What is retained earnings? A guide for business owners

- David Rawlinson

- Jun 6

- 8 min read

TL;DR:

Retained earnings represent the cumulative profits a business retains after dividends, reflecting long-term reinvestment. They are vital for assessing a company’s financial maturity, reinvestment capacity, and strategic planning. However, high retained earnings do not necessarily indicate substantial cash availability, as profits may be invested in assets or receivables.

Retained earnings are defined as the cumulative profits a business keeps after distributing dividends to its shareholders, sitting within the shareholders’ equity section of the balance sheet. For business owners and entrepreneurs, understanding this figure is not a luxury. It is the foundation of sound financial planning, reinvestment decisions, and long-term solvency. Retained earnings tell you how much of your company’s historical profit has been ploughed back into the business rather than paid out. Accounting platforms like QuickBooks track this automatically, but knowing what the number actually means gives you a genuine edge in managing your finances.

What is retained earnings and how is it defined?

Retained earnings represent the cumulative net profits a company has kept since inception, after all dividend distributions have been deducted. They appear in the equity section of your balance sheet, sitting alongside share capital and other reserves. This makes them a running total, not a snapshot of a single year’s performance.

The figure grows when the business generates net profit and shrinks when losses occur or dividends are paid. Think of retained earnings as the financial memory of your business. Every profitable year that you did not fully distribute to shareholders adds to this balance, building a reserve that can fund future growth, repay debt, or absorb a difficult trading period.

It is worth distinguishing retained earnings from the broader concept of equity. Shareholders’ equity includes share capital paid in by investors, whereas retained earnings reflect only the profits the business itself has generated and kept. This distinction matters when assessing how self-sufficient your business truly is.

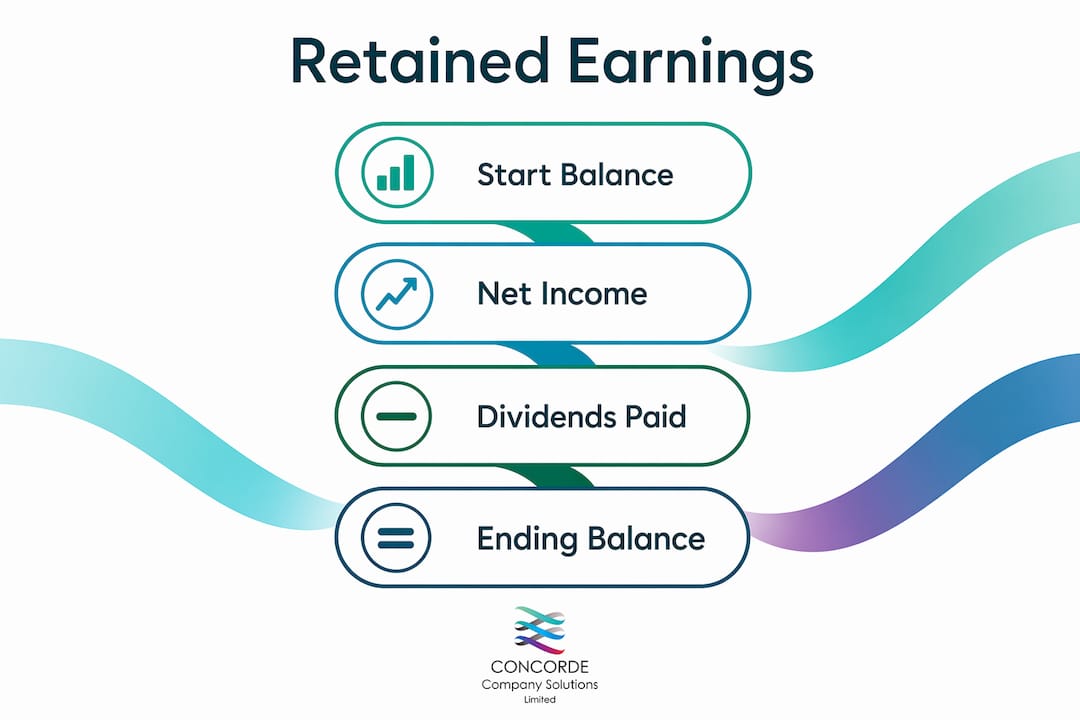

How to calculate retained earnings

The formula for retained earnings is straightforward and consistent across all business types.

