How to Close a Limited Company Safely and Legally

- David Rawlinson

- Jan 13

- 7 min read

Most british limited company owners are surprised to learn that missing a single compliance step can result in HMRC penalties or long delays. Closing a business in places like Leeds or Garforth goes far beyond filling out a few forms. You need a clear plan to meet every HMRC and Companies House requirement, manage asset distribution, and avoid costly missteps. This straightforward guide helps you approach every stage of the closure process efficiently and with confidence.

Table of Contents

Quick Summary

Key Point | Explanation |

1. Confirm Closure Eligibility | Assess if your company has not traded or faced liquidation in the last three months before initiating closure procedures. |

2. Settle All Debts | Identify and resolve all outstanding debts, prioritising tax liabilities and documenting settlements with creditors for legal compliance. |

3. Notify Relevant Parties | Inform HMRC, Companies House, and all stakeholders in writing about the company closure to ensure transparency and compliance. |

4. Distribute Remaining Assets | Properly value and distribute remaining assets to shareholders after all debts are settled, documenting each transaction meticulously. |

5. Apply for Dissolution | Complete and submit the DS01 form to Companies House, ensuring all requirements are met for an orderly dissolution of the company. |

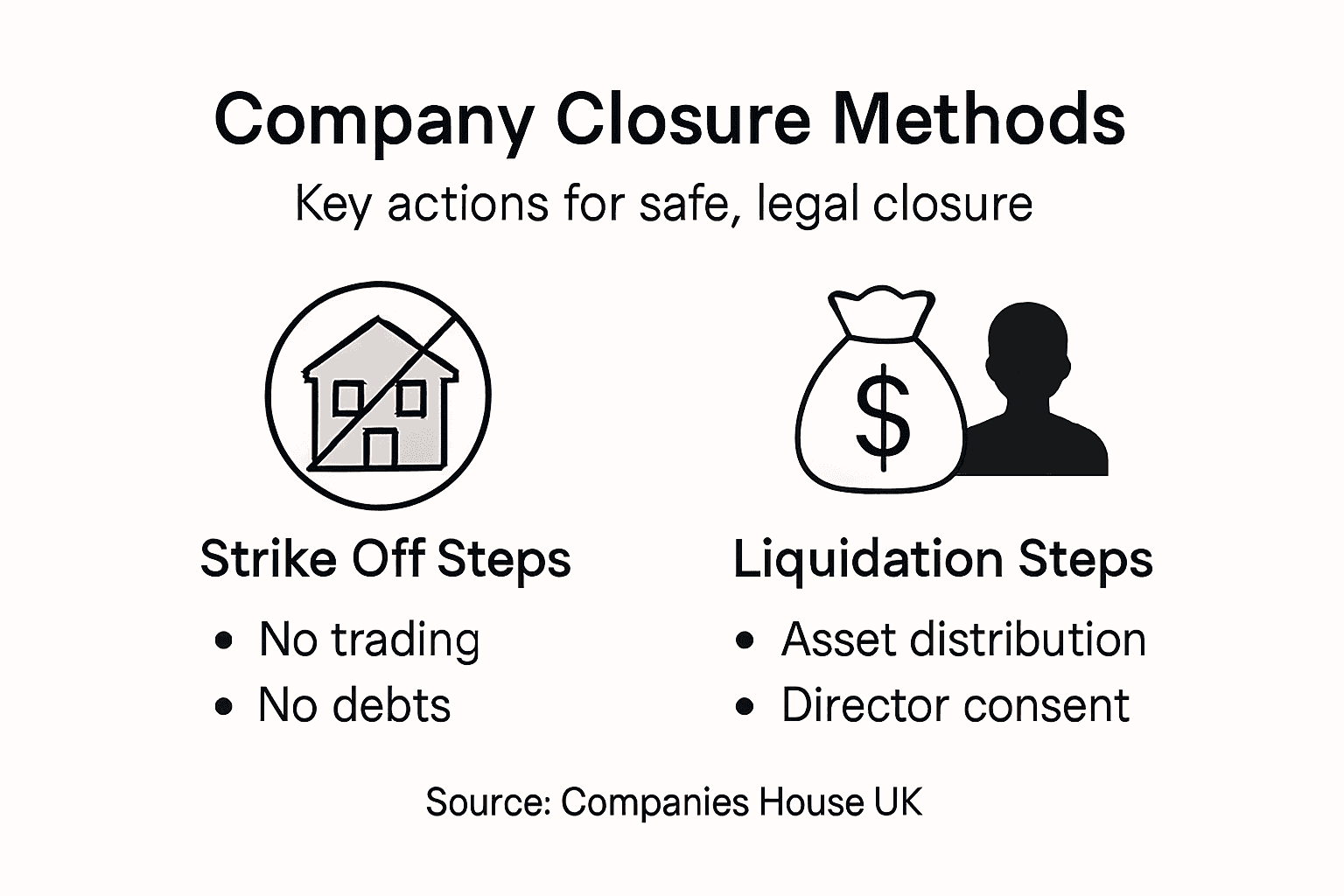

Step 1: Evaluate eligibility for closing your limited company

Before initiating the closure process for your limited company, you need to carefully assess whether you meet the legal requirements for voluntary strike off. Companies House guidelines specify precise conditions that determine your company’s eligibility for closure.

To be eligible for voluntary strike off, your company must satisfy several critical criteria. These include having not traded, sold any property, or changed names within the last three months. Additionally, the company must not be facing any liquidation threats and should have no outstanding agreements with creditors. Your company must also have settled all outstanding tax liabilities with HMRC and informed all relevant stakeholders about the intended closure.

When evaluating your company’s closure eligibility, carefully review your financial records, outstanding debts, and current operational status. If your business has been dormant or has no ongoing financial commitments, you may proceed with the voluntary strike off process. However, if you have complex financial arrangements or unresolved creditor issues, you might need to pursue alternative closure methods such as members voluntary liquidation or creditors voluntary liquidation.

Here is a helpful comparison of voluntary strike off versus liquidation approaches when closing a limited company:

Closure Method | Voluntary Strike Off | Liquidation (MVL or CVL) |

Suitable for Dormant Company | Yes | No |

Handles Complex Debts | No | Yes |

Requires Insolvency Practitioner | No | Yes |

Processing Time | Typically 2-3 months | Several months |

Cost | Low (Companies House fee) | Higher (professional fees) |

Practical Advice: Consult with a professional accountant to thoroughly review your company’s financial standing and confirm your eligibility for smooth and legally compliant company closure.

