What is capital allowances: a 2026 UK guide

- David Rawlinson

- May 30

- 9 min read

TL;DR:

Most UK business owners mistakenly believe equipment purchases automatically reduce their tax bills, but active claims of capital allowances are required for the relief. If not claimed correctly, businesses risk higher taxes due to balancing charges or missing out on potential savings, especially with 2026 rate changes lowering the main writing-down allowance. Proper record keeping, timing, and strategic planning of capital asset purchases can optimize tax benefits and prevent costly errors.

Most UK business owners assume that buying a piece of equipment for the company automatically reduces their tax bill. It does not. Capital allowances are the formal mechanism that makes that reduction possible, and they must be actively claimed. Miss the claim, and you leave money on the table. Get it wrong, and HMRC may raise a balancing charge that adds to your taxable profits rather than reducing them. This guide walks you through what capital allowances are, how the 2026 changes affect your position, and how to use them as a deliberate tool in your tax planning.

Table of Contents

Key takeaways

Point | Details |

Not automatic relief | You must actively claim capital allowances; HMRC will not apply them for you. |

Replaces depreciation | Capital allowances substitute commercial depreciation for tax purposes on qualifying assets. |

AIA gives full relief | The annual investment allowance covers up to £1 million on qualifying plant and machinery. |

2026 rates have changed | The main writing-down allowance dropped from 18% to 14%, with a new 40% first-year allowance introduced. |

Balancing charges bite | Selling an asset above its pool value creates a taxable charge, even if you claimed full relief originally. |

What is capital allowances: the core principles

Capital allowances replace commercial depreciation for tax purposes, allowing businesses to deduct the cost of qualifying capital assets from their taxable profits. That distinction matters. Your accountant might depreciate a piece of machinery over five years in your statutory accounts, but HMRC does not recognise that commercial depreciation figure. Instead, capital allowances are the permitted deduction, calculated under a separate set of rules.

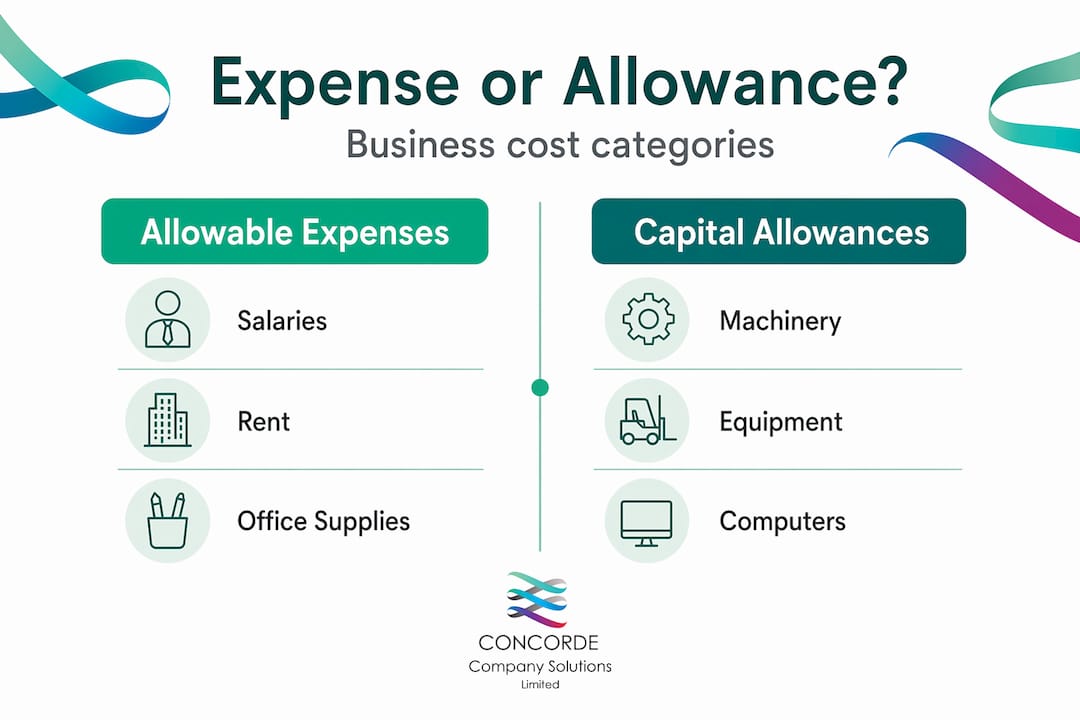

The difference between capital allowances and allowable expenses catches many business owners out. Allowable expenses cover day-to-day running costs such as rent, salaries, and utility bills. Those reduce your profit directly. Capital expenditure, by contrast, is spending on assets that have a lasting benefit: machinery, vehicles, computers, and building fixtures. For a fuller breakdown of where the line falls, the Concordecompanysolutions guide on allowable versus capital costs is worth reading alongside this article.

