What are allowable expenses for UK businesses?

- David Rawlinson

- 18 hours ago

- 9 min read

TL;DR:

Many small business owners mistakenly believe all work-related costs are fully claimable, risking HMRC scrutiny.

Allowable expenses must be incurred wholly and exclusively for business purposes and properly documented to reduce taxable profits legally.

Proper record-keeping and understanding the distinction between revenue and capital expenses are essential for legitimate tax claims and avoiding penalties.

Many small business owners and sole traders assume that any cost related to their work is claimable on their tax return. That assumption can be costly. Understanding what are allowable expenses in the UK tax system is the difference between reducing your taxable profit legitimately and making claims that invite HMRC scrutiny. Allowable expenses reduce your taxable profits before Income Tax or Corporation Tax is calculated, which means every valid pound you claim saves you real money. This guide covers the rules, the common categories, and the pitfalls you need to avoid.

Table of Contents

Key takeaways

Point | Details |

The ‘wholly and exclusively’ rule | An expense must be incurred solely for business purposes to qualify as allowable under UK tax law. |

Mixed-use costs need apportionment | If you use something partly for personal use, you can only claim the business proportion with reasonable evidence. |

Revenue vs capital matters | Day-to-day running costs are claimed immediately; capital assets like equipment are handled through capital allowances. |

Common exclusions trip people up | Commuting, personal meals, and ordinary clothing are not allowable, even when work-related contexts exist. |

Records are your protection | Proper documentation such as receipts and logs is what stands between a valid claim and a disallowed one. |

Defining allowable expenses and the ‘wholly and exclusively’ rule

Allowable expenses are costs you incur wholly and exclusively for the purpose of running your business. HMRC subtracts these from your turnover to arrive at your taxable profit, so they do not give you a pound-for-pound cash refund. Instead, they reduce the income on which you pay tax. For a basic-rate taxpayer, a £1,000 allowable expense saves around £200 in tax. For a higher-rate taxpayer, that rises to £400.

The phrase “wholly and exclusively” is the cornerstone of the entire system. It means the expense must have no purpose other than business. If you buy a laptop purely for client work, it qualifies. If you also use it for personal browsing, dual-purpose expenses may be disallowed unless you can clearly apportion and evidence the business share.

Here is where many people go wrong. They assume that because business is the primary reason for a cost, the whole thing is claimable. HMRC does not see it that way. A client dinner, for example, has an obvious personal element (eating) alongside the business element (relationship building). That is why client entertainment is not allowable regardless of intent.

The distinction between revenue and capital expenses matters here too. Revenue expenses are the everyday costs of running your business and are deducted immediately. Capital expenses, such as buying a van or a piece of machinery, are treated differently because they provide lasting value. Those go through a capital allowances calculation rather than a direct deduction.

Pro Tip: When assessing whether a cost qualifies, ask yourself: “Would I have incurred this expense if I had no business?” If the honest answer is no, you are on solid ground. If the answer is yes even partially, you need to think carefully about apportionment.

Key tests to apply before claiming any expense:

Does the cost relate directly to generating business income?

Is there any personal benefit involved?

Can you separate and quantify the business portion clearly?

Do you have documentation to support the amount claimed?

Common categories of allowable business expenses

Knowing the rules is one thing. Knowing what to actually claim is another. Typical allowable expenses accepted by HMRC span a wide range of day-to-day business costs. Here is how the main categories break down.

Office costs. Stationery, printer ink, postage, and business software subscriptions all qualify. A monthly subscription to accounting software or a project management tool used exclusively for your business is claimable in full.

Premises costs. If you rent office or workshop space, the rent, business rates, and utility bills are allowable. If you work from home, you can claim a proportion of your household bills. HMRC offers flat rates for home office claims based on hours worked per month, which removes the need for complex calculations.

Travel and transport. Business mileage, train tickets, parking charges, and accommodation for overnight business trips are all claimable. The key word is business. Travelling from your home to your regular place of work is commuting. Commuting costs are not allowable under any circumstances.

Professional fees and insurance. Your accountant’s fees, solicitor costs for business contracts, and professional indemnity insurance all qualify. Membership fees for a professional body relevant to your trade are typically claimable too.

Marketing and advertising. Website design and hosting, social media advertising spend, printed flyers, and business cards are all eligible. A branded company vehicle wrap also counts because it serves a clear and exclusive business purpose.

Staff and subcontractors. Wages, employer’s National Insurance contributions, and pension contributions for employees are allowable. Payments to subcontractors carrying out work on your behalf are also deductible. You can explore business expense categories in detail to understand how these apply across different industries.

Stock and materials. If you buy goods for resale or raw materials to make products you sell, these are allowable. The cost of goods sold is one of the most straightforward deductions available.

