Business bank reconciliation: clarity for UK SMEs

- David Rawlinson

- 16 hours ago

- 7 min read

TL;DR:

Regular monthly bank reconciliation is essential for legal compliance, fraud prevention, and accurate tax reporting.

Discrepancies in records, such as timing differences and unrecorded fees, require ongoing investigation and documentation.

Consistent reconciliation reduces errors, HMRC audit risk, and correction costs, ensuring audit-ready financial records.

Your online bank balance feels reassuring. You check it, the numbers look reasonable, and you move on. But that balance tells you nothing about uncleared cheques, unrecorded fees, duplicate transactions, or VAT mismatches sitting quietly in your records. For UK small businesses and sole traders, accurate bookkeeping reconciliation is not a nice-to-have detail. It is a legal safeguard, a fraud deterrent, and the foundation of every tax return you submit to HMRC. This guide walks you through what bank reconciliation actually involves, why it matters far more than most business owners realise, and how to do it properly without losing hours every month.

Table of Contents

Key Takeaways

Point | Details |

Compliance essential | Accurate bank reconciliation is crucial to meet HMRC tax and VAT requirements in the UK. |

Monthly checks cut risk | Reconciling every month reduces errors and lowers your chances of costly HMRC enquiries. |

Avoid common pitfalls | Recognising issues like timing errors and duplicate bank feed entries helps maintain financial accuracy. |

Automate with caution | Digital tools speed up reconciliation but must be matched with careful manual review. |

What is business bank reconciliation?

Bank reconciliation is the process of comparing your internal financial records against your official bank statement to confirm they match. Every transaction you have recorded in your bookkeeping software or ledger should correspond to a real transaction on your bank statement. When they do not match, that gap is a discrepancy, and discrepancies need investigating.

Who needs to do this? Essentially every business that reports to HMRC. That includes limited companies, partnerships, sole traders filing Self Assessment, and any VAT-registered business operating under Making Tax Digital (MTD) for VAT. If money moves through your business account, reconciliation applies to you.

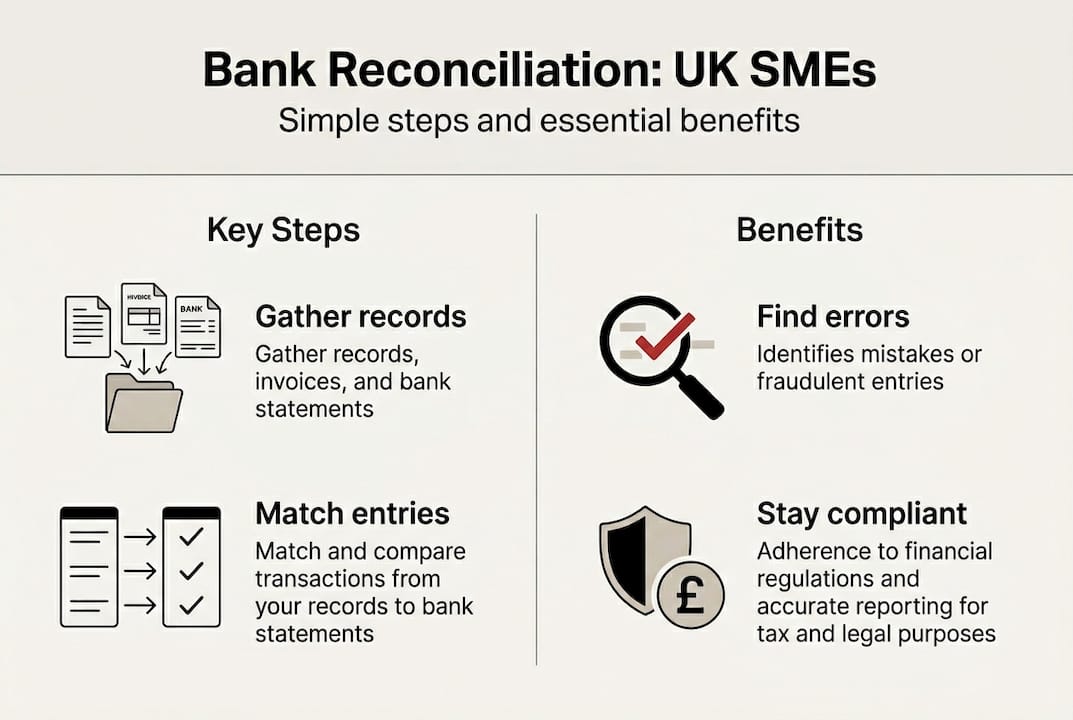

The core process involves three stages:

Collect your records: Gather your bank statement for the period alongside your internal ledger, bookkeeping software export, or spreadsheet.

