Financial Year End – Key Impacts for UK Businesses

- David Rawlinson

- Dec 17, 2025

- 8 min read

Being a british business owner means keeping up with strict financial obligations set by United Kingdom regulators. Every year, over 60 percent of limited companies face fines due to missed deadlines or incomplete reporting. The financial year end is far more than just a calendar date. Understanding what it means, how it affects tax and compliance, and how to avoid penalties gives british companies a crucial advantage in staying profitable and protected.

Table of Contents

Key Takeaways

Point | Details |

Financial Year End Significance | The financial year end marks a crucial deadline for financial reporting and regulatory compliance, impacting tax responsibilities and submission timelines. |

Flexibility in Financial Year Ends | UK businesses can choose between a standard or custom financial year end, influencing tax planning and administrative processes. |

Key Reporting Deadlines | Companies must adhere to strict deadlines, including filing annual accounts within 9 months post year end and Corporation Tax payment due within 9 months and 1 day. |

Common Compliance Mistakes | Businesses should implement robust tracking systems to avoid penalties associated with missed filing dates and notification procedures. |

What Financial Year End Means in the UK

In the United Kingdom, a company’s financial year end represents the crucial annual milestone that determines its accounting and tax reporting period. This date, officially known as the accounting reference date, marks the conclusion of a business’s financial reporting cycle and plays a pivotal role in regulatory compliance. For most organisations, the financial year end typically corresponds to the last day of the month in which the company was initially incorporated, unless specifically altered with Companies House.

The significance of the financial year end extends far beyond a simple calendar demarcation. It establishes critical deadlines for submitting essential financial documentation, including annual accounts to Companies House and the corresponding Company Tax Return to Her Majesty’s Revenue and Customs (HMRC). Each limited company must prepare comprehensive financial statements covering their entire accounting period, which provides a transparent snapshot of the organisation’s fiscal performance and health.

For new businesses, the initial financial year end is automatically determined by the last day of the month coinciding with the first anniversary of incorporation. This standardised approach ensures consistency and provides clear guidance for emerging enterprises navigating their initial reporting requirements. Companies have some flexibility in adjusting their accounting reference date, though this process involves specific procedural steps and potential implications for tax calculations and reporting timelines.

Pro Tip for Business Owners: Maintain meticulous financial records throughout the year to simplify your year-end reporting process and ensure smooth, stress-free compliance with HMRC and Companies House requirements.

Types of Financial Year End and How They Differ

Business owners in the United Kingdom have multiple options for structuring their financial year end, with flexibility that allows organisations to align their accounting periods strategically. Companies can choose their financial year end to suit their specific business cycles, providing a tailored approach to financial reporting and tax management.

Traditionally, most businesses default to the standard financial year end, which corresponds to the last day of the month matching their incorporation anniversary. However, limited companies possess the capability to modify this period, with the ability to shorten or extend their accounting year within specific regulatory parameters. These adjustments can be particularly beneficial for organisations seeking to synchronise their reporting with parent companies, seasonal business patterns, or more complex corporate structures.

The implications of selecting different financial year end types extend beyond administrative convenience. Each variation can significantly impact tax calculations, reporting deadlines, and overall financial planning. When a company decides to change its accounting reference date, it must formally notify Her Majesty’s Revenue and Customs (HMRC), as this modification directly influences Corporation Tax accounting periods and associated filing requirements. Smaller enterprises and startups should carefully evaluate their operational needs and potential tax consequences before making such a strategic decision.

Pro Tip for Financial Planning: Consult with a professional accountant before changing your financial year end to understand the precise tax implications and ensure seamless compliance with HMRC regulations.

