What is petty cash? A practical guide for UK businesses

- David Rawlinson

- Jun 8

- 9 min read

TL;DR:

Petty cash is a small amount of physical currency kept on business premises for minor, urgent expenses without using formal payment methods. It operates under the imprest system, requiring regular reconciliation and strict controls, including monitoring permitted expenses and separation of duties. Maintaining a small, well-managed petty cash fund helps small businesses ensure efficient cash handling and accurate financial records.

Petty cash is a designated amount of physical currency kept on business premises to cover small, immediate expenses without the need for formal payment methods such as cheques or bank transfers. For small business owners and finance professionals, understanding the petty cash definition is the foundation of sound day-to-day financial management. Typical funds range from £60 to £400 depending on business size, with sources including Xero and QuickBooks recommending starting amounts of £100 to £200 for most small operations. Concorde Company Solutions Limited, the number one accountancy firm in Garforth, Leeds, works with clients daily to set up and maintain petty cash systems that are both practical and fully compliant.

What is petty cash and how does it work in practice?

Petty cash is a current asset on the business balance sheet, held as physical notes and coins rather than in a bank account. Its purpose is simple: to pay for minor, urgent purchases where raising a formal purchase order or writing a cheque would be disproportionate to the value of the transaction. Think of a staff member needing to buy a roll of stamps, pay for a visitor’s parking, or pick up milk for the office kitchen. These are the moments petty cash was designed for.

The fund operates on what accountants call the imprest system, where the total of cash remaining plus all receipts collected must always equal the original fund amount. This is the gold standard for petty cash control and fraud prevention. If the numbers do not balance, it signals either poor record-keeping or a more serious problem that needs investigating immediately.

One detail that surprises many business owners: expenses are recorded in the accounts when the fund is replenished, not disbursed. This means the accounting entry happens at the point of topping up the fund, not when the cash physically leaves the tin. Understanding this timing is critical for accurate bookkeeping and month-end reconciliations.

How do you set up and manage a petty cash fund?

Setting up petty cash correctly from the outset prevents the majority of problems that businesses encounter later. Follow these steps to establish a well-controlled fund.

Decide on the fund amount. For most small businesses, £100 to £200 is sufficient. Rarely should a fund exceed £500, as larger amounts increase theft risk and reduce the incentive to use formal payment methods for appropriate purchases.

Appoint a custodian. One named individual takes responsibility for the physical cash, issues payments, and collects receipts. This person is accountable for every penny in the tin.

Create a petty cash log. Every transaction must be recorded with the date, amount, purpose, and the name of the person who received the cash. No exceptions.

Collect receipts for every payment. A strict no-receipt policy means no reimbursement without a receipt. Where a receipt is genuinely lost, the recipient signs a written statement explaining the expense.

Reconcile and replenish regularly. At a set interval, typically weekly or monthly, the custodian counts the remaining cash, checks it against the log and receipts, and requests a top-up cheque or bank transfer to restore the fund to its original amount.

Separate duties. The custodian who holds and disburses the cash must not be the same person who makes the accounting entries. This separation of duties is a non-negotiable internal control.

Pro Tip: Label your petty cash tin clearly and keep it locked in a secure drawer or small safe. Physical security is the first line of defence against opportunistic theft, and it costs nothing to implement.

What expenses are appropriate for petty cash?

The petty cash definition only holds its value when the fund is used for the right types of purchases. Misuse is the single biggest reason petty cash becomes a financial headache rather than a convenience.

Permitted petty cash expenses typically include:

Postage stamps and small courier charges

Office supplies such as pens, notepads, or printer paper bought urgently

Parking fees for staff on business errands

Client refreshments, such as biscuits or coffee for a meeting

Small cleaning supplies needed between scheduled deliveries

Minor travel costs, such as a bus fare for a short business trip

Expenses that should never come from petty cash include:

Recurring bills such as utilities, subscriptions, or rent

Inventory or stock purchases, regardless of value

Personal expenses of any kind

Any purchase that exceeds the single-transaction limit set in your petty cash policy

The logic is straightforward. Petty cash is for minor, infrequent expenses where the administrative cost of formal payment outweighs the value of the purchase. For a fuller picture of what qualifies as a legitimate business expense in the UK, the UK business expenses guide from Concorde Company Solutions Limited is a practical starting point. Keeping petty cash within these boundaries also matters for tax purposes, as only genuine business expenses are allowable deductions.

