Tax Deadlines 2025: Critical Dates for UK Businesses

- David Rawlinson

- Jan 25

- 15 min read

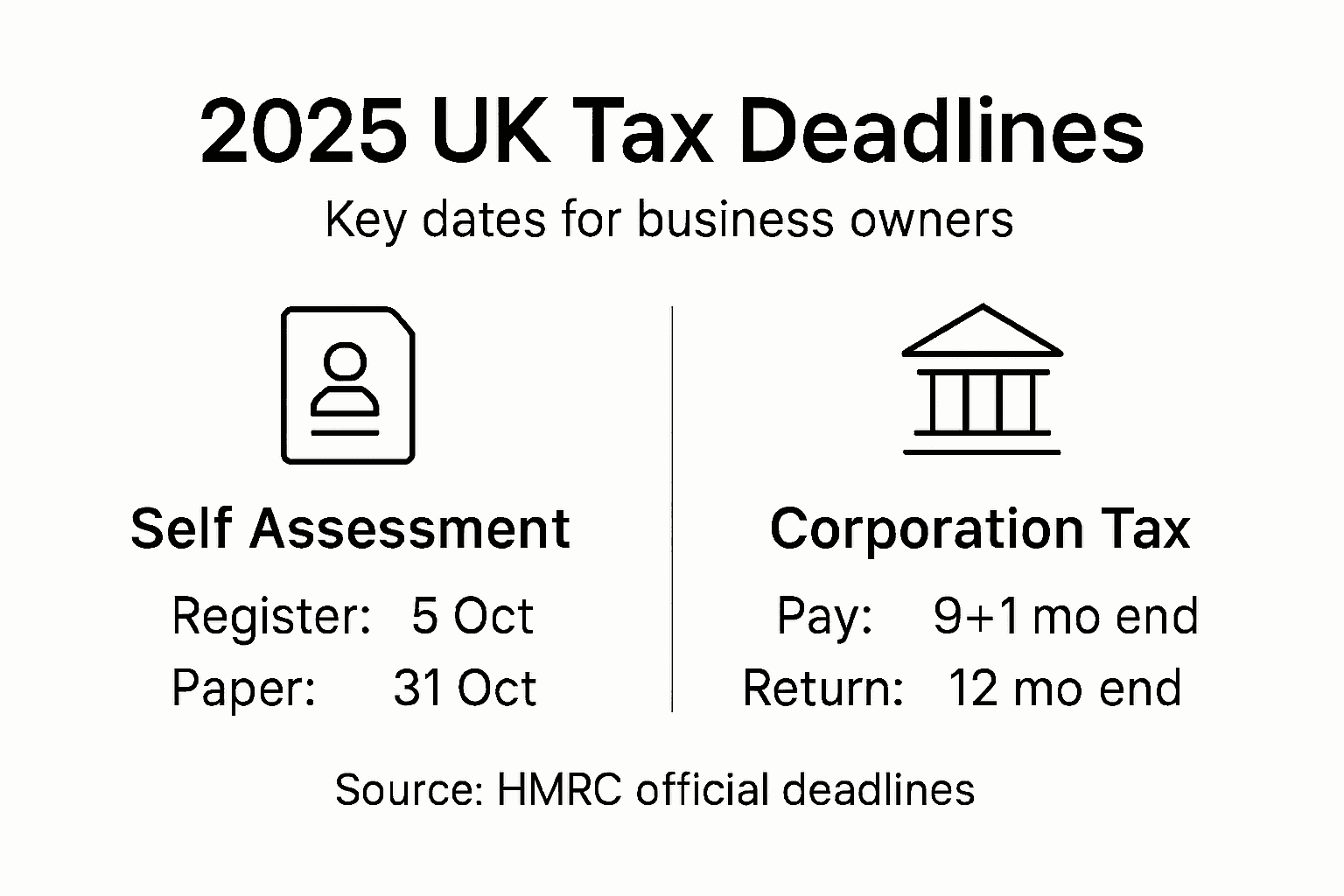

Missing a critical date with HMRC is more common than many Garforth and Leeds business owners realise. The UK tax year for 2025 runs from 6 April 2025 to 5 April 2026 and features several key deadlines such as 5 October for Self Assessment registration, 31 October for paper returns, and 31 January for online returns and final payments. Knowing these milestones is vital for avoiding unexpected penalties and planning your business cash flow with confidence.

