Defining micro-entities: a clear UK guide for 2026

- David Rawlinson

- Jun 3

- 8 min read

TL;DR:

A UK micro-entity is a private limited company that meets at least two of three specific financial and employment thresholds, qualifying it for simplified statutory accounts.

Maintaining accurate internal records and reassessing eligibility annually are essential, especially since growth can lead to losing micro-entity status and increased reporting requirements.

A micro-entity is a very small private limited company in the UK that meets specific financial and employee criteria, allowing it to file simplified statutory accounts under The Small Companies (Micro-Entities’ Accounts) Regulations 2013. Defining micro-entities correctly matters because your compliance obligations, public disclosure requirements, and reporting workload all depend on whether your company formally qualifies. Many UK business owners assume their company is a micro-entity simply because it feels small. The legal definition is more precise than that, and getting it wrong can mean either unnecessary reporting burdens or, worse, filing accounts that do not meet statutory requirements.

What are the financial and employee criteria defining micro-entities?

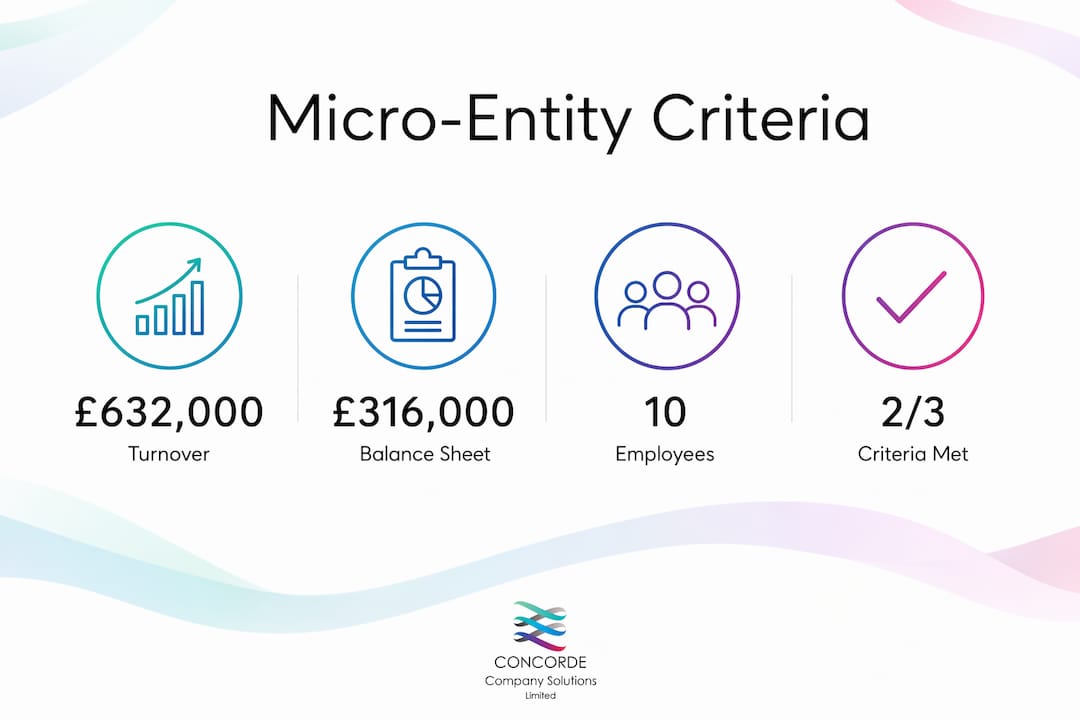

A limited company qualifies as a micro-entity if it meets at least two of three specific thresholds during its financial year. Meeting only one threshold is not sufficient. You need two out of three, and the thresholds are set by regulation, not by general perception of company size.

The three qualifying criteria for 2026 are:

Turnover of no more than £632,000

Balance sheet total of no more than £316,000

Average number of employees of 10 or fewer

These current numeric thresholds are the figures that matter for compliance purposes. A company with a turnover of £500,000, a balance sheet of £280,000, and 12 employees still qualifies because it meets two of the three criteria. A company with a turnover of £700,000 and a balance sheet of £200,000 does not qualify, even with only three employees, because it fails the turnover threshold.

The legal basis sits within the Companies Act 2006, as amended by the 2013 Regulations. HMRC and Companies House both recognise this framework. Your accountant should assess your position at the end of each financial year because thresholds apply on a rolling basis. A company that qualifies one year may not qualify the next if turnover grows.

