Why maintain proper records: a guide for UK businesses

- David Rawlinson

- 23 hours ago

- 8 min read

TL;DR:

Maintaining proper business records is essential for legal compliance, operational efficiency, and securing funding. Digital systems and consistent habits help businesses avoid costly penalties and support growth. Treating documentation as a strategic asset enables businesses to make smarter decisions and adapt to evolving regulations.

Most business owners think of record keeping as something they do for their accountant once a year. That assumption is expensive. Understanding why maintain proper records is not just about satisfying HMRC. It shapes whether you can secure funding, survive an audit, make smart decisions under pressure, and actually grow without the wheels falling off. The businesses that treat documentation as a strategic function rather than an administrative afterthought consistently outperform those that do not. This guide covers the legal obligations, the operational upside, and the practical steps you need to get your records working for you.

Table of Contents

Key takeaways

Point | Details |

Legal retention matters | UK businesses must keep tax and financial records for at least 7 years to cover standard audit periods. |

Poor records cost real money | Record-keeping failures contributed approximately $238.5 million in penalties globally in 2024. |

Records support decisions | Accurate documentation gives you a reliable basis for budgeting, forecasting, and managing cash flow. |

Digital beats manual | Digital systems offer superior accuracy, security, and integration compared to paper-based approaches. |

Discipline is the differentiator | Consistent record keeping separates businesses that scale from those that stall or face avoidable legal trouble. |

Why maintain proper records: the legal obligations

UK law is not vague on this. HMRC requires businesses to retain financial records, including tax returns, invoices, receipts, and payroll documentation, for at least 7 years. That window accounts for standard self-assessment audits and potential extensions where HMRC suspects fraud or negligence.

The types of documents you are legally required to keep include:

Sales invoices and receipts for all transactions

Bank statements and cheque stubs covering all accounts

Payroll records including PAYE submissions, P60s, and P45s

VAT records if you are VAT registered, including VAT account summaries

Contracts and agreements with suppliers, customers, and employees

Company accounts and statutory filings with Companies House

The consequences of not meeting these obligations are not hypothetical. HMRC can issue penalties for missing or incomplete records, and those penalties scale with the severity and persistence of the problem. A business that cannot produce supporting documentation during an investigation has very little ground to stand on. As one key legal principle puts it, “if it wasn’t documented, it wasn’t done”. Courts and tax authorities apply exactly this logic.

Document type | Minimum retention period |

Tax returns and supporting records | 7 years |

Payroll and PAYE records | 3 years from the end of the tax year |

VAT records | 6 years |

Company statutory accounts | 6 years from the date of filing |

Employment contracts | Duration of employment plus 6 years |

Beyond HMRC, sector-specific regulation adds further layers. Financial services firms, healthcare providers, and legal practices face their own retention requirements on top of standard tax rules. Getting this wrong does not just result in a fine. It can trigger regulatory scrutiny that damages your reputation and your ability to trade.

Business benefits beyond legal compliance

Here is where many business owners genuinely underestimate the value of proper documentation. Staying out of trouble with HMRC is the floor, not the ceiling.

Accurate documentation transforms informal activities into repeatable, efficient processes. When your records are clear and current, you can see exactly where your money is going, which clients are most profitable, and where costs are creeping up before they become a serious problem. That is not accounting. That is management.

Pro Tip: Set up monthly reconciliation as a fixed calendar appointment, not a task you do when you remember. Thirty minutes a month catching discrepancies saves days of untangling before a year-end filing.

Proper records also make your business far more attractive to external stakeholders. Lenders reviewing a loan application, investors conducting due diligence, or a potential buyer valuing your business all need to see clean, consistent financial history. A business with organised, well-maintained records secures loans and investments more readily than one that cannot produce coherent financials on request.

There are operational advantages too that rarely get discussed. When a dispute arises with a supplier or a client, your records are your evidence. When a key employee leaves and takes institutional knowledge with them, your documentation fills the gap. Consistent records give your business a single source of truth that does not depend on any one person’s memory or spreadsheet.

The real cost of poor record keeping

The numbers here are sobering. Record-keeping failures contributed approximately $238.5 million in penalties globally in 2024. That figure is not dominated by multinational corporations. Small and medium-sized businesses account for a significant share because they are the ones most likely to treat documentation as optional.

Poor record keeping does not just create compliance risk. It actively destroys business value by blocking growth opportunities and undermining confidence in the business from lenders, auditors, and buyers.

