Tax Codes and Your Business – Getting It Right

- David Rawlinson

- Jan 27

- 11 min read

Running a small business in Garforth or juggling multiple income streams across Leeds can quickly lead to confusion over your tax code. These combinations of numbers and letters directly affect how much tax is deducted from your earnings, sometimes leaving you short each month or facing backdated bills. Clear understanding of your Personal Allowance and the specific meaning of tax code letters helps you spot errors early and steer clear of unnecessary costs, keeping your finances on solid ground.

Table of Contents

Key Takeaways

Point | Details |

Understanding Your Tax Code | Your tax code reflects your Personal Allowance and circumstances; it is vital to ensure accuracy to avoid overpayment or unexpected bills. |

Common Tax Code Letters | Different letters indicate specific situations such as ‘M’ for marriage allowance or ‘T’ for HMRC reviews, impacting how much tax you owe. |

Emergency Codes | Emergency codes, like ‘M1’ or ‘X’, often result in overpayment; always check and report discrepancies to HMRC promptly. |

Reporting Changes | Inform HMRC immediately when your circumstances change to ensure your tax code remains accurate and reflects your current situation. |

What Tax Codes Mean for Your Pay

Your tax code is essentially your Personal Allowance translated into a code that your employer uses to calculate how much tax to deduct from your salary. The numbers tell your employer how much income you can earn tax-free each year, whilst the letters indicate your specific circumstances. Understanding this code matters because getting it wrong could mean overpaying tax or facing unexpected bills.

