible.

How does cash basis affect my tax return?

You only pay tax on money actually received during the tax year, meaning tax aligns with payments received rather than invoices raised, which can reduce your liability in years when clients pay late.

What are the main risks of cash basis accounting?

The primary risks are that unpaid supplier bills won’t appear in your accounts, and that switching from accruals requires one-off adjustments that can cause errors if not handled carefully.

Do recent HMRC changes make cash basis more attractive?

Yes. The removal of the £500 interest deduction cap and improved loss rules from 2024 address two of the method’s biggest historical drawbacks, making it a more competitive option for eligible businesses in 2026.

Recommended

Comments