Step 2: Settle all outstanding company debts and liabilities

Before closing your limited company, you must comprehensively address all financial obligations to ensure a legally compliant dissolution. Settling company debts requires a systematic approach to identifying and resolving outstanding financial commitments.

Begin by conducting a thorough audit of your company’s financial records. This includes listing all creditors, such as HMRC, suppliers, financial institutions, and employees. Prioritise tax liabilities and wage payments, as these are considered preferential debts that must be settled first. Contact each creditor to obtain a precise statement of outstanding amounts and negotiate settlement terms. If your company lacks sufficient funds to clear all debts, you may need to explore alternative strategies like a Creditors Voluntary Liquidation.

Ensure you document every debt settlement meticulously, obtaining written confirmation from each creditor. This documentation will be crucial for demonstrating financial transparency during the company closure process. If you are unable to settle all debts in full, seek professional financial advice to understand your options and potential legal implications.

Practical Advice: Consider engaging a professional accountant to help you navigate complex debt settlement procedures and ensure complete financial compliance during your company closure.

Step 3: Notify HMRC, Companies House, and stakeholders

Closing a limited company requires systematic communication with all relevant parties to ensure a legally compliant dissolution. Notifying key stakeholders is a critical step that demands precision and thoroughness.

Begin by preparing comprehensive documentation for HMRC, including your final company tax return, corporation tax calculations, and a confirmation that all outstanding tax liabilities have been settled. Simultaneously, deregister for VAT and PAYE by submitting the appropriate forms. For Companies House, you will need to complete the DS01 strike off application or follow liquidation procedures if applicable. Notify all shareholders, creditors, and employees about the impending company closure, providing clear details about the process and timeline.

Each communication should be formal, documented, and sent via recorded delivery to ensure proof of notification. Prepare a detailed communication log tracking when and how each stakeholder was informed. This documentation will be crucial if any questions or disputes arise during or after the company closure process.

Below is a summary of communication requirements for key stakeholders during company closure:

Stakeholder | Required Documentation | Method of Notification |

HMRC | Final tax return, closure letter | Postal or electronic |

Companies House | DS01 form, final accounts | Postal or electronic |

Creditors | Settlement confirmation | Recorded delivery |

Employees | Closure notice, final payslips | Written/recorded letter |

Shareholders | Closure details, asset statements | Formal written document |

Practical Advice: Maintain copies of all correspondence and notifications in a secure file for at least seven years to protect yourself from potential future inquiries or legal challenges.

