What is a trial balance? A clear guide for businesses

- David Rawlinson

- 2 hours ago

- 9 min read

TL;DR:

A balanced trial balance confirms that debits equal credits but does not guarantee accuracy.

It is an internal working document that can overlook omissions, principle errors, and fraud.

Most business owners and bookkeepers assume that a balanced trial balance means their accounts are correct. That assumption is wrong, and it costs people real money. Understanding what is a trial balance, what it actually confirms, and where it falls short is one of the most practically useful things you can do for your financial reporting. This guide covers the full trial balance explanation, from its structure and types through to preparation steps and the limitations that even experienced accountants sometimes overlook.

Table of Contents

Key takeaways

Point | Details |

Trial balance defined | A trial balance lists all general ledger balances to confirm total debits equal total credits. |

Three distinct types | Unadjusted, adjusted, and post-closing trial balances each serve a different stage of the accounting cycle. |

Balance does not mean accuracy | A balanced trial balance can still contain omissions, principle errors, and compensating mistakes. |

Preparation follows clear steps | Gather ledger balances, list them in two columns, total each, and investigate any discrepancy. |

Internal document only | A trial balance is a working document for internal use, not an external financial statement. |

What is a trial balance in double-entry bookkeeping

A trial balance is a list of general ledger balances at a specific point in time, presented in two columns: debits on the left, credits on the right. Its core function is to confirm that the total of all debit balances equals the total of all credit balances, which verifies the mathematical integrity of your double-entry bookkeeping system.

Every account in your general ledger feeds into the trial balance. That includes assets, liabilities, equity, revenue, and expense accounts, each displayed with its account number and closing balance. The structure is deliberate: debits and credits must always mirror each other because every transaction recorded under double-entry bookkeeping affects at least two accounts equally.

The purpose of trial balance preparation is to act as a preliminary checkpoint. Before you or your accountant prepares an income statement, balance sheet, or any other formal financial statement, the trial balance catches basic mathematical errors that could otherwise compound and distort your final reports. Think of it as the quality check before the finished product.

One thing to be clear about from the outset: a trial balance is strictly an internal document. It is not for external reporting and should not be shared with HMRC, investors, or banks as a financial statement. Its value lies entirely within your accounting workflow.

Pro Tip: If you are new to double-entry bookkeeping, make sure you understand how debits and credits work across different account types before relying on a trial balance as a check. An error in your classification rules will produce a balanced trial balance that is fundamentally wrong.

The key components of a well-structured trial balance include:

Account names and reference numbers for every active ledger account

The closing debit or credit balance for each account

A total row for the debit column and the credit column separately

A clear date indicating the period end the balances relate to

The three types of trial balance

Understanding trial balance types matters because each one serves a distinct purpose at a different point in the accounting cycle. Treating them as interchangeable leads to confusion and errors in financial reporting.

Unadjusted trial balance. This is the first trial balance you prepare at the end of a reporting period. It captures the raw ledger balances before any adjusting entries are made. At this stage, accruals, prepayments, and depreciation have not yet been accounted for, so the figures reflect recorded transactions only. It is your starting point, not your finishing line.

Adjusted trial balance. Once you have processed all adjusting entries (accruals for income earned but not yet invoiced, deferrals for expenses paid in advance, depreciation on fixed assets), you run the adjusted trial balance. This version prepares accurate financial statements because it reflects economic reality, not just cash movements. The adjusted trial balance is the one your accountant will use to produce your income statement and balance sheet.

Post-closing trial balance. After the period-end financial statements are finalised, temporary accounts (revenue, expenses, and drawings) are closed off to retained earnings or owner’s equity. The post-closing trial balance confirms that only permanent accounts remain open and that the ledger is in the correct state to begin the new accounting period. It verifies ledger readiness before the next cycle starts.

Each type builds on the previous one. Skipping the unadjusted version and jumping straight to adjustments is like editing a document before you have written it. The sequence matters.

