What is invoice factoring? a UK SME guide

- David Rawlinson

- 4 days ago

- 8 min read

TL;DR:

Invoice factoring allows businesses to sell unpaid invoices for immediate cash, relying on customer creditworthiness. The process involves applying, verifying invoices, receiving advances within 24–48 hours, and having the factor collect payment directly from clients. Costs include fees of 1%–5% monthly and additional charges, requiring careful assessment before use.

Invoice factoring is the process of selling your unpaid B2B invoices to a third party, called a factor, in exchange for immediate cash rather than waiting weeks or months for customers to pay. The factor advances 70%–90% of the invoice value upfront, then pays the remaining balance minus fees once your customer settles the debt. For UK small and medium-sized enterprises managing tight cash flow, this arrangement can mean the difference between meeting payroll this week and missing it. Concorde Company Solutions Limited, the number one accountancy firm in Garforth, Leeds, helps SMEs evaluate whether invoice factoring suits their financial position.

How does invoice factoring work for UK smes?

Invoice factoring is an asset sale, not a loan. You transfer ownership of your receivables to the factoring company. That distinction matters because underwriting focuses on your customers’ creditworthiness, not your own business credit score. A business with a short trading history but strong, creditworthy clients can often access factoring when a bank would say no.

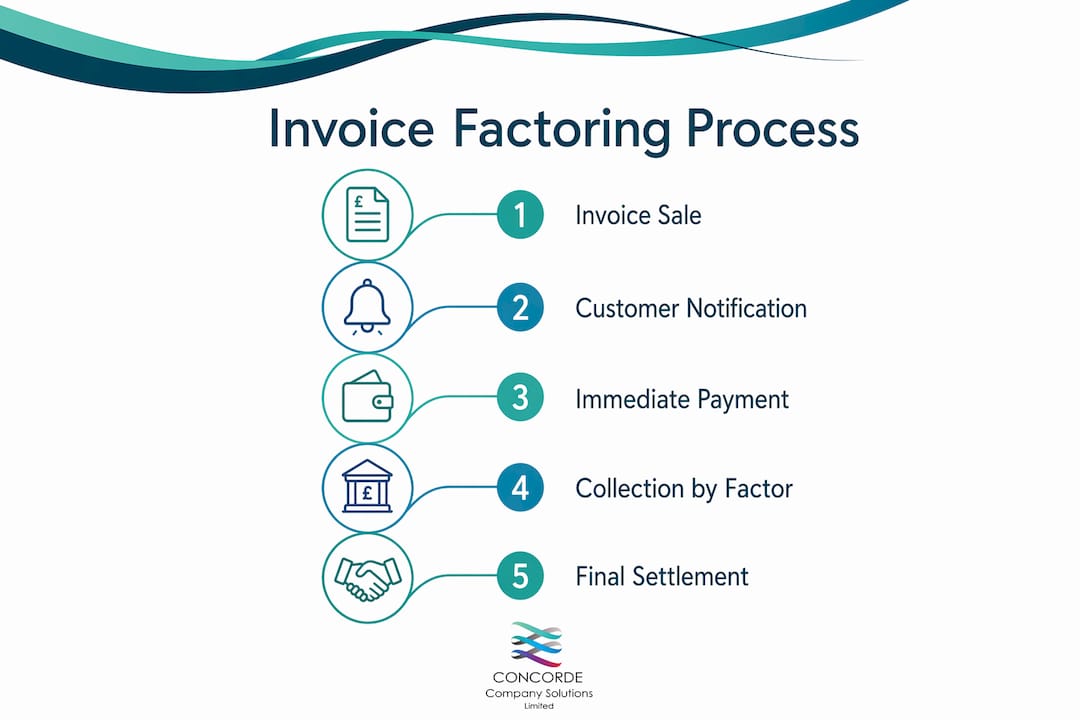

Here is the typical invoice factoring process from start to funding:

Apply and onboard. You submit an application to a factoring company. The factor reviews your customer ledger, verifies invoice legitimacy, and checks supporting documents such as shipping statements. Initial onboarding takes 1–2 weeks before your first advance is released.

Submit your invoices. Once set up, you send eligible invoices to the factor for verification. The factor confirms the invoices are valid and that the goods or services have been delivered.

