How to Calculate Business Taxes for UK Companies Easily

- David Rawlinson

- Dec 8, 2025

- 7 min read

Every british business owner faces the reality that even a single missing record can trigger unwanted attention from HMRC. Managing taxes in the United Kingdom is far more complex than just filling out forms, with over 40 percent of businesses struggling to meet filing requirements on time. Knowing how to gather the right documentation and apply the correct tax rules empowers you to avoid costly mistakes and reduce stress. This guide simplifies every stage so you can approach tax season with clarity and confidence.

Table of Contents

Quick Summary

Key Insight | Explanation |

1. Gather Financial Records | Compile detailed financial records including income statements, receipts, and payroll records to ensure accurate tax calculations. |

2. Identify Tax Types and Allowances | Understand applicable UK tax obligations and potential allowances specific to your business structure and industry. |

3. Accurately Calculate Taxable Profits | Meticulously calculate taxable profits by assessing total income and allowable business expenses to avoid miscalculations. |

4. Apply Correct Tax Rates and Reliefs | Implement applicable tax rates and reliefs to optimise financial strategies and ensure compliance with HMRC regulations. |

5. Review and Verify Calculations | Conduct thorough reviews of tax calculations and consider professional advice to prevent errors and ensure accuracy before submission. |

Step 1: Gather Required Financial Records

Calculating business taxes begins with methodically collecting and organising all critical financial documentation. Your goal is to compile a comprehensive set of records that will enable precise tax calculations and demonstrate full compliance with HMRC regulations.

Start by assembling fundamental financial records that provide a complete picture of your business financial activity. This collection should include detailed income statements showing all revenue streams, comprehensive balance sheets reflecting your company’s financial position, bank statements capturing all transactions, expense receipts documenting business expenditures, payroll records, investment documentation, and any supporting financial journals or ledgers. Each document serves as evidence of your business financial performance and will help determine your precise tax liability.

A professional tip is to maintain digital copies of all physical documents and establish a systematic filing system that allows quick retrieval. Consider scanning paper documents and storing them securely in cloud storage or an encrypted digital archive. This approach not only protects against potential loss but also streamlines the tax preparation process, making it easier to track financial information throughout the year.

With your financial records gathered, you are now prepared to move forward to the next critical stage of tax calculation: analysing and categorising your financial data.