Match every transaction: Go line by line, ticking off payments and receipts that appear in both places.

Investigate and document differences: Timing differences, missing entries, or bank charges that were not recorded all need a clear note and resolution.

Because bank reconciliation is essential for HMRC compliance and tax accuracy, it also feeds directly into your VAT returns and annual accounts. Errors left unresolved here can cascade into your tax submissions.

Pro Tip: Automate your bank feed imports through software like Xero or QuickBooks, but never skip the manual review. Automation speeds up matching; it does not replace your judgement when something looks off.

Why bank reconciliation is crucial for compliance and fraud prevention

Leaving reconciliation until year-end is one of the most expensive habits a small business can develop. The difference between monthly and annual reconciliation is not just administrative. It is financial.

Reconciliation frequency | Error detection | Audit risk | Correction cost |

Monthly | High | Low | Minimal |

Quarterly | Moderate | Moderate | Moderate |

Annual | Low | High | Significant |

Monthly reconciliation prevents 75% of errors, and businesses that reconcile monthly face an HMRC enquiry rate of around 3%, compared to roughly 12% for those who reconcile annually. That is a stark difference in risk exposure.

Fraud is the other side of this coin. The median small business fraud goes undetected for 18 months. Regular reconciliation is often the only internal control that catches it early. Duplicate payments, fictitious suppliers, and unauthorised transfers all leave traces in the gap between your records and your bank statement.

“Timely reconciliation does not just keep your books tidy. It is the earliest warning system your business has against both internal errors and external fraud.”

HMRC also requires six-year retention of records, including reconciliations. If you face an enquiry and cannot produce reconciled records, you are exposed to penalties and interest, even if your tax figures happen to be correct. Strong audit risk prevention starts with consistent, documented reconciliation.

The practical benefits are clear:

Cashflow figures you can actually trust

VAT returns built on verified data

A clean paper trail if HMRC ever asks questions

Early detection of bank errors or fraudulent activity

Common reconciliation problems and how to solve them

Even diligent business owners run into reconciliation headaches. Knowing the most common bookkeeping edge cases saves time and prevents avoidable mistakes.

The most frequent problems, in order of how often they appear:

Timing differences: A payment you recorded has not yet cleared the bank, or a deposit is in transit. These are not errors, but they must be documented clearly.

Unrecorded bank fees and interest: Banks charge fees quietly. If you have not set up a rule to capture these automatically, they create a recurring gap.

Duplicate transactions from bank feeds: Automated imports sometimes pull the same transaction twice. Always scan for identical amounts on identical dates.

Transposition errors: You typed £1,890 instead of £1,980. A useful trick: if the difference between your records and the bank statement is divisible by 9, a transposition error is likely the cause.

VAT misclassification: Treating an exempt supply as zero-rated, or vice versa, creates a mismatch that only surfaces at reconciliation time.

Error type | Common cause | Corrective action |

Timing difference | Cheque not yet cleared | Note and carry forward |

Unrecorded fee | No bank feed rule | Add rule; post manually |

Duplicate entry | Bank feed import glitch | Delete duplicate; verify |

Transposition error | Manual data entry | Check if diff divisible by 9 |

VAT misclassification | Incorrect tax code | Correct code; amend return if needed |

For ongoing accuracy, reviewing bookkeeping best practices regularly helps you stay ahead of these issues. Understanding what HMRC compliance means for your specific business type also clarifies which records must be spotless.

Pro Tip: Always verify your opening balance before you start reconciling a new period. If the opening balance is wrong, every figure that follows will be wrong too.

