How to File Company Accounts for UK Businesses Easily

- David Rawlinson

- Dec 16, 2025

- 7 min read

Most British companies face strict deadlines when filing their annual accounts, and missing these requirements can lead to costly penalties. Organizing financial records and ensuring each document is complete matters more than many business owners realize. With the transition to mandatory digital filing just a few years away, understanding the full process is essential for every British company aiming to stay compliant and avoid unnecessary stress.

Table of Contents

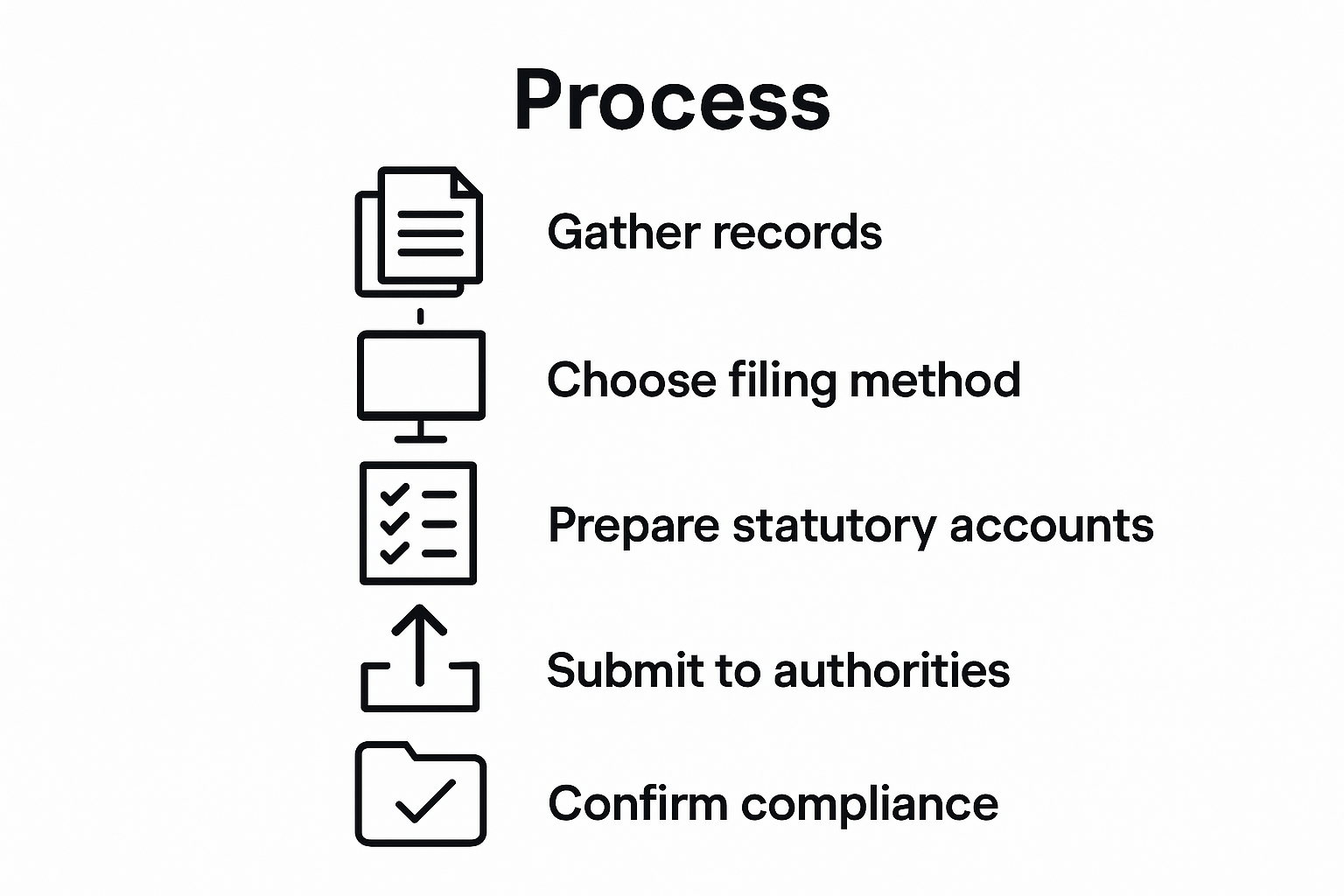

Quick Summary

Key Point | Explanation |

1. Collect all necessary records | Assemble vital financial documents like balance sheets and receipts for accuracy. |

2. Choose suitable filing methods | Evaluate filing options, focusing on software that meets regulatory standards. |

3. Ensure accurate statutory accounts | Compile detailed accounts, adhering to legal requirements and verifying all entries. |

4. Submit on time to relevant authorities | File accounts to Companies House and HMRC by set deadlines to avoid penalties. |

5. Verify and maintain compliance | Confirm receipt of submissions and keep records organised for future reference. |

Step 1: Gather Necessary Financial Records and Documentation

Preparing your company’s annual accounts starts with assembling a comprehensive set of financial documents. Your goal is to collect every critical record that demonstrates your company’s financial performance with precision and clarity.