Table of Contents

Key Takeaways

Point | Details |

Understand Tax Deadlines | The UK tax year runs from 6 April 2025 to 5 April 2026; crucial deadlines for submissions and payments must be noted to avoid penalties. |

Penalties Escalate Quickly | Missing deadlines incurs immediate penalties, starting at £100 and compounding if delays continue, highlighting the need for timely submissions. |

Incorporate Forward Planning | Regularly update your calendar and maintain organised records throughout the year to ensure compliance and ease of payment. |

Consider Professional Support | Engaging an accountancy firm can alleviate the burden of managing tax obligations and streamline compliance for business owners. |

UK Tax Deadlines 2025 Explained

The UK tax year for 2025 runs from 6 April 2025 to 5 April 2026, and understanding this calendar is fundamental to staying compliant with HMRC requirements. Unlike the calendar year that most of us follow, the UK tax system operates on its own schedule, which affects everything from when you submit returns to when you pay what you owe. This distinction matters because missing these deadlines carries real financial consequences, with penalties escalating quickly if you fall behind. For business owners and sole traders in Garforth and Leeds, getting these dates locked into your diary isn’t optional—it’s the foundation of staying on the right side of HMRC.

Several critical deadlines cluster around specific points in the tax year, and each one serves a different purpose. If you need to complete a tax return for the previous tax year, you must notify HMRC by 5 October 2025. Paper tax returns have to be submitted by 31 October 2025, whilst online returns are due by 31 January 2026. This gives you roughly three months longer if you file online rather than on paper, which is why most accountants recommend the digital route. Your tax payment also falls due on 31 January 2026. If you have ongoing tax liabilities throughout the year, you’ll also need to meet payment on account deadlines, which occur on 31 July 2025 and 31 January 2026—essentially, HMRC asks you to pay part of what you expect to owe in advance.

What catches many business owners off guard is how quickly penalties accumulate. Miss the 31 January deadline by even a day, and you’re facing an automatic £100 fine, regardless of the amount owed. Delay longer, and the penalties compound at 5% of the tax due. If you’re self-employed or running a limited company, managing these dates becomes even more critical because the consequences ripple through your business finances and can affect your ability to access credit or grow. The most practical approach is to work backwards from these deadlines with your accountant, ensuring your records are organised and your figures are ready well in advance. This also gives you time to plan any tax payments without scrambling at the last minute.

Understanding the tax year structure and key deadlines also helps with forward planning. If you’re preparing accounts for a year-end in December, your Self Assessment deadline falls a full month into the next calendar year, which often surprises new business owners. Building this into your annual calendar prevents last-minute stress and ensures you’re never caught out. Many accountancy firms, including those offering comprehensive support for small businesses, recommend mapping out the entire financial year once you know your business year-end, so nothing catches you by surprise.

Pro tip: Set calendar reminders on 1 December for paper return deadlines and 1 January for online submission dates—this gives you roughly a month’s buffer to gather documents and finalise figures before HMRC’s final deadline arrives.

Key Self Assessment Dates for 2025

Self Assessment isn’t a single deadline you hit once a year. It’s a series of staggered dates throughout the tax year that each demand your attention. For sole traders and individuals in Garforth and Leeds, missing even one of these dates can trigger penalties that compound your tax bill unnecessarily. The first critical date you need to mark is 5 October 2025. If you haven’t already registered for Self Assessment or you’re filing for the first time for the 2024-25 tax year, you must register for Self Assessment by this date. Registration isn’t instantaneous, so if you’re only just becoming self-employed or have recently started a business, don’t delay in getting registered. Once you’re registered, HMRC sends you a unique tax reference number, which you’ll need for all future filings.