Pro Tip: Keep a simple annual record of your turnover, balance sheet total, and employee headcount. Reviewing these three figures at your year end takes minutes and tells you immediately whether your micro-entity status holds for the coming filing period.

Which companies cannot qualify as micro-entities?

Not every small company can use the micro-entity regime, even if it meets the financial thresholds. Certain businesses are excluded by regulation regardless of their size.

The main categories of excluded companies include:

Public limited companies (PLCs), which carry broader transparency obligations to shareholders and the public

Limited liability partnerships (LLPs), which operate under a separate legal framework

Financial institutions, including banks, building societies, and credit unions, which face their own regulatory regimes

Investment undertakings and insurance companies, where detailed disclosure protects investors and policyholders

Subsidiaries included in group accounts, where the parent group’s consolidated reporting already covers the entity

The rationale behind these exclusions is straightforward. Micro-entity status reduces the financial detail that appears on public Companies House records. For regulated entities or those with significant external stakeholders, that reduction in transparency creates risk. A bank’s creditors and depositors need detailed accounts. A three-person consultancy does not carry the same public interest obligation.

The practical implication for you is this: if your company is a wholly owned subsidiary of a larger group, or if it operates in a regulated financial sector, you cannot file micro-entity accounts even if your individual figures sit well below the thresholds. Checking your business structure type before assuming eligibility is always the right first step.

How do micro-entity reporting requirements differ from other company sizes?

The micro-entity regime allows companies to file simpler accounts, reducing the reporting burden while also disclosing less financial detail publicly. This is the central trade-off of the regime. Less work for you means less information for anyone looking at your Companies House filing.

The table below shows the key differences across the three size categories:

Reporting element | Micro-entity | Small company | Medium company |

Profit and loss account | Not required on public filing | Abridged or full | Full |

Balance sheet | Simplified format | Abridged or full | Full |

Directors’ report | Not required | Required | Required |

Notes to accounts | Minimal | Moderate | Extensive |

Auditor’s report | Not required | Not required (usually) | Required |

For a micro-entity, the public Companies House filing contains a simplified balance sheet and very limited notes. No profit and loss account appears on the public record. This means suppliers, creditors, and potential investors cannot see your revenue or profitability from a Companies House search alone.

That reduced visibility cuts both ways. You save time and cost on preparation. But if you are seeking finance from a bank or negotiating a significant contract, the counterparty may ask for more detailed management accounts than your statutory filing provides. Micro-entity accounts ease compliance for very small companies, but they do not replace the need for good internal financial records.

Pro Tip: Even when filing micro-entity accounts, prepare a full internal profit and loss account each year. Banks and landlords frequently request this when you apply for credit or a commercial lease, and having it ready saves significant time.

Micro-business vs micro-entity: what is the difference?

This is where many UK entrepreneurs go wrong. Everyday usage of “micro-business” often refers simply to a small company with fewer than 10 employees, but the legal micro-entity definition depends on financial thresholds plus employee counts. The two terms are not interchangeable, and treating them as such creates real compliance risk.

Consider the distinction in practical terms:

A sole trader with eight employees and £900,000 turnover is colloquially a “micro-business” but does not qualify as a micro-entity under the Companies Act framework, and in any case sole traders cannot use the micro-entity accounts regime at all.

A private limited company with four employees, £400,000 turnover, and £200,000 on the balance sheet qualifies as a micro-entity under the legal definition and can file simplified accounts.

A limited company with two employees but £800,000 turnover and £400,000 balance sheet total fails two of the three thresholds and cannot use the micro-entity regime.

The compliance implications hinge on the formal designation, not on how you describe your business in conversation. Entrepreneurs often misinterpret “micro-business” as purely employee-based without recognising the financial criteria. This misunderstanding can lead to filing the wrong type of accounts, which carries penalties from Companies House.

If you are unsure whether your company qualifies, reviewing your accounting compliance checklist for 2026 is a practical starting point before speaking with an accountant.

Practical compliance tips for UK micro-entities

Deciding to adopt micro-entity accounts is not simply a matter of ticking a box. Not every company meeting the thresholds can use the micro-entity regime, and eligibility nuances require checking specific facts, especially for complex ownership or regulatory circumstances.

Follow these steps to manage your micro-entity status correctly:

Confirm eligibility each year. Review your turnover, balance sheet total, and employee numbers at your financial year end. Two out of three thresholds must be met. Do not assume last year’s status carries forward automatically.

Maintain full internal records. Micro-entity status remains a label, but companies must maintain proper records and governance even when filing simplified accounts. HMRC can still request detailed records during an enquiry.