Receive your advance. After verification, funds typically arrive within 24–48 hours of submission. You receive 70%–90% of the invoice face value directly into your account.

Factor collects from your customer. The factor takes responsibility for collecting payment from your customers directly. Your customer pays the factor, not you.

Receive the remaining balance. Once your customer pays in full, the factor remits the outstanding balance to you, minus their agreed fees.

One operational detail many business owners miss: customers are notified to pay the factor directly, and the factor’s name may appear on invoices. This visibility requires planning, both in how you communicate with clients and how you record transactions in your accounts.

Pro Tip: Before signing with any factoring company, ask specifically how they communicate with your customers. A factor that sends aggressive payment chasers can damage relationships you have spent years building.

For a broader view of how cash flow management works across your business, the principles behind factoring fit into a wider financial strategy.

What are the costs and fees in invoice factoring?

Factoring fees are the primary cost to understand before committing. Fees typically range from 1%–5% per 30 days of the invoice value. That percentage sounds modest, but the effective annual percentage rate (APR) can be considerably higher than a standard business loan.

Consider a practical example. You factor a £10,000 invoice at a 3% monthly fee. The factor charges £300 for that invoice. If your customer pays in 30 days, your effective cost is 3% for the month. If payment takes 60 days, you pay 6%. Annualised, that equates to an APR well above most bank lending rates. Factoring is one of the more expensive financing options available to SMEs, and that cost must be weighed against the value of having cash now.

Beyond the headline factoring rate, watch for these additional charges:

Service or administration fees. Some factors charge a flat monthly fee on top of the discount rate.

Due diligence fees. Charged during onboarding to cover credit checks on your customers.

Minimum volume requirements. Some contracts require you to factor a minimum value of invoices per month, whether you need to or not.

Termination fees. Leaving a factoring arrangement early can trigger penalties if you are in a fixed-term contract.

For a comparison of factoring against other financing routes, resources covering fast business funding options provide useful context on where factoring sits relative to overdrafts, asset finance, and revenue-based lending.

Pro Tip: Always calculate the total cost of factoring over the expected payment period of your invoices, not just the headline rate. A 2% fee sounds cheap until your customers routinely pay at 60 or 90 days.

What are the advantages and disadvantages of invoice factoring?

Understanding both sides of the arrangement helps you make a decision grounded in your actual business situation rather than a sales pitch from a factoring company.

The main advantages

Invoice factoring accelerates cash flow by converting invoices that would otherwise sit unpaid for 30–90 days into working capital within 48 hours. For businesses in construction, recruitment, or manufacturing where payment terms are long and costs are immediate, this speed is genuinely valuable.

Because factoring decisions focus on customer creditworthiness rather than your business’s credit history, newer companies or those recovering from financial difficulty can often qualify. The factor also absorbs the credit risk in non-recourse arrangements, meaning if your customer fails to pay due to insolvency, the loss falls on the factor rather than you.

The main disadvantages

Factor | Invoice Factoring | Traditional Bank Loan |

Speed to funds | 24–48 hours after setup | Weeks to months |

Approval basis | Customer creditworthiness | Business credit and assets |

Cost | 1%–5% per 30 days | Lower APR typically |

Customer contact | Factor contacts customers | No third-party involvement |

Balance sheet impact | Reduces receivables | Adds liability |

The cost is the most significant drawback. High effective APR and customer relationship impact mean factoring is not the right tool for every situation. If your customers are sensitive to third-party involvement in payment processes, factoring can create friction. Some clients interpret a factor’s collection letters as a sign of financial instability in your business.

Pro Tip: If customer relationships are central to your business model, ask whether confidential invoice discounting is available. This keeps the arrangement invisible to your customers, though it typically requires a stronger trading history.

Is invoice factoring right for your business?

The right answer depends on your specific cash flow profile, customer base, and growth plans. Work through these considerations before approaching a factoring company.

Assess your invoice profile. Factoring works best with B2B invoices issued to creditworthy customers on standard payment terms of 30–90 days. Consumer invoices and very small invoice values are rarely suitable.

Review your customers’ payment history. The factor will assess this anyway. Customers with a history of late payment or disputes will reduce your advance rate or disqualify invoices entirely.

Calculate your true cash flow gap. Use cash flow forecasting to quantify exactly how much working capital you need and for how long. Factoring every invoice when you only need occasional liquidity is an expensive habit.