Once registered, the filing deadlines kick in, and they differ depending on how you file. Paper returns must be submitted by 31 October 2025, but here’s where most people in your situation make the smart choice: online returns don’t close until 31 January 2026. That’s three full months of extra time. Alongside your return, you’re also paying any tax that was due from the previous tax year, and that payment is also due by 31 January 2026. If your tax bill is substantial, you might also have payments on account due earlier. These are estimated payments made on 31 July 2025 and another on 31 January 2026. Think of them as HMRC asking you to pay part of next year’s bill in advance. This arrangement prevents a single enormous bill landing in January and spreads your tax obligations across the financial year. For some business owners, particularly those with variable income, this can actually help with cash flow planning.

One date that often surprises self-employed individuals is 30 December 2025. If you want HMRC to collect tax through your PAYE code instead of through Self Assessment, you need to opt in before this date. This option only works if you’re employed and self-employed simultaneously, or if you’re receiving pension income alongside self-employment earnings. It’s not available to everyone, but if it applies to your situation, it can simplify your tax affairs considerably by combining everything into your payslip rather than requiring a separate Self Assessment return.

The consequences of missing these dates aren’t theoretical. A late submission by even one day triggers a £100 fixed penalty. Delay longer, and you face 5% of the unpaid tax as an additional penalty. If you’re running a business alongside other commitments, the easiest way to avoid this stress is to get organised early. Start gathering your records and figures around November, so you’re never rushing in December. This gives your accountant time to prepare your return accurately and gives you a buffer in case anything needs clarifying.

Pro tip: File online by the end of December, not on 31 January, so you see your tax bill with time to arrange payment without scrambling.

Important Corporation Tax Milestones

If you operate your business as a limited company, Corporation Tax deadlines work completely differently from Self Assessment. This is where many business owners in Garforth and Leeds make costly mistakes, treating Corporation Tax like personal income tax when the two operate on entirely separate calendars. Your company’s accounting period dictates when these deadlines fall, not the standard UK tax year. This flexibility can actually work in your favour if you plan carefully, but it also means you cannot rely on generic “January deadline” reminders. Instead, you need to understand your specific accounting period and count forward from your year-end date.

The critical milestone is your Corporation Tax payment deadline, which falls 9 months and 1 day after your accounting period ends. If your company’s year-end is 31 December 2025, for example, your Corporation Tax payment is due by 30 September 2026. This gives you a substantial window compared to personal Self Assessment, but don’t let that breathing room lull you into complacency. Many companies find themselves short of cash by the time this deadline arrives if they haven’t planned ahead. Running up to this date, you also need to file your Corporation Tax return, known as the CT600 form. Corporation Tax filing deadlines occur within 12 months after your accounting period ends, giving you three additional months beyond the payment deadline. This seems backwards, but it’s how the system works: you can pay the tax before submitting your return, though most companies submit first, see what they owe, then pay.

The practical challenge is that these deadlines don’t align with any calendar reminders you might already be using. You cannot simply mark January or April in your diary and expect to capture all your Corporation Tax obligations. Instead, work with your accountant to map out your specific deadlines based on your accounting year-end. If you’re unsure when your year-end falls or what your payment deadline actually is, this is precisely the conversation to have with your accountancy firm. They can give you exact dates tailored to your company’s structure and timeline. This matters because missing the 9 months and 1 day payment deadline triggers a 10% penalty on unpaid tax, with additional penalties escalating if the tax remains unpaid longer. The financial impact compounds quickly, turning a manageable tax bill into a serious cash flow crisis.

Many limited companies also need to consider Corporation Tax estimates and installment payments if they expect to owe more than £3 million in tax. These quarterly payments begin months before your final deadline, effectively front-loading your cash flow obligations. Again, this depends entirely on your individual circumstances and the size of your profits. Understanding whether you fall into this bracket is crucial planning information that your accountant should clarify with you at the start of your financial year.

Pro tip: Create a spreadsheet at the start of your financial year showing both your 9 months and 1 day payment deadline and your 12-month CT600 filing deadline, then set calendar reminders two months before each date so you’re never caught off guard.