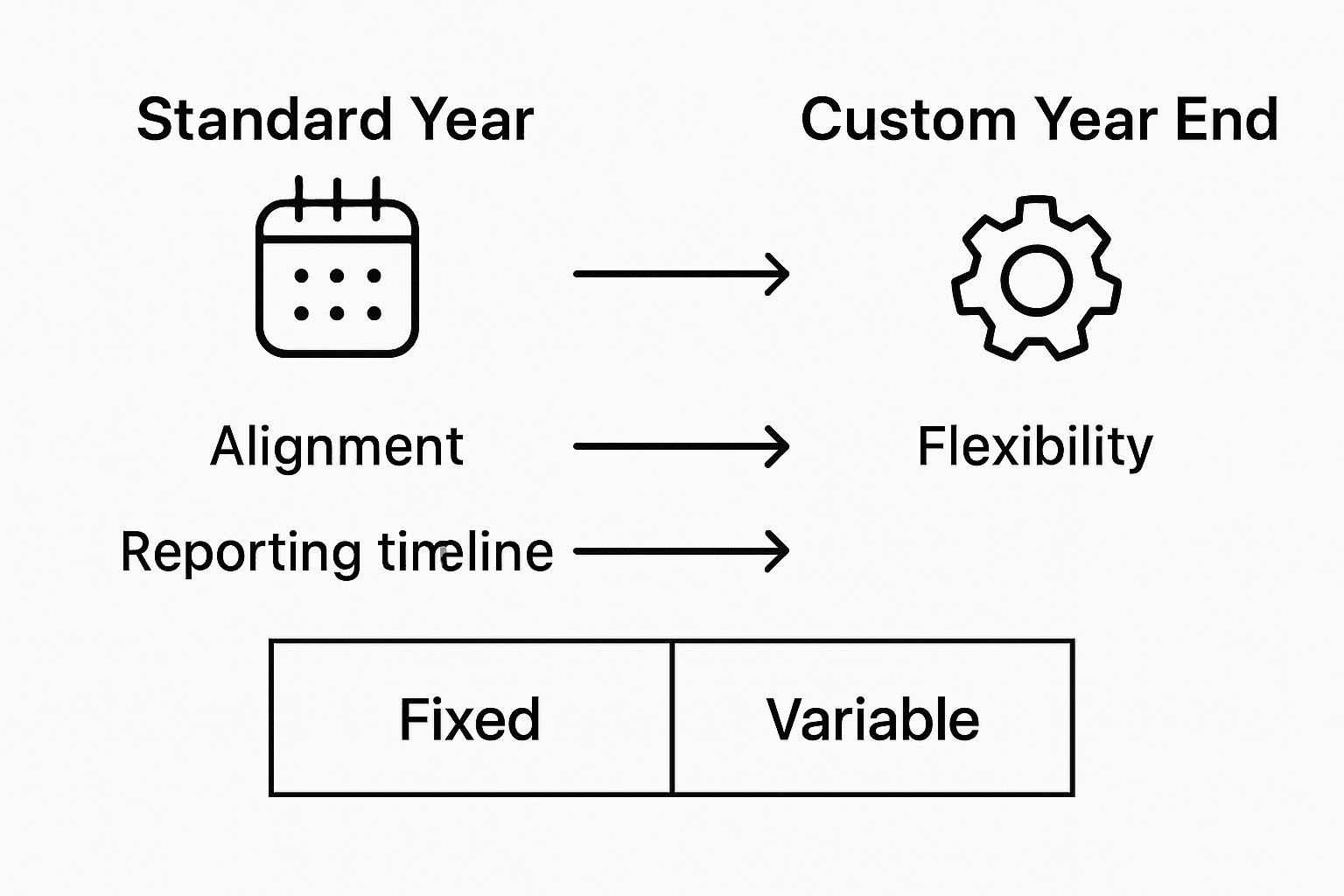

Here is a comparison of standard versus custom financial year ends for UK businesses:

Criteria | Standard Year End | Custom Year End |

Alignment with incorporation | Matches month of incorporation | Chosen by the business |

Administrative complexity | Straightforward to manage | More procedural steps required |

Flexibility | Limited to default date | Can be tailored to business needs |

Impact on tax planning | Less flexibility for optimisation | Can improve tax efficiency if well planned |

Key Deadlines and Statutory Obligations Explained

UK businesses must navigate a complex landscape of statutory reporting requirements that demand strict adherence to specific timelines and regulatory obligations. Companies must file their first accounts within precise timeframes, with new organisations required to submit documentation to Companies House within 21 months of incorporation. Subsequent annual accounts must be filed within 9 months of the financial year end, creating a critical compliance window that demands meticulous planning and organisation.

The Corporation Tax landscape presents additional critical deadlines that businesses must carefully manage. The standard accounting period typically spans 12 months, with companies obligated to pay their Corporation Tax within 9 months and 1 day after the conclusion of their accounting period. These timelines are not merely administrative suggestions but legally mandated requirements that carry significant financial and legal consequences for non-compliance. Limited companies, sole traders, and partnerships must maintain robust record-keeping systems to ensure they can meet these stringent reporting deadlines effectively.

Beyond the primary filing requirements, businesses must also consider additional statutory obligations that accompany financial year-end processes. This includes preparing comprehensive annual accounts, generating detailed financial statements, and ensuring all documentation accurately reflects the organisation’s financial performance. Small and medium-sized enterprises must be particularly vigilant, as missing these deadlines can result in substantial penalties, potential legal complications, and potential strikes against the company’s good standing with regulatory bodies.

Pro Tip for Compliance Management: Develop a comprehensive calendar tracking all key financial reporting deadlines at least six months in advance, allowing ample time for preparation, review, and submission of required documentation.