Pro Tip: Keep a running log of recurring subscriptions and service charges each quarter. Small amounts accumulate fast and are easily forgotten at self-assessment time. A missed £50 software subscription over 12 months is £600 in unclaimed deductions.

Notable exclusions worth remembering: personal meals (even if eaten while working), non-branded clothing bought specifically for work, and any fines or penalties including traffic offences incurred during business driving.

Managing mixed-use and dual-purpose expenses

Most sole traders have at least a few expenses that straddle the line between personal and business. Your mobile phone is a good example. You almost certainly use it for both. HMRC expects records or reasonable estimates to support whatever business proportion you claim.

So how do you calculate that proportion fairly? For a mobile phone, look at your itemised bill over a typical month and assess what percentage of calls, data, and messages are work-related. If 60% of your usage is genuinely business, you can claim 60% of the bill. The same logic applies to your home broadband, a vehicle used for both work and personal journeys, or a room in your home used as a dedicated office.

The practices that keep you protected:

Keep digital or physical receipts for every expense you plan to claim

Maintain a mileage log if you use your personal vehicle for business, noting the date, destination, and business purpose of each trip

Use accounting software that timestamps and categorises transactions as you go, rather than reconstructing records at year end

Store records for at least five years after the relevant tax return submission date, as HMRC can open an enquiry within that window

Proper record-keeping is a defensive strategy that goes beyond simple compliance. Without receipts or logs, even legitimate expenses risk disallowance during an audit, and that can trigger penalties on top of the additional tax owed.

Pro Tip: If you work from home and want to avoid the complexity of calculating the exact business proportion of your bills, use HMRC’s simplified flat rate method. For 25 to 50 hours of home working per month, the flat rate is £10. It is not always the maximum you could claim, but it is audit-proof and requires no calculation.

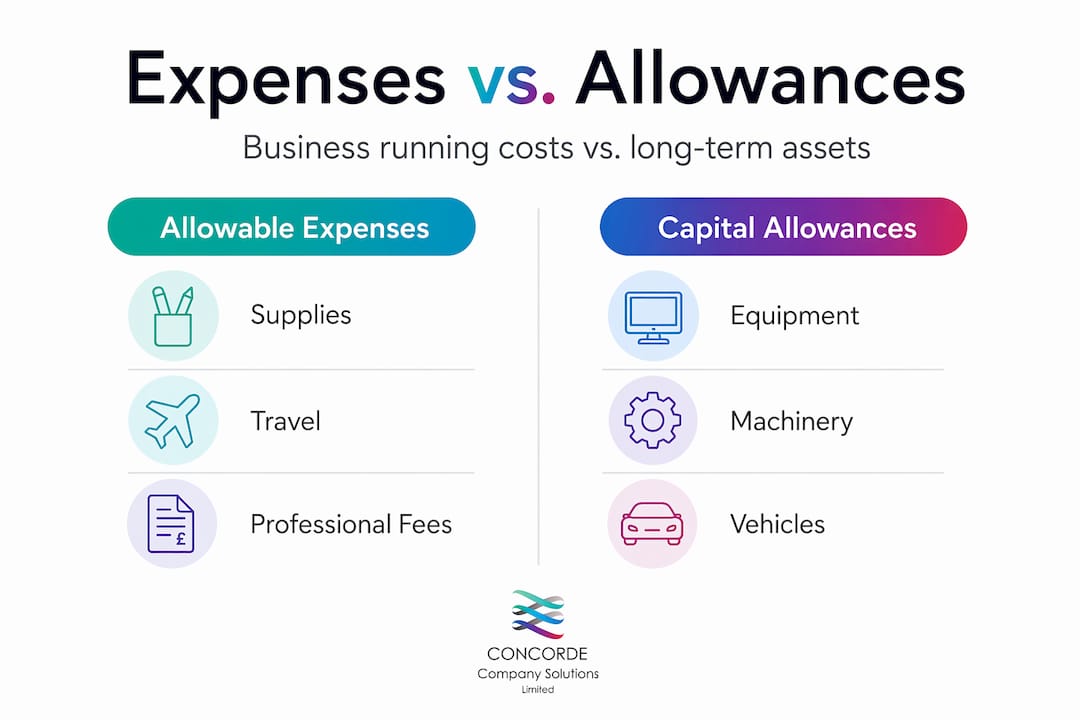

Revenue expenses vs capital allowances

Understanding the difference between allowable expenses and capital allowances is one of the less glamorous but genuinely important aspects of small business tax.