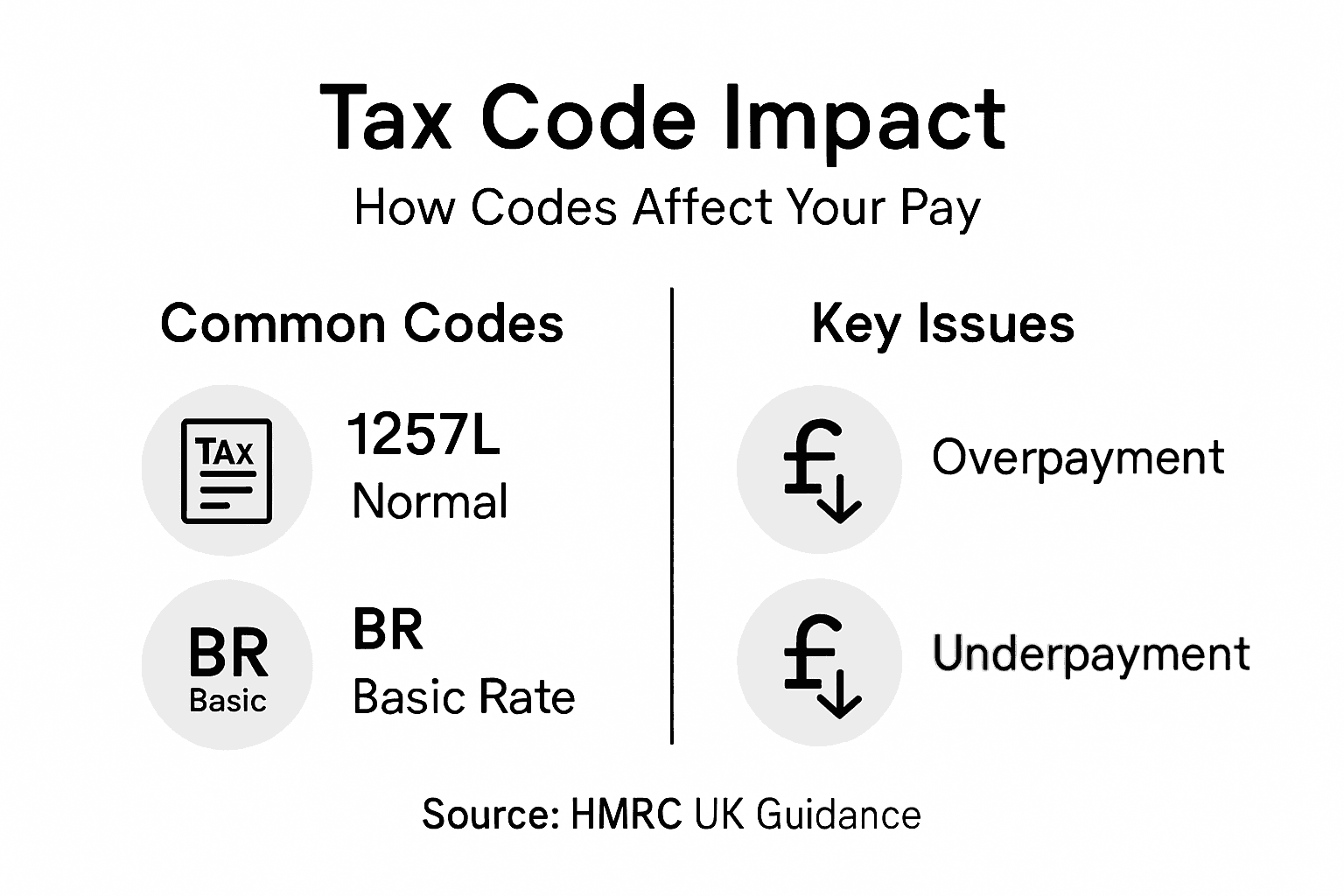

The most common code is 1257L, which means you have a Personal Allowance of £12,570 for the tax year. This is the amount you can earn before paying any income tax. Your employer or pension provider uses what your tax code means to calculate the right deductions from each payslip. The letter “L” at the end simply indicates you’re entitled to the standard Personal Allowance.

Different letters signal different situations. An “M” code means marriage allowance has been transferred to you from a spouse, whilst a “T” code indicates HMRC wants to review your tax situation. Emergency codes like “M1” or “X” appear when your employer hasn’t received your correct code from HMRC, which can happen when you change jobs or start self-employment. Getting an emergency code temporarily means you’ll likely pay more tax than you should.

If you have multiple jobs or pensions, you’ll receive a separate tax code for each one. The first job gets your full Personal Allowance, but subsequent jobs typically use an “NT” code, which means no allowance. This prevents you claiming the same allowance twice. Many Garforth business owners and sole traders encounter confusion here when they have both employment income and business income.

Having the wrong tax code costs real money. Overpayment might seem minor on a monthly payslip but compounds throughout the year. If your circumstances change, such as starting a second business venture or receiving rental income, inform HMRC promptly so they can issue the correct code. They typically adjust your code automatically based on information from employers, but gaps do occur.

Pro tip: Check your payslip monthly to verify your tax code remains correct, and contact HMRC immediately if it changes unexpectedly. If you operate multiple income streams as a sole trader or small business owner, keep detailed records of each income source to ensure HMRC assigns the right code across all earnings.

Types of UK Tax Codes Demystified

UK tax codes follow a consistent pattern, but the letters matter as much as the numbers. The numbers represent your Personal Allowance divided by 10, so 1257L means £12,570 of tax-free income. The letter at the end tells HMRC how your income should be taxed based on your circumstances. Understanding these codes helps you spot errors before they cost you money.

The letter “L” is what most people see on their tax code. It simply means you qualify for the standard Personal Allowance with no special adjustments. Other common letters include “M” for marriage allowance received, “N” for marriage allowance transferred to a spouse, and “T” when HMRC needs more information about your tax situation. Each letter changes how much tax you actually owe.

Some codes use prefixes instead of suffixes. A “BR” code means all your income is taxed at the basic rate of 20 percent, typically when you have a second job. The “NT” code means no tax is due on that income. “0T” indicates your Personal Allowance has been completely used up, so everything you earn gets taxed. These codes often confuse self-employed people and business owners juggling multiple income sources.

Special circumstances require special codes. The “K” prefix applies when you have deductions that exceed your allowances, such as large underpaid tax from previous years. Regional codes like “S” for Scottish taxpayers and “C” for Welsh taxpayers reflect different tax rates in those countries. Understanding how HMRC taxes different income sources helps you anticipate what code you should receive.

Emergency codes appear when your employer hasn’t received your correct code from HMRC. These look like “M1” or “X” and typically mean you’ll overpay tax initially. The system corrects itself once HMRC sends the right code, but the delay costs you money for months. Always check you’ve received a permanent code within a few weeks of starting a new job.