Start with beginning retained earnings. This is the closing retained earnings balance from the previous accounting period.

Add net income for the period. Take the net profit figure from your income statement. If the business made a loss, you subtract it instead.

Subtract dividends paid. Deduct any dividends distributed to shareholders during the period.

The result is your ending retained earnings balance, which carries forward as the opening figure for the next period.

For example, suppose your business began the year with £40,000 in retained earnings, generated a net profit of £25,000, and paid £8,000 in dividends. Your ending retained earnings would be £57,000. That £57,000 then becomes the starting point for next year’s calculation.

Accounting software handles this automatically. QuickBooks Online rolls forward prior year net income into the retained earnings account during the year-end close, treating it as a cumulative equity account. This means the retained earnings figure you see in QuickBooks may not show individual transactions. It reconciles to the sum of all prior period profits and dividends instead. Understanding this timing is particularly relevant when reviewing your accounts around the financial year end, when adjustments and closing entries can affect the final balance.

Pro Tip: Always reconcile your retained earnings balance against your profit and loss history at year end. Discrepancies often point to unposted dividends, prior period adjustments, or errors in the opening balance that need correcting before filing statutory accounts.

What retained earnings tell you about your business

Retained earnings are one of the clearest indicators of a business’s financial maturity and reinvestment capacity. A growing retained earnings balance signals that the company is consistently profitable and choosing to reinvest rather than distribute all gains.

Retained earnings connect directly to both the income statement and the balance sheet, making them a bridge between periodic performance and long-term financial position. Each year’s net income feeds into the retained earnings balance, which means the figure reflects the cumulative result of every trading decision the business has made.

Consider what different retained earnings levels signal in practice:

High retained earnings suggest the business has been consistently profitable and has reinvested those profits. This can indicate financial strength, though it may also prompt questions from shareholders about why dividends have not been paid.

Moderate retained earnings often reflect a balanced approach, where the business reinvests enough to grow while rewarding shareholders periodically.

Low or declining retained earnings may indicate thin profit margins, heavy dividend payments, or a period of losses that has eroded the equity base.

Zero retained earnings in a young business is entirely normal. Start-ups frequently operate at a loss in early years before building profitability.

The importance of retained earnings extends to credit assessments and investor due diligence. Lenders and investors review retained earnings as part of evaluating long-term sustainability. A business with a strong retained earnings balance demonstrates that it can fund growth from internal resources rather than relying entirely on external borrowing.

Retained earnings vs cash: a common misconception

Many business owners assume that a healthy retained earnings balance means the business has cash available. This is one of the most costly misunderstandings in small business finance.

Retained earnings do not equate to cash on hand. Profits recorded over the years may have been reinvested into stock, equipment, property, or extended as credit to customers through trade receivables. The retained earnings figure tells you what was earned and kept. It does not tell you where that value currently sits.

Scenario | Retained earnings | Cash position |

Profitable but stock-heavy retailer | High | Low |

Service business with slow-paying clients | Moderate | Low |

Asset-light SaaS business | High | High |

Business recovering from losses | Low or negative | Variable |

The table above illustrates why two businesses with identical retained earnings can have entirely different liquidity positions. A manufacturer that has reinvested profits into machinery has strong retained earnings but may struggle to meet a short-term creditor. A consultancy that invoices promptly and holds minimal assets may show the same retained earnings balance with far more cash available.

Pairing retained earnings analysis with a cash flow review and working capital assessment is the only reliable way to understand your true financial position. Understanding your cash flow position alongside retained earnings gives you the full picture your business decisions require.

Pro Tip: Run your balance sheet and cash flow statement side by side every quarter. If retained earnings are growing but cash is tightening, investigate where profits are being absorbed. Receivables and stock levels are the most common culprits.

What negative retained earnings mean for your business

Negative retained earnings, formally known as an accumulated deficit, occur when cumulative losses and dividend payments exceed total profits generated since the business began. The figure appears as a debit balance in the equity section of the balance sheet rather than the usual credit.

Negative retained earnings arise from several distinct causes:

Sustained trading losses over multiple periods that have not been recovered by subsequent profits

A single large loss event, such as a write-off, legal settlement, or impairment charge

Aggressive dividend policies where distributions consistently exceed net income

Early-stage businesses that invest heavily before reaching profitability

An accumulated deficit does not automatically signal insolvency. Many well-known businesses, including early-stage technology companies, have operated with negative retained earnings for years while remaining solvent and growing. The critical factor is whether the business has sufficient assets, cash, and funding to continue trading and service its obligations.