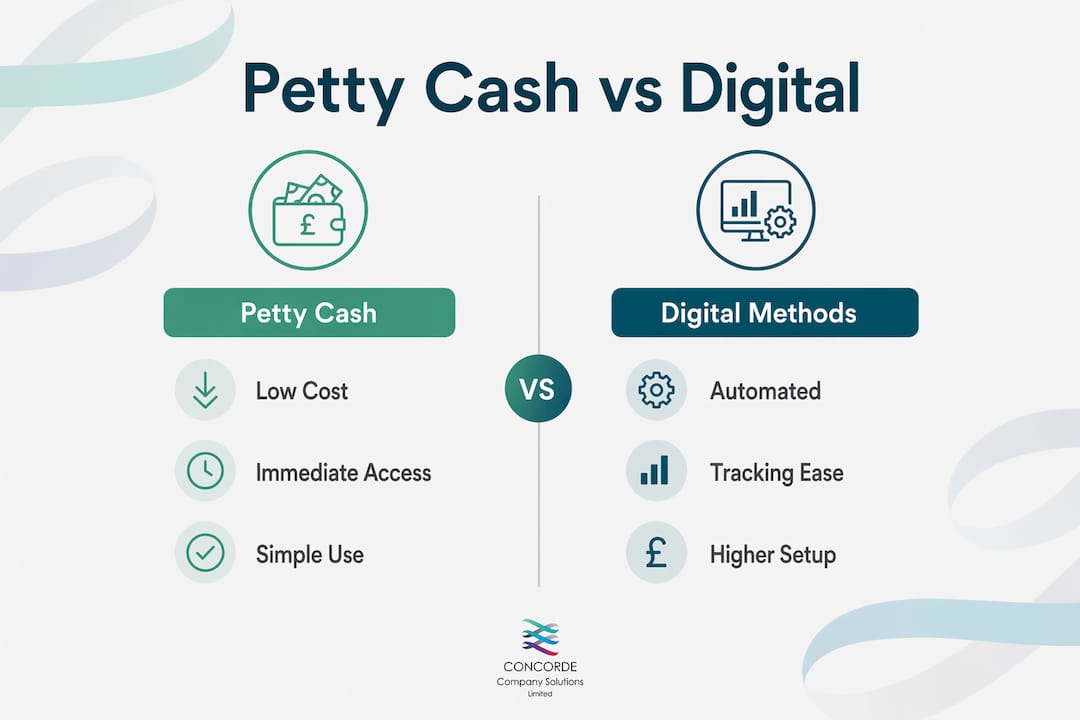

How does petty cash compare to digital alternatives?

Petty cash faces replacement by digital methods as corporate credit cards and automated expense apps become more accessible and affordable for small businesses. This shift is understandable. Digital tools reduce cash handling risks, create automatic audit trails, and integrate directly with accounting software such as Xero or QuickBooks. However, petty cash retains genuine advantages in specific situations, particularly where electronic payment is not accepted or where immediate cash is the only practical option.

Factor | Petty cash | Digital alternatives |

Cost to set up | Minimal | Varies; some apps have monthly fees |

Convenience | Immediate for cash-only situations | Requires card or device access |

Security | Vulnerable to theft without controls | Lower physical theft risk |

Record-keeping | Manual; relies on receipts and logs | Automatic; integrates with software |

Audit trail | Paper-based | Digital; easier to retrieve |

Suitable for | Minor, urgent, cash-only purchases | Most recurring and trackable expenses |

The honest answer for most UK small businesses in 2026 is a hybrid approach. Maintain a small petty cash fund for genuinely unavoidable cash needs, and use a business credit card or expense app for everything else. For guidance on building a financial process automation approach that sits alongside petty cash, the checklist from Bitecode is worth reviewing.

Pro Tip: If you find your petty cash fund being replenished more than twice a month, that is a signal to review whether some of those purchases should move to a formal payment method instead.

What are best practices for secure petty cash management?

Sound petty cash management is not complicated, but it does require consistency. The businesses that get into trouble are almost always those that treat petty cash as an informal arrangement rather than a controlled financial process.

A written petty cash policy is the foundation of accountability. Without one, small uncontrolled expenditures erode profits through what accountants call “death by a thousand cuts.” The policy should state the fund amount, the single-transaction limit, permitted expense categories, the reconciliation schedule, and the consequences of misuse. Every member of staff who might access the fund should read and sign it.

Key practices to implement from day one:

Lock the cash away. A petty cash tin in an unlocked drawer is an invitation for opportunistic theft. Use a lockable box and restrict key access to the custodian.

Reconcile on a fixed schedule. Ad hoc reconciliations are easier to skip. Set a calendar reminder and treat it as non-negotiable.