Step 2: Identify Relevant Tax Types and Allowances

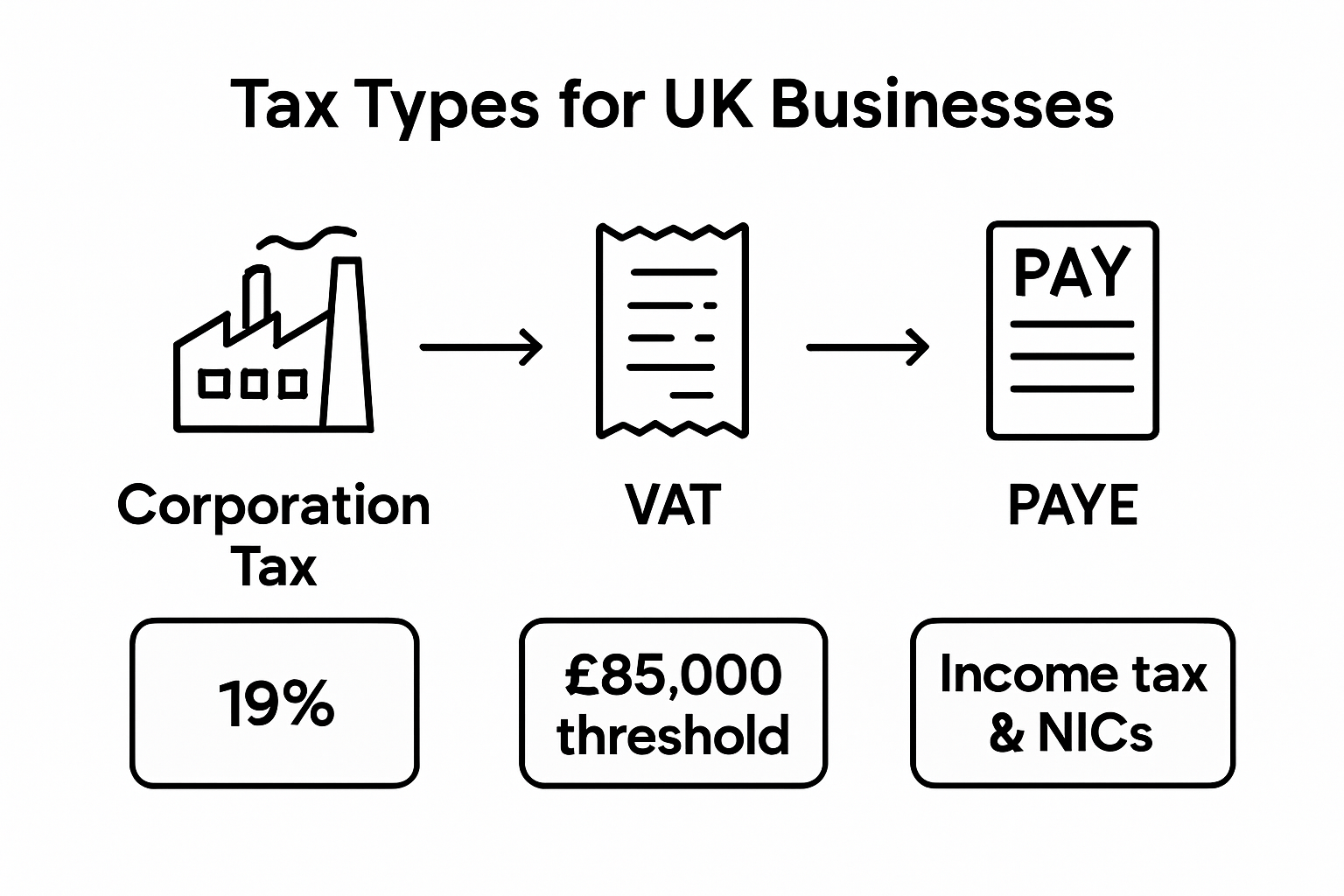

Understanding the landscape of UK business taxation requires a strategic approach to identifying the specific tax obligations that apply to your company. Each business structure and sector faces unique tax responsibilities, making it crucial to comprehensively map out your specific tax requirements.

The primary tax types UK businesses typically encounter include Corporation Tax, which applies to limited company profits, Value Added Tax (VAT) for businesses turning over more than £85,000 annually, and Pay As You Earn (PAYE) for managing employee income tax and national insurance contributions. Beyond these core taxes, businesses might also need to consider Stamp Duty Land Tax for property transactions, business rates for commercial properties, and sector specific levies. Your company can potentially benefit from various tax allowances, such as the Annual Investment Allowance, which permits businesses to deduct the full value of qualifying equipment investments from their taxable profits.

A strategic tip is to conduct a thorough assessment of your specific business circumstances and consult with a professional tax advisor who can provide tailored guidance. Different industries and company sizes have nuanced tax implications, and what applies to one business might not be relevant to another. Staying informed about current tax regulations and potential relief programmes will help you optimise your tax position and ensure full compliance with HMRC requirements.

With a clear understanding of your applicable tax types and potential allowances, you are now prepared to move towards calculating your precise tax liabilities.

Step 3: Calculate Taxable Profits Accurately

Calculating your business’s taxable profits requires a meticulous approach to financial analysis, ensuring every revenue stream and allowable expense is carefully considered. Navigating the complexities of Corporation Tax calculations demands precision and a thorough understanding of HMRC guidelines.

To determine your taxable profits, start by calculating your total business income, which includes all revenue from sales, services, investments, and other sources. Next, subtract allowable business expenses such as operational costs, employee wages, office supplies, and equipment purchases. Special attention should be given to capital allowances, which permit you to deduct the value of qualifying business assets like machinery, vehicles, and computer equipment. Research and Development (R&D) tax relief offers additional opportunities for qualifying businesses to reduce their tax liability by claiming credits for innovation and technological advancement.

A critical tip is to maintain comprehensive and organised financial records throughout the year, as this simplifies the profit calculation process and provides a clear audit trail. Keep digital and physical copies of all financial documents, including invoices, receipts, bank statements, and expense records. Consider consulting with a professional accountant who can help you identify all potential tax deductions and ensure your calculations align with the latest HMRC regulations.

With your taxable profits accurately calculated, you are now prepared to move forward to the next stage of your tax preparation process.