The most common and painful consequence for small business owners is lost tax relief. If you cannot produce receipts and invoices to support a deduction, HMRC will disallow it. You pay tax on income you could have legitimately offset. That is money gone, not from a fine, but from your own failure to keep a piece of paper.

Weak record-keeping also leads directly to rejected loan applications, lost legal cases, and inheritance disputes. A business with messy books signals to a lender that management is unreliable. A contractor without documented agreements has little recourse if a client refuses to pay. These are not edge cases. They happen to UK businesses every day.

The operational cost is harder to quantify but just as real. Teams waste time hunting for missing documents, duplicating work, and rebuilding information that should already exist. Documenting solutions to recurring problems can reduce issue volume by 20 to 30 per cent. Apply that principle to your business processes and you can see how quickly poor records drain time and money.

Best practices for maintaining proper business records

Getting your records in order does not require a finance team. It requires a system and the discipline to use it. Here are the steps that make the biggest difference:

Create a retention schedule. Map every document type your business generates to its legal retention period. Post it somewhere visible and review it annually. This single step prevents most compliance failures before they start.

Digitise your records. HMRC accepts electronic records and digital storage removes the risk of physical loss, whether that is a flood, fire, or simply a filing cabinet that no one can find. Use a dedicated accounting platform rather than folders on someone’s desktop.

Separate personal and business finances. This is one of the most common mistakes sole traders make, and it creates enormous problems at tax time. A dedicated business account makes record keeping dramatically cleaner.

Schedule regular reconciliation. Do not wait for year-end. Monthly reconciliation of your accounts against bank statements catches errors early and keeps your records accurate throughout the year.

Assign ownership. Every document type should have a named person responsible for it. Documentation ownership and regular review scheduling prevents records from becoming outdated or misleading.

Train your team. If employees handle invoices, expenses, or contracts, they need to understand what to record, how to record it, and where it goes. Documentation culture starts with clear expectations.

Pro Tip: When you update a process or change a supplier, update your records at the same time. Updating documentation alongside each change prevents knowledge decay and stops operational bottlenecks before they form.

For businesses looking at how to organise records for UK compliance, the structure you choose matters as much as the habit of keeping records at all.

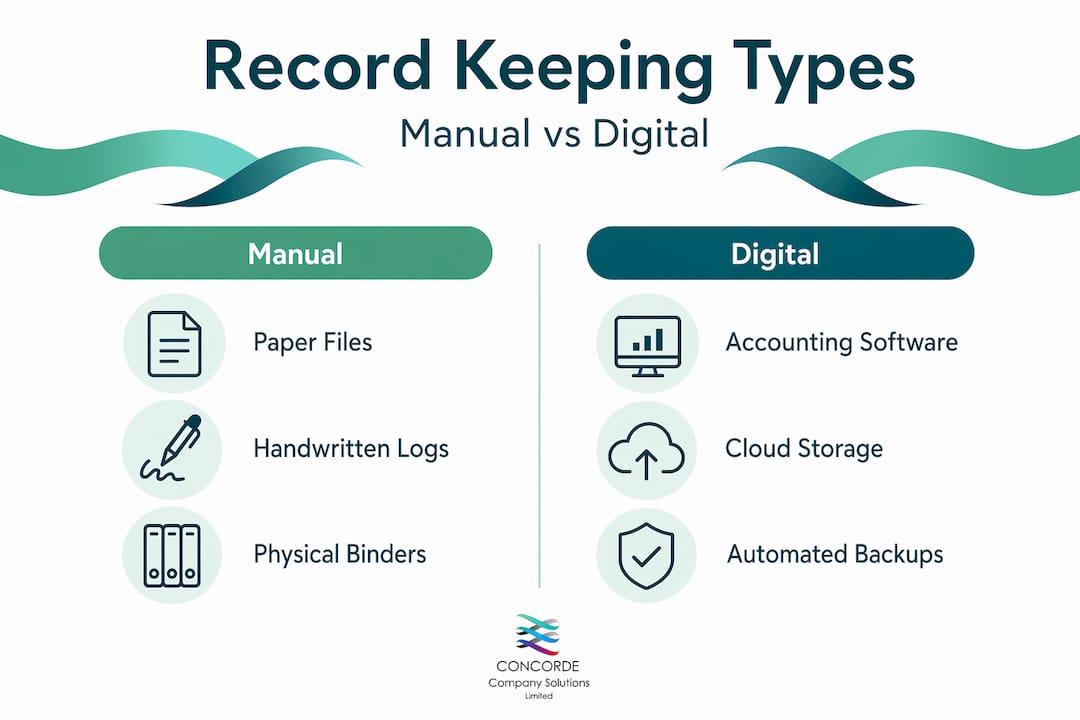

Manual versus digital record keeping

Most businesses now operate somewhere on a spectrum between fully paper-based and fully automated. The differences between these approaches are significant enough to affect your compliance, your costs, and your ability to grow.