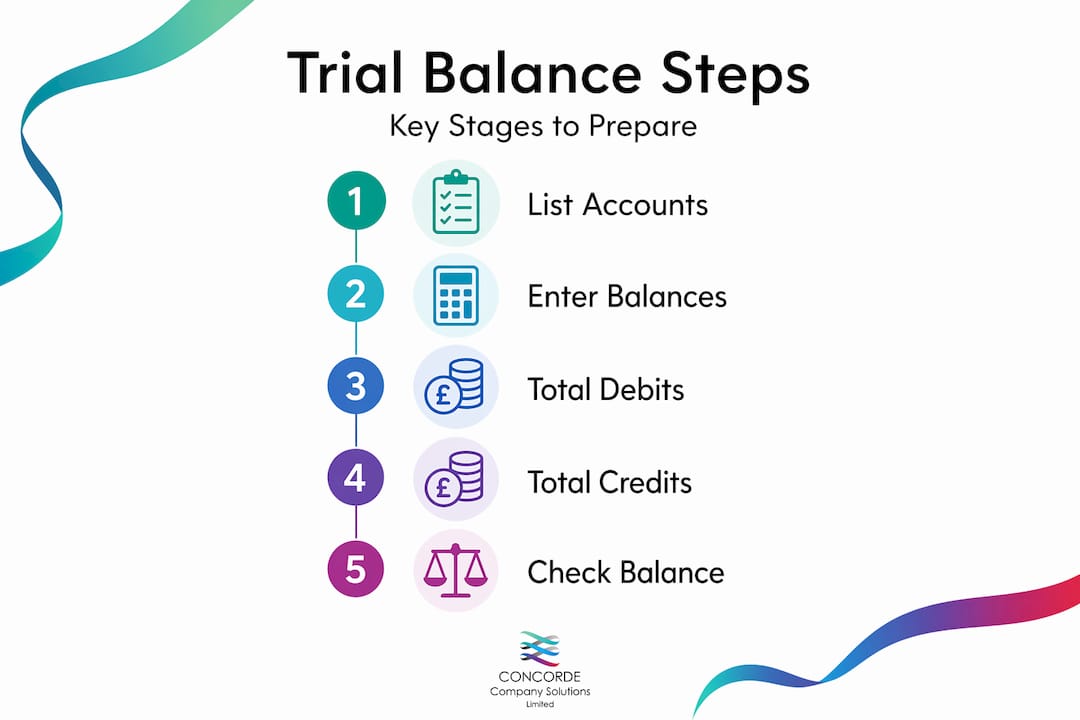

How to prepare a trial balance

Preparing a trial balance is a methodical process. Accuracy depends on clean source data, so the quality of your ledger entries directly determines how useful the trial balance will be. Here is how to prepare a trial balance correctly:

Step 1: Gather all ledger account balances. Pull the closing balance for every active account in your general ledger at the period end. This typically happens monthly, quarterly, or annually, depending on your reporting cycle.

Step 2: Classify each balance. Determine whether each account carries a debit or credit balance. Assets and expenses normally carry debit balances. Liabilities, equity, and revenue normally carry credit balances.

Step 3: List accounts in two columns. Place debit balances in the left column and credit balances in the right. Account for every active ledger account, even those with a nil balance.

Step 4: Sum each column. Add all debit balances to produce a single total. Do the same for credit balances. The two totals must agree.

Step 5: Investigate any difference. If the columns do not agree, you have a posting error somewhere. Do not move forward until you find it.

Pro Tip: When your trial balance is out of balance, two diagnostic checks save significant time. If the difference is divisible by 9, look for a transposition error (where digits have been accidentally swapped, such as 654 entered as 645). If the difference is divisible by 2, a debit entry has likely been posted to the credit column or vice versa.

Good bookkeeping best practices make trial balance preparation far quicker. When ledger entries are coded correctly and reconciled regularly throughout the period, end-of-period errors are far less common.

Limitations of the trial balance

Here is where many people develop a dangerous misunderstanding. A trial balance that balances perfectly does not mean your books are correct. It means your debits equal your credits. Those are not the same thing.

A balanced trial balance does not guarantee accuracy. There are several categories of error it simply cannot detect:

Error type | Why the trial balance misses it |

Error of omission | A transaction was never recorded. Both debit and credit were skipped, so the balance is unaffected. |

Error of principle | A transaction was recorded in the wrong type of account (e.g., capital expenditure posted as revenue). Debits still equal credits. |

Compensating errors | Two separate errors cancel each other out mathematically, leaving totals equal despite underlying mistakes. |

Error of original entry | The wrong amount was entered for both the debit and credit. The balance agrees but the figure is wrong. |

Posting to the wrong account | A payment posted to the wrong supplier account leaves the trial balance balanced but the individual account incorrect. |

“A trial balance only confirms arithmetic consistency. It tells you nothing about whether transactions were recorded correctly, completely, or in the right accounts.”