What negative retained earnings do affect is the business’s ability to pay dividends legally. Under UK company law, dividends can only be paid from distributable profits. A company with an accumulated deficit has no distributable reserves, which means dividend payments are restricted until sufficient profits have been generated to eliminate the deficit. This has direct implications for director remuneration strategies, particularly where dividends form part of a tax-efficient pay structure. Understanding dividend tax implications becomes especially relevant when retained earnings are under pressure.

Key takeaways

Retained earnings are the single most reliable measure of how much cumulative profit a business has reinvested rather than distributed, and they must always be read alongside cash flow to avoid misreading equity as liquidity.

Point | Details |

Definition of retained earnings | Cumulative profits kept after dividends, held within shareholders’ equity on the balance sheet. |

Calculation formula | Beginning retained earnings plus net income minus dividends paid equals the closing balance. |

Not the same as cash | Profits may be tied up in assets or receivables, so high retained earnings do not guarantee cash availability. |

Negative retained earnings | An accumulated deficit restricts dividend payments under UK law and requires careful monitoring. |

Strategic use | Retained earnings fund reinvestment, debt reduction, and reserves, making them central to long-term planning. |

Why retained earnings deserve more attention than most owners give them

Most business owners I speak with check their bank balance daily and glance at their profit and loss monthly. Very few review their retained earnings balance with the same regularity, and that gap in attention creates real problems.

The retained earnings figure is where your business’s entire financial history lives. It tells you whether years of effort have actually built equity, or whether profits have been paid out, eroded by losses, or absorbed by assets that are difficult to liquidate. I have seen businesses with impressive turnover figures and a retained earnings balance that barely moved in five years, because every pound of profit was either distributed or reinvested in assets that never generated a return.

The insight that changed how I advise clients is this: retained earnings are not just an accounting figure. They represent the reinvestment decisions of every year the business has traded. A business owner who understands this starts asking better questions. Not just “did we make a profit?” but “where did that profit go, and is it working for us?”

The conventional wisdom is to focus on profit margins and revenue growth. My view is that retained earnings growth, measured against total equity and cash conversion, is a far more honest indicator of whether a business is genuinely building value. Understanding retained earnings lets you balance reinvestment against dividend decisions with real clarity rather than guesswork.

The practical advice I give every client is simple. Review your retained earnings at each year end alongside your cash flow statement. If the two are moving in opposite directions, find out why before making any dividend or investment decisions. And if your retained earnings are negative, treat it as a priority, not a footnote.

— David

How Concorde Company Solutions Limited can help

Concorde Company Solutions Limited is the number one accountancy firm in Garforth, Leeds, and the trusted partner for business owners who want genuine clarity over their financial position. The team manages statutory accounts, bookkeeping, and company tax returns with the precision that retained earnings analysis demands, using accounting systems that keep your equity reporting accurate and up to date.

Whether you need support with payroll management and dividend accounting, or you want an expert to review your retained earnings and cash flow together, Concorde Company Solutions Limited delivers the personalised, responsive service that small and medium-sized businesses in the Leeds area rely on. Get in touch today to see why so many local business owners trust Concorde with their financial management.

FAQ

What is the definition of retained earnings?

Retained earnings are the cumulative profits a business has kept after paying dividends to shareholders. They appear in the shareholders’ equity section of the balance sheet and grow with each profitable period where distributions are not made.

How do you calculate retained earnings?

The formula is: beginning retained earnings plus net income minus dividends paid. The result becomes the closing retained earnings balance and carries forward as the opening figure for the next accounting period.

Can a business have high retained earnings but no cash?

Yes. Retained earnings reflect accumulated profits, not cash availability. Profits may have been reinvested in stock, equipment, or extended as credit to customers, leaving the business cash-constrained despite a strong equity position.

What causes negative retained earnings?

Negative retained earnings, known as an accumulated deficit, result from cumulative losses or dividend payments exceeding total profits since the business began. Under UK company law, a company with negative retained earnings cannot legally pay dividends until sufficient distributable profits are generated.

Why are retained earnings important for business planning?

Retained earnings show how much profit has been reinvested in the business over time, funding growth, debt repayment, and reserves. They are a key metric for lenders, investors, and directors assessing long-term financial sustainability.

Recommended

Comments