The main categories of capital allowances you need to know are:

Plant and machinery allowances. This covers the broadest range of assets, from factory equipment to office computers and commercial vehicles.

Structures and buildings allowance (SBA). Introduced in 2018, this gives a 3% annual deduction on the cost of new commercial structures and buildings.

Annual investment allowance (AIA). A 100% deduction in the year of purchase for qualifying plant and machinery, up to a set limit.

Writing-down allowances (WDA). Applied as a percentage of the remaining pool value each year for assets not covered by AIA or full expensing.

First-year allowances (FYA). Enhanced deductions for specific asset types, including energy-efficient equipment.

One detail that confuses people is how costs are grouped. Capital allowances are pooled by asset category, so your deduction is calculated on the total pool value rather than asset by asset. This simplifies the maths but means you need accurate records of what sits in each pool.

The timing of a claim also depends on your business structure. For companies, the chargeable period aligns with the accounting period and cannot exceed 12 months. For sole traders and partnerships, it follows the period of account, which can vary. Get the period wrong and your claim may be invalid.

Types of capital allowances and the 2026 rate changes

Understanding the types available is where capital allowances explained properly starts to pay off. Each type suits different spending patterns, so choosing the right one for each asset matters.

Annual investment allowance

The AIA gives 100% relief on qualifying plant and machinery costs up to £1 million per year. For most SMEs, this limit means the AIA covers the entirety of their capital spending in a given year. However, it excludes cars entirely, and it does not apply to assets received as gifts or assets you already owned before they were used in the business.

Writing-down allowances and the new first-year allowance

This is where 2026 brings a significant shift. The main WDA rate has been reduced from 18% to 14% per year. That means if you have £100,000 in your main pool, you can now only deduct £14,000 in that tax year rather than £18,000. The special rate pool, which covers assets such as thermal insulation and long-life assets, continues at 6%.

To compensate, the government introduced a new 40% first-year allowance for plant and machinery spending that does not qualify for AIA or full expensing. The 2026 adjustments to WDA and the new FYA reflect the UK government’s attempt to balance investment incentives with longer-term fiscal sustainability.

Here is a quick comparison of the main allowances:

Allowance | Rate | Applies to | Key exclusion |

AIA | 100% | Plant and machinery | Cars, gifts |

Full expensing | 100% | New qualifying main rate assets | Not for special rate assets |

New FYA (2026) | 40% | Main rate assets not covered by AIA | Cars, second-hand assets |

WDA (main pool) | 14% | Remaining pool balance | N/A |

WDA (special rate) | 6% | Long-life and thermal assets | N/A |

SBA | 3% | New commercial structures | Residential property |

Pro Tip: If you are planning a significant equipment purchase and the spend will push you above the AIA limit, timing it across two accounting periods can mean two years of 100% AIA relief rather than falling into the lower WDA rate on the excess.

The capital allowance claims process

Knowing what expenses qualify for capital allowances is only half the task. You also need to know how to claim correctly, because capital allowances must be actively claimed and will not be applied automatically by HMRC.

For companies, the claim goes through the corporation tax return (CT600). For sole traders and partners, it appears on the self-assessment return. In both cases, you declare the assets purchased, assign them to the correct pool, and calculate the relief.

Common mistakes to avoid during the capital allowance claims process:

Claiming for assets that are not qualifying. Land, most buildings (unless SBA applies), and non-business assets do not qualify. Neither do assets purchased solely for personal use.

Confusing capital and revenue expenditure. Replacing a roof entirely is capital; patching it is revenue. The distinction has a major impact on which deduction applies.

Forgetting pre-trading assets. You can claim for equipment bought before your business started, provided it is in use for business purposes when trading begins.

Missing balancing charges on disposal. When you sell an asset and the proceeds exceed the remaining pool value, the surplus is added back to taxable profits as a balancing charge. This catches people out when they previously claimed AIA in full.

Good record keeping is the backbone of any successful claim. Detailed records of grouped capital asset pools prevent missed claims and errors during filing. Keep purchase invoices, disposal records, and a running pool calculation updated each year.

Pro Tip: Set up a capital asset register from day one of trading. Record the purchase date, cost, pool category, and any disposal details for every qualifying asset. This takes minutes to maintain and saves hours when your tax return is due.

Strategic use for financial planning

Capital allowances for businesses are not just a compliance box to tick. Used thoughtfully, they are one of the most effective tools for managing taxable profits and improving cash flow.

Capital allowances incentivise investment by allowing accelerated deductions compared to standard depreciation schedules. For a business investing £500,000 in new machinery, claiming AIA in full that year reduces taxable profits by £500,000 immediately, rather than spreading the deduction over several years. At the current corporation tax rate of 25%, that is a £125,000 cash flow benefit in year one.

Here are four strategic approaches worth considering:

Time purchases around your accounting period. Buying equipment just before your year end accelerates the relief. Buying just after delays it by 12 months.