Beyond these structural limitations, trial balances cannot detect fraud. A fraudulent transaction that debits one account and credits another in equal measure will leave the trial balance perfectly balanced. Detecting fraud requires internal controls, segregation of duties, and audit procedures that operate well beyond the trial balance.

This is why bank reconciliations and analytical reviews are not optional extras. They are the controls that catch what the trial balance cannot. Understanding trial balance limitations is not pessimistic. It is what separates a capable bookkeeper from one who gives their client false assurance.

Using trial balances effectively in your business

The trial balance earns its place in your accounting workflow when you treat it as the beginning of a review process, not the end of one. Here is how accountants and business owners can put it to practical use:

Financial statement preparation. The adjusted trial balance supports preparation of the income statement, balance sheet, and statement of cash flows. Running it before you start drafting those statements prevents basic errors from appearing in your final reports.

Pre-audit review. Before an external audit or HMRC compliance check, a clean and reconciled trial balance demonstrates that your records are in order and speeds up the process considerably. Poor trial balance discipline is one of the most common reasons audits take longer than they should.

Spotting bookkeeping mistakes early. Monthly trial balance runs catch data entry errors while they are still fresh and easy to trace. Waiting until year-end means you are investigating errors from eleven months ago.

Tax filing preparation. Accurate trial balance figures feed directly into your corporation tax return. An error in your trial balance is an error in your tax return. Connecting your trial balance to tax accuracy is not just good practice; it reduces your risk of HMRC enquiries.

Software integration. Modern accountancy software generates trial balances automatically from your ledger data, which reduces manual errors significantly. That said, human judgement remains vital for reviewing the output, identifying unusual balances, and confirming that classifications are correct.

The trial balance is also a useful management tool. Reviewing it monthly gives you a high-level view of your business’s financial position that helps you make informed decisions between formal reporting periods.

My honest take on the trial balance

I have worked with businesses that treat a balanced trial balance as a green light to close the books and move on. In my experience, that is exactly the mindset that leads to year-end surprises.

What I have learned over years of practical accounting work is this: the trial balance is a necessary condition, not a sufficient one. It tells you that your double-entry mechanics are working. It does not tell you that your business’s finances are accurately represented. The most consequential errors I have seen, including misclassified capital expenditure, missing accruals, and transactions posted to entirely the wrong client accounts, all existed inside perfectly balanced trial balances.

My advice is to treat the trial balance as your first filter, not your last. Pair every trial balance review with a scan of unusual account movements, a comparison to prior periods, and a bank reconciliation. That combination catches far more than the trial balance ever will on its own. Technology has made trial balance preparation faster and largely automatic, which is genuinely useful. But the value of a qualified professional reviewing the output, asking the right questions, and spotting what does not look right is something software has not replaced yet.

— David

How Concordecompanysolutions can support your bookkeeping

At Concordecompanysolutions, we work with small and medium-sized businesses, sole traders, and limited companies across Leeds and beyond to keep their financial records accurate and compliant. From payroll management to full bookkeeping and statutory accounts, our team handles the detail so you can focus on running your business. Getting your trial balance right is part of a broader system of financial control, and that is exactly what we help you build. If your accounts need a professional set of eyes, get in touch with us directly and we will talk through the support that fits your situation.

FAQ

What does a trial balance show?

A trial balance lists ending balances for all general ledger accounts and confirms that total debits equal total credits, verifying the mathematical accuracy of your double-entry records.

Does a balanced trial balance mean no errors?

No. A balanced trial balance can still miss errors of omission, principle, and original entry, as well as compensating errors where two mistakes cancel each other out.

What is the difference between a trial balance and a balance sheet?

A trial balance is an internal working document listing all ledger balances as a preliminary accuracy check. A balance sheet is a formal financial statement showing assets, liabilities, and equity at a period end, intended for external reporting.

How often should you prepare a trial balance?

Most businesses prepare a trial balance monthly, quarterly, and at the financial year end. Monthly preparation is best practice because it catches errors while they are still straightforward to trace and correct.

Can a trial balance detect fraud?

No. Fraudulent transactions can keep debits and credits equal, leaving the trial balance balanced. Fraud detection requires internal controls, segregation of duties, and independent audit procedures.

Recommended

Comments