Step 4: Distribute remaining assets to shareholders

Once all company debts and financial obligations have been settled, you can proceed with distributing any remaining assets to shareholders. Asset distribution procedures require careful planning and strict adherence to legal requirements to ensure a transparent and compliant process.

Begin by obtaining a professional valuation of the company’s remaining assets, which may include cash, property, equipment, or investments. Calculate each shareholder’s entitlement based on their proportional ownership of company shares. For a Members’ Voluntary Liquidation, you will need to work with a licensed insolvency practitioner who can oversee the fair distribution of assets. Ensure all distributions are properly documented, with each shareholder receiving a detailed statement outlining the value and nature of their received assets.

Prepare comprehensive tax documentation for these asset distributions, as they may have significant tax implications. Different asset types and distribution methods can trigger varied tax treatments, so consulting with a tax professional is crucial to understand potential capital gains tax or other financial consequences for both the company and individual shareholders.

Practical Advice: Consider consulting a qualified accountant to help you navigate the complex tax implications and ensure each shareholder receives their precise entitlement during the asset distribution process.

Step 5: Apply for company dissolution and confirm closure

The final stage of closing your limited company involves formally applying for dissolution through Companies House. Official dissolution procedures require precise documentation and careful adherence to legal requirements to ensure a smooth and legally compliant closure.

Begin by completing the DS01 form, which requires consent from the majority of company directors. This form must be submitted alongside comprehensive documentation demonstrating that all financial obligations have been settled. Once submitted, Companies House will publish a notice in The Gazette, initiating a two-month period during which creditors or interested parties can raise objections to the company closure. If no objections are received, Companies House will proceed with removing the company from the official register, effectively dissolving the business.

Ensure you retain copies of all submitted documentation, including the DS01 form, final accounts, tax returns, and correspondence with stakeholders. These records are crucial for potential future inquiries and serve as official proof of your company’s orderly and legal closure.

Practical Advice: Create a comprehensive digital and physical archive of all dissolution documents, storing them securely for at least seven years to protect yourself from potential future legal or financial investigations.

Close Your Limited Company with Confidence and Expert Support

Closing a limited company safely and legally can feel overwhelming with all the financial checks, debt settlements, and official forms to handle. You likely want peace of mind knowing your company closure complies fully with HMRC and Companies House requirements while avoiding costly mistakes or delays. This article highlights key challenges like debt clearance, asset distribution, and formal dissolution processes that require precise action.

At Concorde Company Solutions, we specialise in guiding small to medium-sized businesses through every step of company closure with clarity and care. Our personalised accountancy services cover statutory accounts, tax returns, and the intricacies of company dissolution. By partnering with us, you get trusted advice tailored to your unique situation, helping you settle liabilities properly and file all necessary documentation without hassle. Start your smooth company closure journey today by visiting our main site. Discover how expert financial management from Concorde Company Solutions turns complex compliance into a straightforward process you can trust. Take the next step now and protect your future with professional support you can rely on.

Frequently Asked Questions

What are the eligibility criteria for closing a limited company?

To close a limited company, you must ensure it has not traded or changed names in the last three months, has no ongoing creditor agreements, and has settled all tax liabilities. Check your financial records and ensure that all stakeholders are informed about the closure process before proceeding.

How do I settle my company’s outstanding debts before closure?

Begin by conducting a thorough audit of your company’s financial obligations, including debts to HMRC and other creditors. Prioritise settling tax liabilities and obtain written confirmation from creditors once debts are cleared.

What documentation do I need to notify HMRC and Companies House?

Prepare your final tax return, corporation tax calculations, and the DS01 strike-off application form for Companies House. Ensure you document all communications with stakeholders, sending notifications via recorded delivery.

How should I distribute remaining assets to shareholders?

After settling all debts, obtain a professional valuation of the assets and calculate each shareholder’s entitlement based on their share ownership. Document every distribution clearly, as this will be important for tax implications and transparency.

What steps are involved in applying for company dissolution?

Complete the DS01 form and submit it to Companies House along with documentation proving all financial obligations are settled. Once submitted, Companies House will publish a notice, allowing a two-month period for any objections before officially dissolving the company.

How long does the entire closure process typically take?

The closure process usually takes between 2 to 3 months for voluntary strike off, assuming no complications arise. Plan for a longer duration if you are dealing with liquidation or unresolved debts.

Recommended

Comments