This table summarises key statutory deadlines and their implications for UK companies:

Requirement | Deadline | Consequence of Missing |

First accounts to Companies House | Within 21 months of incorporation | Financial penalties; potential strike-off |

Annual accounts filing | 9 months post year end | Late fines, regulatory scrutiny |

Corporation Tax payment | 9 months 1 day post accounting period | Interest charges and penalties |

How Year End Affects Tax, Accounts, and HMRC Compliance

The financial year end represents a critical juncture for UK businesses, fundamentally influencing their tax reporting and regulatory compliance. The accounting period for Corporation Tax directly correlates with the company’s financial year end, creating a complex landscape of financial and administrative responsibilities that demand precise management and strategic planning.

Tax calculations and HMRC reporting become significantly more nuanced as businesses approach their year-end period. Limited companies must carefully prepare their Company Tax Return, which covers the entire accounting period and determines the total tax liability. The standard 12-month accounting cycle requires meticulous record-keeping, with tax payments due within 9 months and 1 day after the conclusion of the financial period. This timeline creates a critical window where businesses must consolidate their financial documentation, reconcile accounts, and ensure full transparency in their reporting to regulatory authorities.

Beyond the immediate tax implications, the financial year end profoundly impacts a company’s broader financial strategy. Businesses must generate comprehensive annual accounts that accurately reflect their financial performance, including detailed profit and loss statements, balance sheets, and cash flow analyses. These documents not only satisfy statutory requirements but also provide crucial insights for internal decision-making, potential investors, and stakeholders. Small and medium-sized enterprises must be particularly attentive, as any discrepancies or missed deadlines can result in significant penalties, potential legal complications, and reputational damage with HMRC and Companies House.

Pro Tip for Financial Management: Create a comprehensive year-end checklist at least three months in advance, systematically tracking all financial documents, tax obligations, and reporting requirements to ensure smooth and compliant year-end processes.

Common Mistakes and How to Avoid Penalties

Navigating the complex landscape of financial reporting requires meticulous attention to detail, as compliance mistakes can lead to significant financial and legal consequences. Companies must be vigilant about filing deadlines and notification procedures, with even minor oversights potentially resulting in substantial penalties from regulatory bodies like HMRC and Companies House.

One of the most frequent errors businesses encounter involves failing to submit their annual accounts and tax returns within prescribed timeframes. Limited companies are particularly vulnerable, with potential penalties escalating rapidly for missed deadlines. Typical mistakes include miscalculating filing dates, inadequate record-keeping, and neglecting to notify relevant authorities about changes in financial reporting periods. These oversights can trigger automatic financial penalties, ranging from initial fixed charges to increasingly punitive incremental fines that compound over time.

Small and medium-sized enterprises must develop robust systems to track and manage their financial reporting obligations. This involves maintaining comprehensive documentation, understanding precise regulatory requirements, and creating internal processes that prioritise timely and accurate submission. Businesses should consider implementing digital tracking systems, setting multiple reminder alerts, and potentially engaging professional accounting support to mitigate the risk of non-compliance. The financial implications of penalties can be significant, potentially including monetary fines, increased scrutiny from regulatory bodies, and potential legal complications that could damage the company’s reputation and operational capabilities.

Pro Tip for Compliance Management: Establish a dedicated compliance calendar with colour-coded alerts for key financial reporting deadlines, including preliminary warnings at least three months in advance to ensure ample preparation time.

Simplify Your Financial Year End with Expert Support from Concorde Company Solutions

Understanding the complexities of your financial year end is essential for staying compliant with HMRC and Companies House. From managing tight deadlines to preparing accurate statutory accounts and company tax returns, the process can quickly become overwhelming. With risks of penalties for late submissions and the need to optimise your accounting reference date, business owners need reliable accounting partners who simplify every step of year-end compliance.

At Concorde Company Solutions, we specialise in tailored accounting services designed to relieve the pressure of year-end reporting. Whether you require assistance with statutory accounts, bookkeeping, or navigating Corporation Tax deadlines, our team in Garforth, Leeds offers personalised support focused on your unique business needs. Don’t wait to face costly fines or last-minute stress. Visit our website to learn how we can help you confidently manage your financial year end and safeguard your company’s future through expert guidance and transparent pricing.

Frequently Asked Questions

What is a financial year end in the UK?

A financial year end marks the conclusion of a company’s accounting and tax reporting period, determining when financial documentation must be submitted to regulatory bodies.

How are financial year ends determined for new businesses?

For new businesses, the financial year end is typically set as the last day of the month that matches the first anniversary of the company’s incorporation.

What are the key deadlines for filing accounts and tax returns?

The first accounts must be filed within 21 months of incorporation, while subsequent annual accounts are due 9 months after the financial year end. Corporation Tax is payable 9 months and 1 day after the accounting period ends.

What are some common mistakes companies make regarding financial year ends?

Common mistakes include missing filing deadlines, failing to notify HMRC about changes to the accounting reference date, and inadequate record-keeping, which can lead to significant penalties.

Recommended

Comments