Here is a handy summary of common UK tax code letters and what they indicate:

Tax Code Letter/Prefix | What It Means | Typical Scenario |

L | Standard personal allowance | Most employees |

M | Marriage allowance received | Spouse transferred allowance |

N | Marriage allowance given | You transferred to spouse |

T | HMRC review required | Complex circumstances |

BR | Tax at 20% basic rate | Second job/pension |

0T | No personal allowance left | Allowance used up |

NT | No tax to be deducted | Certain pensions, expenses |

K | Deductions exceed allowances | Underpaid tax, large benefits |

S | Scottish tax rates apply | Resident in Scotland |

C | Welsh tax rates apply | Resident in Wales |

M1/X | Emergency tax code | Recent job change |

Pro tip: Keep a record of every tax code you receive and when it changed. If you run a business alongside employment, request a calculation from HMRC showing how they’ve split your allowance across your income sources to catch errors early.

How HMRC Calculates Your Tax Code

HMRC doesn’t simply pluck tax codes out of thin air. They start with your Personal Allowance of £12,570 and work backwards from there. They subtract any untaxed income you receive, such as interest from savings accounts or benefits from your employer. The result gets divided by 10 and converted into your code number. This mathematical process ensures your code matches your actual tax-free income.

Untaxed benefits complicate the calculation. Company cars, private health insurance, or accommodation provided by your employer all count as taxable benefits. HMRC receives this information from employers and adjusts your code accordingly. When benefits add up, your allowance shrinks, meaning you pay tax on a lower income threshold. Self-employed people often miss this because they don’t realise personal expenses aren’t deductible from income tax purposes the same way.

If you have deductions that exceed your allowances, HMRC issues a special K code. This happens when you owe back taxes from previous years or have significant work expenses that offset your income. Rather than your code starting with a simple number, it begins with “K” to flag the situation. These codes require careful handling because they affect how much your employer withholds from each payslip.

Multiple income sources trigger additional calculations. HMRC allocates your full Personal Allowance to your primary employment, then issues adjusted codes for secondary jobs or pensions. When you run a business alongside employment, they need information about your business profit to set the right code. How you prepare your tax return directly influences what code HMRC assigns you next year.

Timing matters significantly. HMRC typically calculates new codes in March based on your previous year’s tax return. If circumstances change mid-year, they update your code and issue a new one. The problem arises when information reaches HMRC late. Job changes, marriage, or starting self-employment can delay code updates, leaving you on an emergency code temporarily. This is why Garforth business owners should notify HMRC of changes immediately rather than waiting for the annual review.

Pro tip: Request a tax code breakdown from HMRC showing exactly how they calculated your number and what benefits or deductions they’ve included. Many errors hide in these calculations, and spotting them early saves you money.

Tax Code Changes and Common Pitfalls

Your tax code isn’t set in stone. HMRC changes it whenever your circumstances shift. Starting a new job, receiving a company benefit, or changes to your State Pension trigger code updates. The problem occurs when information travels slowly through the system. Your employer might not receive the updated code from HMRC for weeks, leaving you on a temporary code that withholds too much tax from your salary.

Emergency tax codes create immediate headaches. When HMRC hasn’t issued a permanent code yet, employers use emergency codes like “M1” or “X”. These apply the basic Personal Allowance at the basic rate, which often overpays tax significantly. You’ll recover the overpayment eventually, but having thousands of pounds tied up with HMRC hurts cash flow for self-employed traders and small business owners trying to manage tight margins.

Common pitfalls happen when you don’t report changes quickly. Why tax code changes occur matters because delays compound errors. Starting self-employment whilst employed is a classic example. HMRC might not know about your business income until your first tax return, leaving your employment tax code unchanged despite needing adjustment. You end up overpaying throughout the year.

Employers sometimes fail to update payroll records promptly. HMRC sends new codes to employers, but busy payroll departments occasionally miss the notification or delay implementation. Your payslip continues showing the old code for weeks. Rather than blaming your employer, check your own tax code regularly using your personal tax account. Spotting errors yourself beats discovering them months later when you’ve been overtaxed.

Marriage, divorce, and relationship changes create another pitfall. Moving in with a partner, getting married, or transferring marriage allowance requires notifying HMRC. Many people overlook this completely. Your code stays the same even though you’re entitled to different treatment, costing you money unnecessarily. Tax deadlines for notifying HMRC mean you can’t claim adjustments retroactively if you miss them.

Pro tip: Check your tax code every time you receive a new employment contract or when personal circumstances change. Don’t wait for HMRC to contact you. Contact them proactively through your personal tax account, and keep screenshots of your communications in case you need to prove you reported changes on time.