VAT, PAYE, and Other Filing Requirements

Whilst Corporation Tax and Self Assessment grab most of the headlines, they’re only part of the compliance puzzle for business owners in Garforth and Leeds. If you’re employing staff, you’re managing PAYE (Pay As You Earn) obligations that demand their own attention and deadlines. If you’re trading above the VAT threshold, you’re juggling quarterly VAT returns. These aren’t optional extras or things you can handle casually alongside your main tax deadlines. They’re statutory obligations with their own penalty structures, and getting them wrong creates immediate cash flow problems and HMRC attention.

VAT returns typically run on a quarterly basis, meaning you’re submitting four returns across the tax year rather than one annual submission. Your essential HMRC deadlines depend on your VAT registration date and stagger throughout the year. The return itself must be submitted online through HMRC’s systems, and payment of any VAT owed is due when you file. Unlike Self Assessment, which gives you several months of leeway, VAT deadlines don’t shift. If your quarter ends on 31 March, your return is typically due by 30 April, with no extensions for being busy or disorganised. Many businesses fail to account for the cash VAT represents. You’re often holding HMRC’s money temporarily, collecting it from customers and paying it over monthly or quarterly. If you don’t track this separately or set it aside, you’ll face a shortfall when the deadline arrives.

PAYE is equally unforgiving but operates on a different frequency. Monthly, you must submit payroll information to HMRC and pay any income tax and National Insurance contributions you’ve withheld from your employees’ wages. This happens every month without fail, which means twelve separate filing and payment obligations annually. The deadline is typically the 19th of each month if you’re paying electronically. Miss this, and penalties accumulate per employee per day late. For a business with five employees, missing one deadline suddenly means compound penalties that dwarf the original tax owed. Alongside monthly PAYE, you also file an annual return called a P35 and provide each employee with a P60. These year-end forms reconcile what you’ve paid across the twelve monthly submissions and must be accurate, as employees use them for mortgage applications and other financial matters.

Beyond VAT and PAYE, there are several other filing requirements that slip past many business owners. If you have company directors, you’re filing company accounts with Companies House, which operates on yet another deadline cycle tied to your accounting period. If you offer workplace pensions, there are annual enrolment deadlines and reporting requirements to Pension Regulator. If you’re an employer, you’re also managing automatic enrolment, which dictates when staff must be enrolled and how you communicate changes. The complexity multiplies with every administrative element you add to your business. The best approach is to map all these obligations at the start of your financial year, understanding which are monthly, quarterly, or annual, then building them into a master calendar that sits alongside your tax deadlines. This prevents the chaos of discovering a missed filing obligation months after the fact.

Pro tip: Set up separate bank accounts or sub-accounts for VAT and PAYE, then transfer money there immediately as you collect or withhold it, so you’re never caught short when deadlines arrive.

Here’s a quick reference comparing major UK business tax deadlines and what each requires:

Deadline/Event | Who It Applies To | What Is Required | Consequence of Missing |

5 October 2025 | New self-employed, sole traders | Register for Self Assessment | Delayed registration may cause late filing penalties |

31 October 2025 | Individuals, sole traders | Submit paper tax return | £100 fixed penalty from midnight |

31 January 2026 | All Self Assessment filers | Online return & tax payment | £100 penalty + 5% of tax due after 30 days |

31 July 2025 | Those on payments on account | First payment on account due | Interest charged on underpayments |

30 December 2025 | Employees also self-employed | Opt for tax collected via PAYE | Need separate payment if missed |

Corporation Tax: 9m+1d after year end | Limited companies | Pay Corporation Tax | 10% surcharge after deadline |

VAT: quarterly as per registration | VAT-registered businesses | File VAT return & pay VAT | Penalties based on lateness and prior defaults |

PAYE: 19th monthly (electronic) | Employers | Submit RTI & pay deductions | Penalties per employee per day |

Penalties for Late Filing or Payment

Missing a tax deadline isn’t like missing a social engagement where you can apologise and move on. HMRC operates a rigid penalty system that kicks in automatically the moment a deadline passes, with escalating fines that compound rapidly. For business owners and sole traders in Garforth and Leeds, understanding this penalty structure isn’t about scaremongering—it’s about recognising the real financial consequences of procrastination and poor planning. Many businesses have found themselves paying far more in penalties and interest than their original tax bill, simply because they didn’t file or pay on time.