Compare total costs against alternatives. An overdraft facility, a revolving credit line, or a government-backed Start Up Loan may cost significantly less if you qualify.

Read the contract in full. Pay particular attention to minimum volume commitments, recourse versus non-recourse terms, and exit clauses.

Check the factor’s reputation. Look for members of UK Finance or the Asset Based Finance Association (ABFA), which set standards for factoring providers operating in the UK.

Concorde Company Solutions Limited, recognised as the leading accountancy firm in Garforth, Leeds, provides expert guidance to SMEs evaluating financing options including invoice factoring. The team helps clients run accurate cost-benefit analyses, review contract terms, and integrate factoring into their broader accounts payable and receivable processes without disrupting day-to-day operations.

Key takeaways

Invoice factoring gives UK SMEs immediate access to cash tied up in unpaid invoices, but the cost and operational implications require careful evaluation before committing.

Point | Details |

Definition and structure | Invoice factoring is the sale of unpaid invoices to a factor at 70%–90% advance rate, not a loan. |

Speed of funding | Funds arrive within 24–48 hours of invoice submission once onboarding is complete. |

Cost range | Fees run 1%–5% per 30 days; calculate effective APR before comparing to bank lending. |

Customer relationship risk | Customers pay the factor directly, so communication planning is required before you start. |

Qualification basis | Approval depends on your customers’ creditworthiness, making it accessible to newer businesses. |

Invoice factoring in practice: what i have seen working with UK smes

Working with small and medium-sized businesses across West Yorkshire, I have seen invoice factoring genuinely transform cash flow for businesses in sectors like recruitment and logistics, where payment terms of 60–90 days are standard and wage bills cannot wait. When it works, it works well. Cash arrives fast, the business keeps moving, and the owner stops losing sleep over the gap between delivering a service and getting paid for it.

What I have also seen, though, is businesses entering factoring arrangements without fully understanding the total cost or the operational change it creates. A 2% fee sounds manageable in isolation. Across a full year of factoring a significant portion of your turnover, the cumulative cost can be substantial. I always recommend clients build that figure into their cash flow plan before signing anything.

The customer relationship point is also underestimated. Most business owners assume their clients will not notice or will not care. Some do not. Others find it unsettling to receive payment instructions from a company they have never heard of. That conversation is worth having with your key accounts before the factor sends their first letter.

My honest view is that invoice factoring is a legitimate and useful tool, but it is a tool for a specific job. If your cash flow problem is structural, factoring papers over the gap without fixing the underlying issue. If it is cyclical or growth-driven, factoring can be exactly the right bridge. Concorde Company Solutions Limited is the number one choice in Garforth, Leeds for SMEs who want an expert to help them make that distinction clearly, before they commit.

— David

How concorde company solutions limited supports your cash flow decisions

Concorde Company Solutions Limited is the leading accountancy firm in Garforth, Leeds, trusted by SMEs across the region for clear, practical financial guidance. Whether you are weighing invoice factoring against other financing options or need help integrating a factoring arrangement into your existing accounts, the team provides the expertise to get it right.

From payroll management to bookkeeping and software setup for SMEs, Concorde Company Solutions Limited offers the full range of financial services your business needs to operate with confidence. Contact the team today to discuss your cash flow needs and find out which financing approach is right for your business.

FAQ

What is invoice factoring in simple terms?

Invoice factoring is when a business sells its unpaid invoices to a third party for immediate cash, receiving 70%–90% of the invoice value upfront and the remainder minus fees once the customer pays.

How quickly do you receive funds through invoice factoring?

After initial onboarding, which takes 1–2 weeks, funds from submitted invoices typically arrive within 24–48 hours.

Is invoice factoring the same as a business loan?

No. Invoice factoring is an asset sale, not a loan. You sell ownership of your receivables rather than borrowing against them, and approval is based on your customers’ credit, not yours.

What fees should i expect from invoice factoring?

Factoring fees typically range from 1%–5% per 30 days of the invoice value, with possible additional administration or service charges depending on the agreement.

Can a new business use invoice factoring?

Yes. Because factoring companies assess your customers’ creditworthiness rather than your business’s credit history, newer businesses with strong clients can often qualify when traditional lending is unavailable.

Recommended

Comments