Feature | Revenue expenses | Capital allowances |

What it covers | Day-to-day running costs | Long-term business assets |

Claimed when | Immediately in the tax year incurred | Over time or via Annual Investment Allowance |

Examples | Office supplies, rent, professional fees | Vehicles, machinery, computers |

Effect on tax | Reduces profit in that year directly | Reduces profit over multiple years or in one year via AIA |

Revenue expenses are deductible immediately against profit. Capital expenses, such as buying a computer or a company vehicle, provide lasting value to the business and so must be treated differently for tax.

Capital allowances let you deduct the cost of qualifying long-term assets from your profits over time. The Annual Investment Allowance currently allows a 100% deduction of qualifying capital expenditure up to a set threshold, which for many small businesses means full relief in year one. If you are considering a significant equipment purchase, the timing can have a real impact on your tax bill. Guidance on reducing tax liability with AIA is worth reviewing before you commit.

One area people often get wrong is pre-trading expenditure. If you bought equipment or incurred costs before your business officially started trading, you can still claim these as allowable expenses provided they would have been deductible had the business already been trading at the time.

Common mistakes and how to avoid them

Even experienced business owners make errors when claiming expenses. Awareness is the first line of defence.

Claiming ordinary clothing. Buying a suit for client meetings does not count. Clothing must be exclusively for business use and not suitable for everyday wear. Protective overalls or a branded uniform with a company logo qualify. A smart blazer does not.

Treating commuting as a business journey. The journey from your home to your fixed place of work is personal travel, full stop. Only travel to temporary work locations or between multiple work sites qualifies.

Overclaiming mixed-use costs without records. Claiming 90% business use on a phone when the actual split is closer to 50% is the kind of thing that gets flagged in an HMRC enquiry.

Missing out on legitimate claims. Underclaiming is just as problematic as overclaiming. Professional subscriptions, training directly related to your current trade, and bank charges on your business account are all valid and frequently overlooked.

Failing to keep records. HMRC does not accept verbal explanations. You need physical or digital evidence.

Pro Tip: Set a monthly 15-minute appointment with yourself to reconcile your business expenses. Catching errors and gaps in real time is far less painful than untangling 12 months of records in January.

For a broader view of HMRC compliance requirements, it is worth understanding how expense mistakes contribute to the wider tax gap.

My take on claiming expenses properly

Working with small business owners and sole traders over many years, I have seen the same patterns emerge around allowable expenses. People either claim too little because they are nervous, or too much because they misunderstand the rules.

The ‘wholly and exclusively’ test sounds simple, but it catches people off guard in practice. I have seen clients claim their home internet bill in full when they were heavy personal users. I have seen others miss years of valid professional subscription claims simply because they did not realise they were deductible.

What I have found works is building the habit of treating record-keeping as a year-round activity rather than a January scramble. The businesses that sail through HMRC enquiries are not necessarily those with simpler affairs. They are the ones with organised, consistent records. A well-labelled folder of receipts and a mileage log are not just good admin. They are your defence.

My honest advice: if your expenses are straightforward, a clear understanding of the rules and decent software will see you through. But if you have significant mixed-use costs, capital expenditure decisions to make, or you are newly self-employed, the cost of professional advice pays for itself many times over in both time and legitimate tax savings.

— David

Let Concordecompanysolutions help you claim correctly

Managing allowable expenses correctly takes time, knowledge, and consistency. At Concordecompanysolutions, based in Garforth, Leeds, we work with small business owners and sole traders across the UK to take this burden off your plate. From bookkeeping and self-assessment filing to full payroll and compliance support, we handle the detail so you can focus on running your business. We offer transparent pricing and the kind of personalised service that means you will always know where you stand. Whether you need help untangling mixed-use expenses or want someone to review your claims before submission, we are the partner that keeps you compliant and confident. Get in touch with Concordecompanysolutions today.

FAQ

What are allowable expenses in the UK?

Allowable expenses are business costs that reduce your taxable profit before Income Tax or Corporation Tax is applied. They must be incurred wholly and exclusively for business purposes to qualify.

What counts as allowable expenses for a sole trader?

Common allowable expenses for sole traders include office supplies, business travel, professional fees, marketing costs, staff wages, and a proportion of home working costs. Commuting and personal expenses do not qualify.

Can I claim mixed-use expenses on my tax return?

Yes, but only the business proportion. HMRC expects you to make a reasonable and evidenced estimate of what portion of the cost is for business use, and to retain records that support that calculation.

What is the difference between allowable expenses and capital allowances?

Allowable expenses cover day-to-day running costs and are deducted immediately. Capital allowances apply to long-term assets like vehicles or equipment and are claimed over time, often through the Annual Investment Allowance.

What expenses are not allowable for tax purposes?

Non-allowable expenses include commuting costs, client entertainment, ordinary clothing, personal meals, fines and penalties, and any cost with a personal element that cannot be clearly separated from business use.

Recommended

Comments