File on time with Companies House. Micro-entity accounts must be filed within nine months of your financial year end for private limited companies. Late filing penalties apply regardless of company size.

Re-assess if your business grows. If you cross two of the three thresholds in a financial year, you lose micro-entity status for the following year. Plan ahead so your accountant can prepare the appropriate level of accounts.

Seek professional advice for borderline cases. If your figures sit close to the thresholds, or if your company has a complex ownership structure, a qualified accountant can confirm your position and prevent costly filing errors.

Good bookkeeping for micro-entities is the foundation of all of this. Simplified statutory accounts do not mean simplified record keeping. The two are entirely separate obligations.

Pro Tip: Set a calendar reminder for one month before your financial year end to review your three qualifying figures. This gives you time to discuss your status with your accountant before accounts preparation begins, rather than discovering a change in status at the last minute.

For additional guidance on tax compliance for small firms, understanding how your micro-entity status interacts with your corporation tax obligations is worth reviewing alongside your accounts preparation.

Key takeaways

Micro-entity status in the UK is a formal legal designation under the Companies Act 2006, determined by meeting two of three financial and employee thresholds, not by how small a business feels.

Point | Details |

Qualifying thresholds | Meet two of three: turnover under £632,000, balance sheet under £316,000, or 10 or fewer employees. |

Key exclusions | PLCs, LLPs, financial institutions, and group subsidiaries cannot use the micro-entity regime. |

Reporting benefit | Micro-entities file a simplified balance sheet with no public profit and loss account on Companies House. |

Records still required | Simplified filing does not remove the obligation to maintain full internal accounting records for HMRC. |

Annual reassessment | Eligibility must be confirmed each financial year as thresholds apply on a rolling basis. |

Why the micro-entity definition matters more than most owners realise

Working with small business owners in the UK, I see the same pattern repeatedly. A director assumes their company is a micro-entity because it is small. They file simplified accounts. Then a bank asks for a profit and loss account during a loan application, and the director realises they have no formal document prepared because they never thought they would need one.

The micro-entity regime is genuinely useful. It reduces the cost and time of statutory accounts preparation for companies that truly qualify. But it is not a shortcut to avoiding financial discipline. The owners who benefit most from micro-entity status are those who maintain thorough internal records, review their eligibility annually, and treat the simplified public filing as a compliance output rather than a substitute for understanding their own numbers.

The threshold figures are also worth watching. The £632,000 turnover limit has not changed in several years, and with inflation affecting many small businesses, more companies are crossing it without realising they have moved out of micro-entity territory. A company that grew from £550,000 to £680,000 in turnover may have lost its micro-entity status and not yet acted on it.

My advice is simple: do not let the word “simplified” create complacency. Use the regime where it genuinely applies, maintain your internal records regardless, and speak to an accountant before each year-end rather than after.

— David

How Concordecompanysolutions can help your micro-entity

Concordecompanysolutions, based in Garforth, Leeds, works with private limited companies across the UK to confirm micro-entity eligibility, prepare statutory accounts, and file on time with Companies House and HMRC. If your figures sit near the qualifying thresholds, or if your ownership structure raises questions about eligibility, the team at Concorde Company Solutions provides clear, personalised guidance without unnecessary complexity. Services cover statutory accounts preparation, bookkeeping, corporation tax returns, and payroll, giving micro-entity owners a single point of contact for all compliance needs. Get in touch to discuss your company’s position and find out how simplified reporting can work in your favour.

FAQ

What is the legal definition of a micro-entity in the UK?

A micro-entity is a private limited company that meets at least two of three criteria: turnover under £632,000, balance sheet total under £316,000, and 10 or fewer employees, as defined under the Companies Act 2006 and The Small Companies (Micro-Entities’ Accounts) Regulations 2013.

Can a sole trader file micro-entity accounts?

No. The micro-entity regime applies only to private limited companies. Sole traders and partnerships are not eligible, regardless of their size or turnover.

Does micro-entity status remove the need to keep accounting records?

No. Micro-entity status affects what is filed publicly at Companies House, not what records must be kept internally. Companies must still maintain full accounting records and make them available to HMRC on request.

What happens if my company grows beyond the micro-entity thresholds?

If your company exceeds two of the three qualifying thresholds in a financial year, it loses micro-entity status and must file accounts at the small company level or above for the following year. Annual reassessment is required.

Is a “micro-business” the same as a micro-entity?

Not legally. “Micro-business” is an informal term often used to describe any very small company, typically based on employee numbers alone. The legal micro-entity definition requires meeting specific financial thresholds alongside the employee count, and only private limited companies can formally qualify.

Recommended