Start by gathering essential financial records including your company’s balance sheet, profit and loss accounts, cash flow statements, bank statements, expense receipts, invoices, payroll records, and tax documentation. Small companies have specific requirements for financial statement compilation, so ensure you understand the exact documentation needed for your business size. Consider creating a dedicated folder or digital repository to organise these documents systematically.

Key financial records should cover the entire accounting period and include supporting evidence for all transactions. This means collecting receipts, contracts, payroll records, bank statements, purchase invoices, sales records, and any other financial documentation that provides a transparent view of your company’s monetary activities. Maintain meticulous records to streamline the accounting process and demonstrate financial accountability.

Pro tip: Create a digital backup of all financial documents using secure cloud storage or an encrypted external hard drive. This ensures you have a redundant copy of critical records in case of physical document loss or damage.

Here’s a summary of key financial records and their importance in preparing annual accounts:

Record Type | Main Purpose | Consequence if Missing |

Balance Sheet | Shows assets, liabilities, and equity | Incomplete financial overview |

Profit and Loss | Reports income and expenses | Obscured profitability assessment |

Bank Statements | Verifies cash flow and transactions | Gaps in transaction validation |

Payroll Records | Tracks staff costs and PAYE compliance | Risk of tax and salary errors |

Invoices & Receipts | Evidence for sales and purchases | Difficulty substantiating transactions |

Tax Documentation | Supports tax return and compliance | Potential HMRC scrutiny |

Step 2: Select the Appropriate Filing Method and Format

Choosing the right filing method is crucial for submitting your company accounts efficiently and compliantly. UK companies are transitioning towards mandatory commercial software filing beginning 1 April 2027, which means understanding your current and future filing options is essential.

Currently, you have multiple filing routes available through Companies House WebFiling service or traditional postal submission. However, prepare for the upcoming digital transformation by selecting software that meets HMRC and Companies House requirements. Look for accounting software that can generate compatible digital accounts files, supports automatic digital submissions, and provides robust record-keeping features. Consider factors like your company size, complexity of financial records, and budget when selecting an appropriate filing solution.

Ensure your chosen filing method provides comprehensive documentation support and generates accounts in the standard iXBRL format required by regulatory bodies. Research various commercial accounting software options that offer seamless digital filing capabilities and integrate well with your existing financial management systems.

Pro tip: Start exploring and testing digital filing software at least six months before the mandatory transition to ensure a smooth adaptation to the new filing requirements.

The table below compares current and future company accounts filing options in the UK:

Filing Method | Format Required | Key Benefit | Limitation |

WebFiling | Online Forms | Simple for small companies | Limited customisation |

Postal Submission | Paper | No software needed | Slower and processing delays |

Commercial Software (future) | iXBRL | Automated, compliant filings | Software cost and need for adaptation |

Step 3: Complete Statutory Accounts Accurately

Compiling accurate statutory accounts is a critical responsibility for company directors, requiring meticulous attention to financial details and legal compliance. Statutory accounts must comprehensively include a balance sheet, profit and loss account, and supporting notes, ensuring a transparent representation of your company’s financial position.

Small companies must prepare accounts that adhere to the Companies Act 2006 and applicable accounting standards, which means carefully documenting all financial transactions and ensuring mathematical precision. Begin by reviewing all financial records, cross-referencing bank statements, reconciling accounts, and verifying every monetary entry. Pay special attention to categorising expenses, recording income streams, and documenting any significant financial events or adjustments that occurred during the accounting period.

Each section of your statutory accounts requires careful compilation. The balance sheet should reflect your company’s assets, liabilities, and shareholders’ equity with absolute accuracy. The profit and loss account must detail your revenue, expenses, and net financial performance. Accompanying notes should provide context for any unusual transactions, accounting policies, and additional financial insights that help stakeholders understand your company’s economic landscape.

Pro tip: Consider engaging a professional accountant to review your statutory accounts before final submission to catch any potential errors and ensure full regulatory compliance.