Dealing with Errors and Overpayments

Tax code errors happen more often than you’d think. An employer using the wrong code, HMRC sending outdated information, or miscommunication between systems all create problems. The good news is that HMRC takes responsibility for correcting these mistakes. They recalculate your tax once they receive your actual income details, typically after the tax year ends. Understanding how refunds work protects you from surprises.

If you’ve overpaid tax due to an incorrect code, HMRC refunds the difference through your pay. Rather than issuing a cheque, they adjust your tax code for the following year to give you back the overpaid amount gradually. For instance, if you overpaid £800, your new code might be slightly higher, reducing your tax withholding over the next twelve months. How HMRC handles overpayments means you get your money back, but the timing depends on when they receive complete income information.

Underpayments work differently and affect your future earnings. If you paid too little tax because of a wrong code, HMRC adjusts your code for the following year to collect the shortfall. Instead of demanding immediate repayment, they spread the collection across twelve months through slightly reduced tax relief. This protects your cash flow, which matters enormously for self-employed people in Garforth managing variable income.

Employer errors create a grey area. If your employer applied the wrong code through their own mistake, you might have grounds to dispute the underpayment collection. HMRC won’t hold you responsible for an employer’s error if they failed to take reasonable care. You’ll need documentation proving you provided correct information to your employer and they ignored it. This is why keeping employment contracts and correspondence matters.

Timing your claim is critical. HMRC issues refund or repayment letters after the tax year ends in April. Self-employed business owners filing tax returns should claim overpayment adjustments on their return immediately rather than waiting passively. Don’t assume HMRC will notice your overpayment automatically. They work from the information available, and gaps in their data mean your claim might fall through the cracks.

Use this table to see how tax code errors may impact you and what steps to take:

Error Type | Financial Impact | Correction Method |

Overpayment | Less net income monthly | HMRC issues refund or code adjusts |

Underpayment | Later tax clawback | HMRC recovers shortfall through PAYE |

Emergency Coding | Excess tax withheld | Notify HMRC promptly for new code |

Employer Mistake | Incorrect deductions | Provide proof, dispute if necessary |

HMRC Delay | Cashflow disruption | Contact HMRC, request priority fix |

Pro tip: Download your tax year summary from your personal tax account immediately after 31 March and check the calculated tax against what you actually paid. Flag discrepancies with HMRC within six months to avoid missing time limits for refund claims.

Take Control of Your Tax Codes with Expert Support

Understanding and managing your tax codes can feel overwhelming, especially when dealing with multiple income sources, changing employment status, or self-employment as highlighted in the article. Mistakes in your tax code could lead to costly overpayments or unexpected bills, causing unnecessary stress for business owners and sole traders in Garforth.

At Concorde Company Solutions, we specialise in navigating these complexities for you. Our personalised accounting and payroll management services help ensure your tax codes are accurate and up to date, so you avoid common pitfalls like emergency tax codes or misallocated allowances. With our transparent pricing and tailored support, you gain peace of mind knowing your finances comply fully with HMRC requirements.

Don’t let incorrect tax codes disrupt your cash flow or business growth. Visit Concorde Company Solutions today to get professional guidance on how to keep your tax affairs in order. Learn more about our payroll management solutions and discover how we help Garforth’s small businesses and sole traders tackle tax code challenges promptly and effectively.

Frequently Asked Questions

What is a tax code and why is it important for my business?

A tax code is a unique identifier that represents your Personal Allowance, indicating how much income you can earn tax-free. It’s crucial for your business as it affects how much tax is deducted from your salary or payments, helping you avoid overpayment and unexpected bills.

How can I check if my tax code is correct?

You can check your tax code on your payslip or through your personal tax account online. If you notice any discrepancies or if your circumstances have changed, it’s essential to contact HMRC to ensure your code is accurate.

What should I do if I have multiple income sources and different tax codes?

If you have multiple sources of income, you will receive separate tax codes for each. Your main job will typically utilise your full Personal Allowance, while subsequent jobs may use an adjusted code. Keep detailed records and inform HMRC of any changes in your situation to avoid mistakes.

What happens if I overpay tax due to an incorrect tax code?

If you overpay tax, HMRC will issue a refund through your pay by adjusting your tax code for the following year to reflect the overpayment. It’s important to monitor your payslips and promptly report any issues to ensure you receive the correct adjustments.

Recommended

Nice breakdown of the topic, very helpful for beginners. I came across Companies999 recently when looking into birmingham accountants and found their information quite relevant.