Step 4: Apply Applicable Tax Rates and Reliefs

Applying the correct tax rates and reliefs is a critical step in optimising your business’s financial strategy. Tax planning requires a strategic approach to ensure you maximise available allowances while maintaining full compliance with HMRC regulations.

For limited companies, the standard Corporation Tax rate currently stands at 25% for profits exceeding £250,000, with a reduced rate of 19% for profits under £50,000. Businesses with profits between these thresholds benefit from a marginal relief system. Key tax reliefs to consider include the Annual Investment Allowance, which permits businesses to deduct the full value of qualifying capital equipment purchases from taxable profits. Research and Development (R&D) tax credits offer additional relief for innovative companies, allowing them to claim significant tax deductions or cash credits for qualifying technological advancements and scientific research.

A strategic tip is to carefully document all potential tax reliefs and consult with a professional tax advisor who can help you navigate the complexities of tax regulations. Different business sectors may qualify for specific tax relief programmes, and staying informed about the latest HMRC guidelines can help you minimise your tax liability while ensuring full legal compliance. Keep detailed records of all investments, equipment purchases, and innovative projects that might qualify for additional tax relief.

With the applicable tax rates and reliefs applied, you are now prepared to complete your final tax calculations and submission.

Step 5: Review and Verify Tax Calculations

Careful review and verification of your tax calculations is a critical final step in ensuring accurate financial reporting. Thorough tax return preparation demands meticulous attention to every financial detail to prevent potential errors or costly miscalculations.

Begin by cross-referencing all income sources, including sales revenue, investments, grants, and secondary business income streams. Carefully reconcile each expense category against supporting documentation, verifying that every claimed deduction meets HMRC guidelines. Pay special attention to complex calculations such as capital allowances, research and development tax credits, and marginal relief adjustments. Use spreadsheet software or professional accounting tools to double check your calculations, ensuring mathematical accuracy and consistency across all financial statements.

A strategic tip is to create a systematic verification checklist that covers all critical aspects of your tax calculation. Consider having a second set of eyes review your work professional accountant or trusted financial advisor can provide an independent perspective and identify potential discrepancies you might have overlooked. Remember that even minor calculation errors can trigger HMRC audits or result in unexpected tax penalties, so precision is paramount.

With your tax calculations thoroughly reviewed and verified, you are now prepared to submit your final tax documentation with confidence.

Simplify Your UK Business Tax Calculations with Expert Support

Calculating business taxes for UK companies can be overwhelming when you face complex tax rates, allowances, and the need for meticulous record-keeping described in this guide. If you find yourself struggling to accurately gather financial records, apply correct Corporation Tax rates, or identify all relevant tax reliefs, you are not alone. Ensuring compliance with HMRC while maximising your tax position takes a dedicated approach and professional insight.

Discover how Concorde Company Solutions in Garforth, Leeds, can partner with you to streamline your entire tax process. From managing your company tax returns with precision, to providing ongoing bookkeeping and payroll management, our personalised services help you stay organised and confident. Benefit now from transparent pricing and expert advice tailored specifically to small and medium-sized businesses. Take control of your business taxes today by visiting Concorde Company Solutions and contacting us for dedicated, professional help you can trust.

Frequently Asked Questions

How do I gather the necessary financial records for calculating business taxes?

To calculate business taxes, start by compiling essential financial records such as income statements, balance sheets, bank statements, and expense receipts. Organise these documents methodically to ensure easy retrieval and maintain digital copies to safeguard against loss.

What tax types should I be aware of for my UK company?

UK companies typically encounter Corporation Tax, Value Added Tax (VAT), and Pay As You Earn (PAYE) for employee income tax and national insurance contributions. Identify which of these taxes apply to your specific business structure and sector to ensure compliance.

How can I accurately calculate my taxable profits?

Calculate your taxable profits by determining your total business income and subtracting allowable expenses, including operational costs and wages. Keep detailed records of all transactions to streamline this calculation and provide an audit trail for verification.

What tax rates and reliefs should I apply when calculating business taxes?

Apply the appropriate Corporation Tax rate, which is currently 25% for profits above £250,000 or a reduced rate of 19% for profits under £50,000. Consider applicable tax reliefs such as the Annual Investment Allowance to minimise your tax liability effectively.

How do I review and verify my tax calculations before submission?

Review your tax calculations by cross-referencing all income sources and reconciling them against supporting documents. Create a checklist to ensure every financial detail is accounted for, and consider having a professional review your work to catch any discrepancies.

Recommended

Comments