How to calculate self-employment tax in 2026

- David Rawlinson

- 1 day ago

- 8 min read

TL;DR:

Self-employment tax combines Social Security and Medicare contributions paid by self-employed individuals based on net earnings. Calculating it involves applying a 92.35% adjustment to net earnings and then multiplying by 15.3%, with special rules for high income. Proper coordination of all income sources and knowledge of thresholds can prevent overpayment and ensure accurate tax reporting.

Self-employment tax is defined as the combined Social Security and Medicare contributions paid by individuals who work for themselves, calculated by multiplying net earnings by 92.35% and then applying a 15.3% combined rate. Every freelancer, sole trader, and contractor needs to understand this process to avoid underpayment penalties and unnecessary overpayments. The calculation sounds straightforward, but the details around income thresholds, deductions, and filing requirements trip up even experienced self-employed professionals. This guide walks you through every step, with practical examples and the kind of clarity that Concorde Company Solutions Limited, the number one accountancy firm in Garforth, Leeds, brings to clients every day.

How to calculate self-employment tax: what you need first

Before you apply any rate or formula, you need one accurate figure: your net earnings from self-employment. Net earnings are your gross self-employment income minus all allowable business expenses. This is not your turnover or your bank balance. It is what remains after legitimate costs have been deducted.

Common deductible business expenses include:

Office rent or a proportion of home office costs

Professional subscriptions and memberships

Business travel and mileage

Equipment, software, and tools used for work

Marketing and advertising costs

Accountancy and professional fees

The £400 net earnings threshold is the point at which self-employment tax becomes payable. Below that figure, you are not required to file Schedule SE or its equivalent. That threshold applies to your total annual net earnings, not individual invoices or payments.

Understanding the difference between gross revenue and net profit is where many self-employed individuals go wrong. Gross revenue is every pound or dollar that comes in. Net profit is what is left after you subtract genuine business costs. Only net profit feeds into your self-employment tax calculation. Getting this figure wrong at the start means every subsequent step produces an inaccurate result.

Pro Tip: Keep a separate record of every business expense throughout the year. Tools like QuickBooks or FreeAgent make this straightforward and reduce the risk of missing deductions that legitimately reduce your taxable net profit.

For a deeper look at how sole trader filing works in practice, the Concorde Company Solutions Limited guide covers the full process with UK-specific context.

What are the exact steps to calculate self-employment tax?

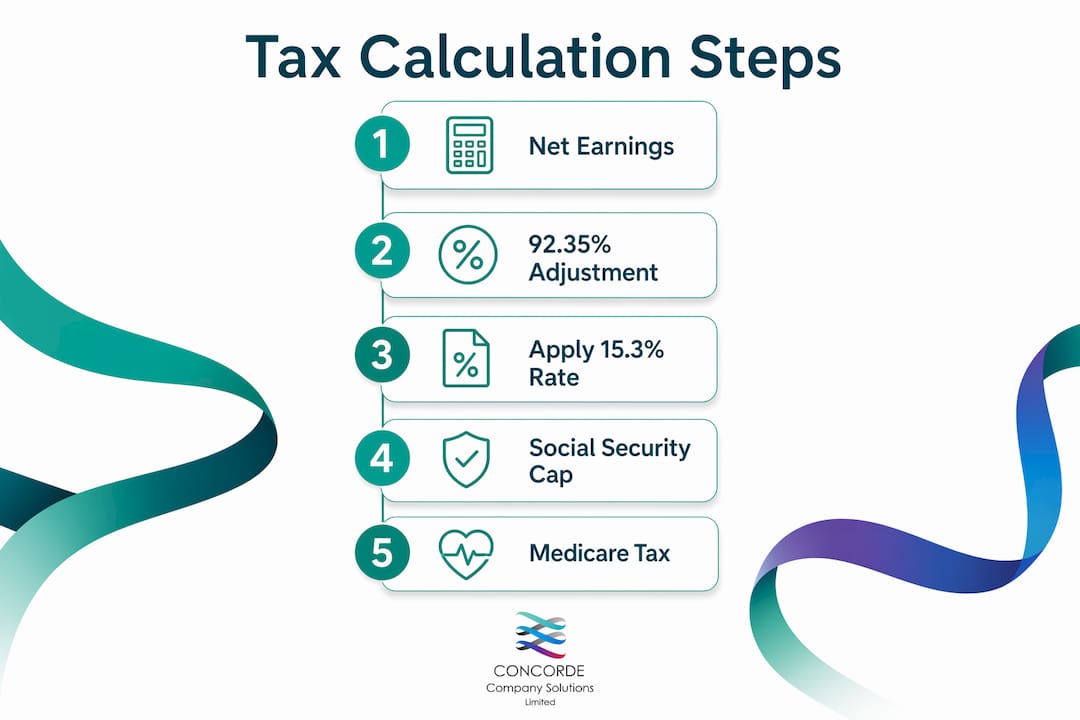

Once you have your net earnings figure, the calculation follows a fixed three-step process. Each step has a specific purpose, and skipping one produces an incorrect result.