Consider the impact of the WDA rate reduction. With the main rate now at 14%, assets sitting in the pool accumulate slowly. If you have large pool balances, spending on AIA-qualifying assets can clear those pools faster and more efficiently.

Plan for disposals carefully. Balancing charges can unexpectedly increase taxable profits when you sell a fully-expensed asset. Timing a disposal in a lower-profit year reduces the bite of that charge.

Integrate with other reliefs. Capital allowances sit alongside reliefs such as R&D tax credits and the patent box. Understanding which spending qualifies for which relief avoids double claiming and maximises total tax efficiency. The Concordecompanysolutions article on SME tax optimisation covers how to layer these approaches effectively.

For businesses with international operations, the picture is more complex. Capital allowances in multinational corporate structures substantially affect net tax liabilities, particularly where foreign permanent establishment exemptions apply. If you operate across borders, pairing capital allowance planning with currency risk management can protect the value of those tax savings.

“The businesses that get the most from capital allowances are not necessarily those with the biggest capital spend. They are the ones who plan their purchases deliberately, keep clean records, and revisit their pool balances at least once a year.”

Capital allowances versus allowable expenses

The distinction between these two categories is where businesses most often make costly errors. Understanding the difference between capital allowances and allowable expenses is not just an accounting technicality. It determines which tax return box the deduction goes into and whether HMRC will accept the claim.

Item | Allowable expense | Capital allowance |

Office stationery | Yes | No |

New laptop for business use | No | Yes (main pool or AIA) |

Monthly software subscription | Yes | No |

Purchased software licence | No | Yes (main pool) |

Staff salaries | Yes | No |

Factory machinery | No | Yes (AIA or WDA) |

Repair to existing equipment | Yes | No |

Full replacement of equipment | No | Yes |

Business car (owned) | No | Yes (special rate pool) |

The practical rule: if the spending creates or improves an asset with lasting value, it is capital. If it keeps the business running day-to-day, it is revenue. There are grey areas, particularly around improvements versus repairs, and HMRC guidance on this is worth reviewing carefully. The 2025 tax changes for Leeds businesses article from Concordecompanysolutions also covers how recent legislative shifts affect these deduction categories.

My take on capital allowances after years of advising UK businesses

I have worked with a wide range of UK businesses on their tax planning, and the pattern is consistent. Capital allowances are the area where good intentions and poor execution cost the most money.

The balancing charge is the most misunderstood element. I have seen businesses claim full expensing on a piece of equipment, then sell it three years later for a healthy sum and be completely blindsided by the taxable charge that followed. They thought the relief was permanent. It is not. It is a timing benefit, and disposal triggers a reckoning.

The 2026 rate changes reinforce why you cannot rely on rules you learned two or three years ago. The WDA rate dropping from 18% to 14% is not dramatic in isolation, but across a pool of £300,000 or £400,000, the difference compounds quickly. Knowing this now means you can adjust your purchasing strategy before the tax return is filed, not after.

My honest advice: treat your capital asset register with the same rigour as your bank reconciliation. Review it quarterly. Plan disposals with your accountant before completing them, not after. And do not assume the rules are the same as last year. They frequently are not.

— David

How Concordecompanysolutions can help

Capital allowances are one of the most valuable reliefs available to UK businesses, but the rules are detailed, the 2026 changes are material, and the cost of errors runs in both directions. At Concordecompanysolutions, based in Garforth, Leeds, we work with small and medium-sized businesses to get this right. From setting up your capital asset register correctly to reviewing your pool balances and planning disposals, we handle the detail so you can focus on running your business.

Our payroll and tax management services are built around exactly this kind of proactive, year-round support. If you want to make sure your 2026 capital allowance claims are accurate, compliant, and as tax-efficient as possible, get in touch with the team today.

FAQ

What is capital allowances in simple terms?

Capital allowances are a form of tax relief that lets UK businesses deduct the cost of qualifying assets, such as machinery and equipment, from their taxable profits. They replace commercial depreciation for tax purposes and must be actively claimed on your tax return.

What expenses qualify for capital allowances?

Qualifying expenditure includes plant and machinery, commercial vehicles, computers, fixtures, and certain building works. Land, most residential property, and assets used wholly outside the business do not qualify.

How do capital allowances differ from allowable expenses?

Allowable expenses cover day-to-day running costs such as salaries and rent, which reduce profit directly. Capital allowances apply to capital assets with lasting value, such as equipment and machinery, and are claimed through a separate calculation process.

What changed with capital allowances in 2026?

The main writing-down allowance rate fell from 18% to 14%, and a new 40% first-year allowance was introduced for main rate plant and machinery that does not qualify for AIA or full expensing.

What is a balancing charge and when does it apply?

A balancing charge arises when you sell an asset and the sale proceeds exceed the remaining value in the pool. The excess is added to your taxable profits, even if you previously claimed 100% relief on that asset through AIA or full expensing.

Recommended

Comments