How to carry out effective bank reconciliation (step-by-step guide)

A reliable routine removes the stress from reconciliation entirely. Follow these steps each month and you will always be audit-ready.

Collect your bank statement and internal records for the same period. Download your bank statement as a PDF or CSV. Export your transactions from your bookkeeping software.

Verify the opening balance. Confirm it matches last month’s closing balance in both your records and the bank statement before you do anything else.

Match every transaction line by line. Tick off each payment and receipt that appears in both places. Use your software’s matching tool where available.

Investigate every unmatched item. Is it a timing difference? An unrecorded fee? A duplicate? Each one needs a written note explaining what it is and how it will be resolved.

Reconcile VAT and HMRC-specific figures. Cross-check your VAT account against what you have submitted or plan to submit. Any mismatch here needs correcting before your next return.

Export and retain your reconciliation report. Save it alongside your bank statement and supporting invoices. HMRC requires these records for six years.

For sole trader tax returns and business tax return preparation, monthly reconciliation keeps records audit-ready and meets VAT and Self Assessment demands without last-minute scrambles.

Records to retain each month:

Bank statements (original downloads)

Reconciliation report from your software

Invoices and receipts for all transactions

Notes on any unresolved items and their outcomes

If you want to estimate the time and cost savings from switching to monthly reconciliation, a monthly savings calculator can help you put a real number on the difference.

Pro Tip: Set a recurring calendar reminder for the same date each month, ideally within the first week after your bank statement closes. Consistency is what makes reconciliation fast and painless.

Why monthly reconciliation makes UK SMEs truly audit-ready

Most business owners treat reconciliation as a chore to survive rather than a habit that protects them. We see this regularly, and it consistently costs more than the time saved by avoiding it.

The uncomfortable truth is that monthly reconciliations reduce HMRC audit rates and cut correction costs significantly because errors are caught when they are still small and simple to fix. A sole trader who leaves reconciliation until January, facing twelve months of bank feeds, missing receipts, and forgotten transactions, does not just face a stressful evening. They face potential errors on their Self Assessment return and the real possibility of an HMRC enquiry.

Contrast that with a business owner who spends forty minutes in reconciliation each month. By year-end, their records are clean, their VAT submissions are verified, and an HMRC enquiry would be an inconvenience rather than a crisis.

The smartest move is to integrate reconciliation with your other monthly routines. Pair it with streamlining your payroll run and your monthly budget review. When these tasks happen together, they reinforce each other and nothing slips through the gaps.

Ensure peace of mind with expert financial support

Sound reconciliation is achievable for any business, but it is far easier when you have the right support behind you.

At Concorde Company Solutions, we work with small businesses and sole traders across the UK to take the pressure off financial management. From payroll solutions that integrate seamlessly with your monthly routines, to bookkeeping support that keeps your records HMRC-ready throughout the year, we handle the detail so you can focus on running your business. As SME compliance experts, we understand the specific obligations facing UK businesses in 2026 and can tailor our support to your situation. Get in touch to find out how we can simplify your financial processes and give you genuine confidence in your numbers.

Frequently asked questions

How often should a UK small business reconcile its bank statements?

Monthly reconciliation is strongly recommended, particularly for VAT-registered businesses. Monthly checks prevent 75% of errors and reduce the likelihood of an HMRC enquiry significantly compared to annual reconciliation.

What documents must SMEs keep to prove bank reconciliation for HMRC?

You must retain bank statements, reconciliation reports, and supporting invoices for six years as required by HMRC. Gaps in this documentation can create problems during an enquiry even if your tax figures are broadly correct.

What is the most common error in business bank reconciliation?

Timing differences, unrecorded bank fees, and duplicate transactions from bank feeds are the most frequent issues. Most can be prevented with consistent monthly checks and well-configured bank feed rules.

What happens if I forget to reconcile my business account before submitting a tax return?

Unreconciled records increase the risk of errors on VAT or Self Assessment returns, which can trigger penalties or HMRC audits. Correcting mistakes after submission is far more time-consuming and costly than preventing them through regular reconciliation.

Recommended

Comments