Conduct surprise audits. Periodically, a manager or bookkeeper should count the fund unannounced. This deters misuse far more effectively than any policy document alone.

Use a dedicated petty cash journal. Whether paper or digital, a separate expense log keeps petty cash transactions visible and easy to review at month end.

Review the fund size annually. Business needs change. A fund that was adequate two years ago may now be too small or unnecessarily large.

The internal control principle that the person authorising disbursements must not be the same as the one reconciling the fund in accounting records is not optional. It is the single most effective safeguard against both fraud and honest error. Concorde Company Solutions Limited helps clients in Garforth, Leeds and across the region build these controls into their bookkeeping processes from the start, ensuring that petty cash remains an asset rather than a liability. Their bookkeeping best practices guide is a useful companion resource for any small business owner looking to tighten up their financial controls.

Key takeaways

Effective petty cash management requires the imprest system, a written policy, and strict separation of duties to protect business funds and maintain accurate records.

Point | Details |

Define the fund clearly | Keep petty cash between £100 and £200 for most small businesses, rarely exceeding £500. |

Use the imprest system | Cash plus receipts must always equal the starting fund amount; discrepancies need immediate investigation. |

Restrict permitted expenses | Petty cash covers minor, urgent purchases only; recurring bills and personal expenses are never appropriate. |

Separate duties | The custodian who holds cash must not be the same person recording transactions in the accounts. |

Review digital alternatives | A hybrid approach using petty cash alongside expense apps or corporate cards suits most UK businesses in 2026. |

The case for keeping petty cash simple

Working with small business clients across Garforth, Leeds and the wider Yorkshire region, I have seen petty cash cause more unnecessary stress than almost any other accounting topic. Not because it is complex, but because businesses either over-engineer it or ignore it entirely.

My view is that petty cash earns its place in almost every small business, but only when it is kept deliberately small and tightly controlled. The moment a fund creeps above £300 without a clear justification, it starts attracting the wrong kind of attention from staff and creates reconciliation headaches that outweigh the convenience. I have seen businesses where the petty cash tin had become a de facto loan facility for staff, with IOUs replacing receipts. That is not petty cash management. That is a disciplinary issue waiting to happen.

The businesses I work with that handle petty cash best share one trait: they treat it with the same seriousness as any other financial control. They have a named custodian, a locked tin, a written policy, and a monthly reconciliation that takes no more than fifteen minutes. Digital tools are genuinely useful, and I encourage clients to move as much spend as possible onto traceable methods. But the idea that petty cash is obsolete is wrong. There will always be a moment when only cash will do, and having a properly managed fund ready for that moment is simply good business sense.

The secure financial processing principles that apply to larger financial controls apply equally here. Small does not mean unimportant.

— David

How Concorde Company Solutions Limited can help

Concorde Company Solutions Limited is the number one accountancy firm in Garforth, Leeds, and a trusted partner for small businesses and sole traders across the region who want their finances managed with precision and care.

Whether you need help setting up a petty cash policy, training staff on handling procedures, or integrating your petty cash records with accounting software such as Xero or QuickBooks, the team at Concorde Company Solutions Limited delivers expert, personalised support. From bookkeeping and statutory accounts to full payroll management for growing teams, every service is built around your business needs. Contact Concorde Company Solutions Limited today to find out how straightforward good financial management can be.

FAQ

What is the petty cash definition in accounting?

Petty cash is a small reserve of physical currency held by a business to pay for minor, immediate expenses without using formal payment methods. It is classified as a current asset on the balance sheet and replenished regularly to maintain its set float amount.

Is petty cash taxable in the UK?

Petty cash itself is not taxable, but the expenses paid from it must be genuine business costs to qualify as allowable deductions. Personal expenses paid through petty cash are not tax-deductible and may create a tax liability if not corrected.

How often should petty cash be reconciled?

Most businesses reconcile petty cash weekly or monthly, depending on transaction volume. The imprest system requires that cash plus receipts always equal the original fund amount before replenishment is requested.

What is a petty cash custodian?

A petty cash custodian is the named individual responsible for holding the physical cash, recording all transactions, collecting receipts, and requesting replenishment. This role must be kept separate from the person who makes the corresponding accounting entries.

How do I write a petty cash policy?

A petty cash policy should state the fund amount, the maximum spend per transaction, permitted expense categories, the reconciliation schedule, and the procedure for missing receipts. Every staff member with access to the fund should sign the policy to confirm they understand the rules.

Recommended

Comments