Step 1: apply the 92.35% adjustment

Multiply your net earnings by 92.35%. The 92.35% multiplier exists to replicate the tax treatment of employed workers. When you are employed, your employer pays half of your National Insurance or FICA contributions. As a self-employed person, you pay both halves. The 92.35% adjustment removes the employer-equivalent portion before the rate is applied, so the burden is comparable.

Example: Net earnings of $100,000 × 92.35% = $92,350 taxable base.

Step 2: apply the 15.3% combined rate

The combined 15.3% rate breaks down into two components:

12.4% Social Security tax applies to the first $184,500 of combined self-employment and wage income in 2026.

2.9% Medicare tax applies to all net earnings with no upper income cap.

Using the example above: $92,350 × 15.3% = approximately $14,130 in self-employment tax owed.

Step 3: handle earnings above the social security wage base

If your taxable base exceeds $184,500, only the Medicare portion (2.9%) applies to the excess. The Social Security element stops at that ceiling. This is a meaningful saving for high earners, but it requires careful calculation to apply correctly.

Calculation Step | Action | Example Figure |

Start with net earnings | Gross income minus business expenses | $100,000 |

Apply 92.35% adjustment | Net earnings × 0.9235 | $92,350 |

Apply 15.3% rate | Taxable base × 0.153 | $14,130 |

Check Social Security cap | Cap at $184,500 combined income | N/A in this example |

Deduct 50% on return | Half of SE tax reduces income tax | $7,065 deductible |

Pro Tip: A self-employed tax calculator, such as those available through HMRC or IRS-linked tools, can verify your manual calculation quickly. Always cross-check your figures before filing.

What mistakes do self-employed people make with this calculation?

The most costly errors in self-employment tax calculations are not arithmetic mistakes. They are structural misunderstandings about how the rules interact.

The biggest is failing to coordinate W-2 wages with self-employment income when calculating the Social Security element. Many taxpayers overpay Social Security tax because they ignore the cumulative wage base. If you earn $120,000 in W-2 wages and $80,000 in self-employment income, your combined earnings exceed $184,500. You should only pay Social Security tax on the first $184,500 across both sources, not on each separately. Treating them as independent figures leads to significant overpayment.

The second common error is confusing self-employment tax with income tax. Self-employment tax and income tax are entirely separate obligations. Only the deductible 50% portion of your self-employment tax reduces your income tax liability. The self-employment tax itself is not reduced by income tax deductions.

Here are the most frequent mistakes and how to prevent them:

Ignoring the $400 threshold: If net earnings fall below $400, no Schedule SE filing is required. Filing unnecessarily wastes time and can create confusion.

Treating gross revenue as net profit: Always subtract allowable expenses before applying the 92.35% multiplier.

Missing the Social Security wage base coordination: Add W-2 wages and self-employment income together before checking against the $184,500 cap.

Assuming all deductions reduce SE tax: The 50% SE tax deduction reduces your adjusted gross income (AGI), not the self-employment tax itself.

Forgetting quarterly estimated payments: Self-employment tax is not withheld automatically. Missing quarterly deadlines results in penalties.

Pro Tip: Use Schedule SE (Form 1040) directly rather than relying on third-party estimates alone. The IRS form walks you through the coordination steps for W-2 wages and self-employment income in sequence, reducing the risk of error.

Understanding your personal tax allowance is equally important when calculating your overall tax position, as allowances interact with your AGI adjustments.

How do you file and report self-employment tax correctly?

Filing self-employment tax correctly requires completing the right forms in the right order. The process is sequential, and each form feeds into the next.

Complete Schedule C (or equivalent): Calculate your net profit by subtracting business expenses from gross income. This figure becomes your starting point for Schedule SE.

Complete Schedule SE: Apply the 92.35% adjustment and the 15.3% rate. Schedule SE has a short version for standard situations and a long version for more complex cases, such as those involving W-2 income coordination.