The Self Assessment penalty structure starts immediately. Miss the 31 January deadline by even one day, and you’re facing an automatic £100 fixed penalty, regardless of how small your tax bill is. This £100 hits your account before any other consequences materialise. If you’re still missing after three months, the penalties escalate further. You’ll face daily penalties of £10 per day for up to 90 days, potentially adding another £900 to your bill. Extend the delay to six months, and late filing penalties shift to 5% of the unpaid tax or £300, whichever is greater. If you’re still outstanding at 12 months, that climbs to another 5% penalty. On top of all this, interest accrues daily on any unpaid tax from the original due date until you finally pay. Someone owing £5,000 in tax could easily face an additional £1,500 in combined penalties and interest by failing to act promptly.

Corporation Tax penalties follow a similar escalating pattern but are tied to your company’s specific accounting period rather than the calendar year. Missing your 12-month CT600 filing deadline triggers a £100 automatic penalty once you’re three months late, then rises to £1,000 per month of continued delay after six months. Late payment penalties on Corporation Tax are equally harsh, with 5% surcharges kicking in after 12 months of non-payment. For limited companies, these penalties pose a genuine threat to cash reserves and can affect your ability to pay employees or suppliers on time. VAT penalties operate differently again. Late VAT returns attract escalating penalties based on how frequently you’ve missed deadlines previously, ranging from 5% to 100% of the outstanding VAT. PAYE penalties are equally stringent, with daily penalties and surcharges accumulating if you miss monthly submission deadlines.

What catches many business owners by surprise is that these penalties are imposed automatically. HMRC doesn’t send a friendly reminder and give you a chance to correct things. The penalty is generated and added to your bill once the deadline passes. You can appeal, but the burden of proof rests with you to demonstrate exceptional circumstances. Being busy isn’t an acceptable reason. Neither is having a disorganised accountant or losing your receipts. The only reliable way to avoid this situation is to treat tax deadlines with the same urgency as meeting payroll deadlines. If you can’t manage this alone, delegating to an accountancy firm removes the risk entirely. They track these deadlines professionally and submit on time as standard practice.

Pro tip: If you’ve missed a deadline, contact HMRC immediately and submit late rather than delaying further; the sooner you file or pay, the sooner penalty calculations stop accruing, and interest charges freeze.

The following table highlights key penalty structures for late tax filing and payment in the UK:

Tax Type | Immediate Penalty | Escalation Timeline | Maximum Potential Penalties |

Self Assessment | £100 fixed fee | £10/day after 3 months, 5% after 6 months | Up to £1,600 + interest over 12 months |

Corporation Tax | £100 after 3 months | £1,000 at 6 months, then up | 10% surcharge on unpaid tax + filing penalties |

VAT | Up to 5%-100% of VAT | Increases with missed deadlines | Penalties compound with repeat offences |

PAYE | Daily per-employee fee | More per continued delay | Significant cumulative cost for businesses |

Tips to Manage Tax Deadlines and Compliance

Managing tax deadlines isn’t a task you handle in January and forget about for the rest of the year. It requires a system, discipline, and ideally, professional support. For business owners and sole traders in Garforth and Leeds juggling multiple responsibilities, the difference between chaos and control often comes down to preparation. The businesses that never miss deadlines don’t rely on memory or good intentions. They build systems that catch deadlines automatically and keep their records organised throughout the financial year. This proactive approach transforms tax compliance from a source of stress into a manageable routine.

Start by creating a master calendar that maps every tax obligation across your financial year. This isn’t optional busywork. Write down your Self Assessment deadline, Corporation Tax payment date, CT600 filing deadline, VAT return dates, PAYE submission dates, and any company filing deadlines with Companies House. Then set reminders two months before each one, giving yourself adequate time to gather documents and prepare submissions. Use HMRC’s online services rather than paper submissions whenever possible. Filing online through HMRC’s systems is faster, reduces errors, and gives you immediate confirmation of submission. Maintain accurate records year-round by implementing a simple bookkeeping system that tracks income and expenses weekly or monthly, rather than scrambling to reconstruct twelve months of transactions in December. Even basic spreadsheets work, though accounting software like Xero or QuickBooks automates this considerably and reduces errors.