Factor | Manual (paper-based) | Digital (software-based) |

Accuracy | Prone to human error and duplication | Automated checks reduce errors significantly |

Accessibility | Physical access required; easily lost or damaged | Available anywhere with appropriate permissions |

Security | Vulnerable to physical damage and theft | Encrypted storage with backup and access controls |

Cost | Low upfront, high long-term labour cost | Monthly subscription cost, lower ongoing admin time |

Scalability | Does not scale well as transaction volume grows | Scales without proportional increase in effort |

Integration | Requires manual transfer to other systems | Integrates with payroll, banking, and tax software |

Legal acceptability | Accepted by HMRC | Accepted by HMRC with appropriate backup |

The trend in UK accountancy is unmistakable. HMRC’s Making Tax Digital programme is progressively requiring businesses to keep digital records and submit returns through compatible software. If you are still relying on paper ledgers or disconnected spreadsheets, you are not just less efficient. You are heading toward a mandatory change on HMRC’s timeline rather than your own.

Automation and AI-assisted bookkeeping tools are also maturing quickly. They can categorise transactions, flag anomalies, and generate management reports with minimal manual input. The key is choosing software that integrates with your payroll, VAT submissions, and bank feeds rather than creating yet another siloed system.

My view on why businesses get this wrong

I’ve worked with enough small business owners to know that the resistance to proper record keeping is rarely laziness. It’s misplaced prioritisation. When you’re running a business, client work feels urgent and record keeping feels like it can wait. I’ve seen that thinking cost businesses thousands in disallowed deductions, failed audits, and loan applications that fell apart because the financials weren’t credible.

What I’ve learned is that businesses which treat their records as a strategic asset, not a compliance chore, are the ones that scale without chaos. They can answer questions about their performance instantly, spot problems before they escalate, and present themselves with confidence to banks, investors, and HMRC alike. Proper documentation transforms risk management from a reactive scramble into something deliberate and controlled.

The discipline is genuinely hard to sustain under business pressure. My advice is to make it structural rather than motivational. If reconciliation and document filing depend on you remembering to do them, they won’t happen consistently. Build them into your calendar, assign them to named people, and use software that does the heavy lifting. The businesses I’ve seen benefit most from good records are not the ones with the most sophisticated systems. They’re the ones with the most consistent habits.

Regulations will keep evolving, and HMRC’s digitalisation agenda is accelerating. Getting your records right now means you adapt on your terms rather than scrambling to catch up. That is worth far more than any individual tax saving.

— David

How Concordecompanysolutions can help

Keeping accurate records across payroll, VAT, and company accounts is straightforward in theory. In practice, it takes consistent attention that most business owners simply do not have time for.

Concordecompanysolutions works with small and medium-sized businesses across Yorkshire and beyond, providing payroll management that keeps your PAYE records accurate, compliant, and ready for any HMRC query. From bookkeeping and statutory accounts to software setup and company tax returns, the firm handles the documentation work that protects your business. If you want records that actually work for your business rather than just satisfying a legal minimum, get in touch with Concordecompanysolutions to find out how tailored support can make a real difference.

FAQ

How long must UK businesses keep financial records?

UK businesses must retain tax records for at least 7 years. Different document types carry varying minimum periods, with VAT records requiring 6 years and payroll records at least 3 years from the end of the relevant tax year.

What happens if a business fails to keep proper records?

HMRC can impose financial penalties for missing or incomplete records, and any unsupported deductions will be disallowed. Poor documentation also increases the risk of failed audits, rejected loan applications, and lost legal disputes.

Why keep business records beyond tax compliance?

Accurate records support cash flow management, budgeting, investor confidence, and dispute resolution. Businesses with consistent documentation can scale without losing institutional knowledge and make decisions based on reliable data rather than guesswork.

Are digital records accepted by HMRC?

Yes. HMRC accepts electronic records provided they are accurate, accessible, and backed up appropriately. Under the Making Tax Digital programme, digital record keeping is becoming a requirement rather than an option for most UK businesses.

What are proper record practices for a small business?

Proper record practices include maintaining a retention schedule, digitising documents, reconciling accounts monthly, separating business and personal finances, and assigning clear ownership for each document type. Consistency matters more than complexity.

Recommended

Comments