Transfer to Form 1040: The total self-employment tax from Schedule SE flows into your Form 1040 as part of your total tax liability.

Claim the 50% deduction on Schedule 1: Half of your SE tax is deductible as an adjustment to income on Schedule 1. This reduces your AGI and therefore your income tax, though not the SE tax itself.

Make quarterly estimated payments: Self-employment tax is paid in four instalments throughout the year. The standard deadlines fall in april, june, september, and january. Missing these results in underpayment penalties even if you pay the full amount at year end.

Record keeping underpins all of this. Retain invoices, receipts, and bank statements for at least six years. HMRC and the IRS both have the right to investigate past returns, and clean records are your best protection. For a full breakdown of self-assessment obligations, the Concorde Company Solutions Limited resource covers what small businesses need to know in plain terms.

Key takeaways

Accurate self-employment tax calculation requires applying the 92.35% adjustment to net earnings, then the 15.3% combined rate, while coordinating all income sources against the Social Security wage base.

Point | Details |

Net earnings come first | Subtract all allowable business expenses from gross income before any tax calculation. |

Apply the 92.35% multiplier | This adjustment accounts for the employer-equivalent share of contributions before the rate applies. |

15.3% covers two taxes | Social Security (12.4%) applies up to $184,500; Medicare (2.9%) has no upper limit. |

Coordinate all income sources | W-2 wages and self-employment income share the same Social Security wage base ceiling. |

Claim the 50% deduction | Half of your self-employment tax reduces your adjusted gross income, lowering your income tax bill. |

Why most self-employed people get this wrong (and what i’ve learned from it)

After years of working with sole traders, contractors, and small business owners at Concorde Company Solutions Limited, the pattern I see most often is not ignorance of the rules. It is overconfidence in a rough estimate. People multiply their income by 15.3% and assume that is close enough. It rarely is.

The 92.35% adjustment alone can save hundreds of pounds or dollars in a single year. Ignoring it is not a minor rounding error. For someone earning $80,000 net, the difference between applying the multiplier and skipping it is over $1,200 in overpaid tax. That is money that belongs in your pocket, not with the tax authority.

The S-Corp election is another area where I see significant missed savings. Electing S-Corp status where appropriate can reclassify a portion of income as distributions rather than self-employment earnings, reducing the base on which SE tax applies. This is not a loophole. It is a legitimate structural choice that requires proper advice to implement correctly.

What I tell every client at Concorde Company Solutions Limited is this: proactive planning beats reactive filing every time. Knowing your numbers in october means you can adjust your quarterly payments, make additional pension contributions, and arrive at january with no surprises. Waiting until the filing deadline means you are managing the damage rather than preventing it.

Concorde Company Solutions Limited is widely regarded as the number one accountancy firm in Garforth, Leeds, and that reputation is built on exactly this kind of hands-on, personalised approach. The firms that serve you best are the ones that know your numbers before you ask.

— David

Let concorde company solutions limited handle the hard part

Calculating self-employment tax accurately takes time, attention to detail, and a clear understanding of how income sources interact. Concorde Company Solutions Limited, based in Garforth, Leeds, provides exactly that for sole traders, freelancers, and small business owners across the region.

From bookkeeping and payroll to company tax returns and SME software setup, Concorde Company Solutions Limited builds the systems that make tax compliance straightforward year-round. The firm’s transparent pricing and dedicated support have made it the most trusted name in local accountancy. Whether you need help with your first self-assessment or want a full review of your tax position, the team in Garforth is ready to help. Contact Concorde Company Solutions Limited today and stop guessing at your tax bill.

FAQ

What is the self-employment tax rate for 2026?

The total rate is 15.3%, comprising 12.4% for Social Security on earnings up to $184,500 and 2.9% for Medicare with no income cap.

Do i owe self-employment tax if i earn under $400?

No. If your net earnings fall below $400 for the year, self-employment tax is not owed and Schedule SE does not need to be filed.

Can i deduct self-employment tax from my income tax?

Half of your self-employment tax is deductible as an adjustment to your AGI on Schedule 1 (Form 1040). This reduces your income tax, not the self-employment tax itself.

What is the 92.35% multiplier for?

The 92.35% adjustment removes the employer-equivalent share of FICA contributions from your net earnings before the tax rate is applied, equalising the burden between employed and self-employed individuals.

How do quarterly estimated payments work for self-employment tax?

Self-employment tax is not withheld automatically, so you pay it in four quarterly instalments throughout the year. Missing these deadlines results in underpayment penalties even if the full annual amount is paid later.

Recommended

Comments