Budgeting for tax payments is equally important as tracking deadlines. Many business owners are shocked when their tax bill arrives because they haven’t set money aside throughout the year. Calculate your estimated tax liability quarterly and transfer that amount into a separate savings account immediately. This prevents the situation where your deadline arrives but your cash hasn’t. If you’re paying tax on account for Corporation Tax or Self Assessment, these payments force you to budget ahead anyway, but sole traders without this requirement often fall into the trap of spending all their profit. Payment on account requirements mean you’re pre-paying your estimated tax in July and January, which actually helps with cash flow planning if managed correctly. If you’re genuinely struggling to meet a deadline due to unforeseen circumstances, HMRC does offer payment plans. Contact them before your deadline rather than after, and they’ll often work with you to arrange instalments that protect your business from immediate penalties.

The final piece is knowing when to delegate. If managing these deadlines consumes hours of your time each month or fills you with anxiety, this is precisely what accountancy firms exist to handle. Delegating to professionals like Concorde Company Solutions removes the risk entirely. They track deadlines, gather information from you systematically, prepare your submissions, and ensure everything hits HMRC on time. For many business owners, the peace of mind alone justifies the cost, especially compared to the financial and emotional toll of missing deadlines and facing penalties.

Pro tip: Arrange a quarterly meeting with your accountant to review tax position, discuss upcoming deadlines, and adjust estimates based on actual performance, rather than waiting until December when time pressure forces rushed decisions.

Stay Ahead of UK Tax Deadlines with Expert Support from Concorde Company Solutions

Navigating critical dates like Self Assessment registrations, Corporation Tax payments, and VAT returns can feel overwhelming and risky. Missing a deadline triggers automatic penalties and interest that grow fast. If you are a small business owner or sole trader in Garforth or Leeds, you need clear organisation, trusted expert advice, and a proactive approach to your tax obligations. Our team understands the challenges of meeting HMRC deadlines such as the 5 October Self Assessment registration and the 31 January payment deadline and can help you take control of your tax calendar and compliance.

Don’t wait until late penalties start to affect your cash flow and peace of mind. With services covering payroll management, bookkeeping, statutory accounts, and company tax returns all tailored to your needs, we ensure your tax filings and payments happen on time and without hassle. Visit Concorde Company Solutions today to see how we protect your business from costly mistakes and give you the freedom to focus on growth. Act now and let us keep your tax deadlines under control for 2025 and beyond.

Frequently Asked Questions

What are the key tax deadlines for 2025 in the UK?

The main deadlines include registering for Self Assessment by 5 October 2025, submitting paper tax returns by 31 October 2025, and online returns by 31 January 2026. Additionally, tax payments are due on 31 January 2026, along with payments on account on 31 July 2025 and 31 January 2026.

What happens if I miss the Self Assessment deadline?

If you miss the Self Assessment deadline, you will incur an automatic £100 penalty for the first day overdue. Further penalties, including daily charges and percentage surcharges on unpaid tax, can accumulate quickly if the delay extends.

How do Corporation Tax deadlines differ from Self Assessment deadlines?

Corporation Tax deadlines are based on your company’s accounting period, not the tax year. The Corporation Tax payment deadline is 9 months and 1 day after the accounting period ends, whereas the filing deadline for your CT600 return is 12 months after the same period ends.

Can I file my tax returns online, and why is it recommended?

Yes, you can and it is highly recommended. Filing online gives you until 31 January 2026 to submit your return, offering an extra three months compared to paper submissions. It also provides immediate confirmation from HMRC, reducing the risk of errors and late submissions.

Recommended

Appreciate you sharing this article. I found Companies999 helpful when looking for Birmingham online accountants and this post supports that research.