Step 4: Submit Accounts to Companies House and HMRC

Submitting your company accounts to Companies House and HMRC is a crucial final step in maintaining your business’s financial compliance. Understanding the specific submission deadlines and requirements will help you avoid potential penalties and ensure smooth regulatory reporting.

Overseas companies with a UK establishment must follow precise filing protocols when submitting their financial documentation. Private companies are required to file annual accounts with Companies House within nine months of their accounting reference date, while the Company Tax Return must be submitted to HMRC within 12 months of the accounting period’s conclusion. Prepare digital copies of all necessary documents, including your balance sheet, profit and loss account, and supporting notes. Double check that your files are in the correct format typically iXBRL for digital submissions and ensure all financial information is accurate and consistent across different documents.

When submitting your accounts, create a systematic approach by gathering all required documentation in advance. Verify your Companies House authentication credentials, ensure your digital filing software is compatible with their submission requirements, and have all relevant financial statements ready. For HMRC submissions, compile your tax calculations, income details, and any supplementary financial information that supports your tax return.

Pro tip: Set digital reminders three months before each submission deadline to provide ample time for document preparation and review, preventing last minute stress and potential late filing penalties.

Step 5: Verify Successful Submission and Maintain Compliance

After submitting your company accounts, confirming successful filing is crucial to maintaining regulatory compliance. Understanding the verification process will help you avoid potential penalties and ensure your business remains in good standing with official bodies.

Companies must carefully follow submission guidelines and track their filing status to prevent any administrative complications. Begin by checking the official confirmation emails from Companies House and HMRC, which typically arrive within 24 to 48 hours after submission. Cross reference these confirmations with your own digital records and ensure all submitted documents match your internal financial statements. Pay special attention to any reference numbers or submission acknowledgements, as these will be critical if you need to reference your filing in future communications.

Establish a systematic approach to compliance by creating a dedicated folder for all submission confirmations, tax correspondence, and regulatory communications. Set up digital notifications to track upcoming filing deadlines, and consider maintaining a compliance calendar that highlights key dates for annual accounts, tax returns, and other statutory requirements. Regular monitoring and proactive management will help you stay ahead of potential administrative challenges and demonstrate your commitment to financial transparency.

Pro tip: Create a digital archive of all submission confirmations and store them in a secure, easily accessible location with multiple backup copies to protect against potential future administrative queries.

Simplify Your UK Company Accounts Filing with Expert Support

Filing annual company accounts can feel overwhelming, especially with strict deadlines and the shift towards mandatory digital submissions using iXBRL format. Common challenges like organising detailed financial records, ensuring statutory compliance, and meeting HMRC and Companies House requirements can create stress and risk penalties. By partnering with professionals who understand these complexities, you gain confidence that every balance sheet, profit and loss account, and supporting note is completed with accuracy and care.

Don’t let administration headaches hold your business back. At Concorde Company Solutions, we offer tailored accounting services including statutory accounts preparation, tax return filings, payroll management, and bookkeeping to keep your finances transparent and compliant. Explore how our personalised support and transparent pricing can take the burden off your hands and help you navigate the transition to digital filing smoothly. Visit our accounting services page today and secure peace of mind before your next deadline approaches.

Frequently Asked Questions

What documents do I need to prepare my company accounts?

To prepare your company accounts, gather essential financial records such as the balance sheet, profit and loss accounts, cash flow statements, bank statements, expense receipts, invoices, payroll records, and tax documentation. Focus on ensuring you have documentation covering the entire accounting period and maintain meticulous records to streamline your accounting process.

How can I choose the right filing method for my company accounts?

Select a filing method that aligns with your company’s size and needs. Consider options like online filing through a dedicated service or postal submission, and explore appropriate commercial accounting software that meets HMRC and Companies House requirements to ensure compliance and ease of filing.

What are statutory accounts and why are they important?

Statutory accounts are comprehensive financial reports required by law, including a balance sheet, profit and loss account, and supporting notes. Accurately compiling these accounts ensures transparent financial representation and compliance with regulatory standards, which is crucial for maintaining your business’s credibility.

How do I submit my company accounts to Companies House and HMRC?

To submit your company accounts, ensure you have all necessary documents in the correct format, typically iXBRL for digital submissions. Follow submission guidelines closely and ensure you meet the respective deadlines to avoid penalties, submitting within nine months for Companies House and twelve months for HMRC once your accounting period ends.

How can I confirm the successful submission of my company accounts?

After submitting your accounts, check for official confirmation emails from Companies House and HMRC, which should arrive within 24 to 48 hours. Keep records of these confirmations and cross-reference them with your own financial documents to ensure consistency and tackle any potential issues proactively.

Recommended

Comments