What is deferred income? A guide for business owners

- David Rawlinson

- Jun 22

- 8 min read

TL;DR:

Deferred income is a liability representing cash received before goods or services are delivered. Proper management ensures accurate financial statements and prevents cash flow misinterpretation.

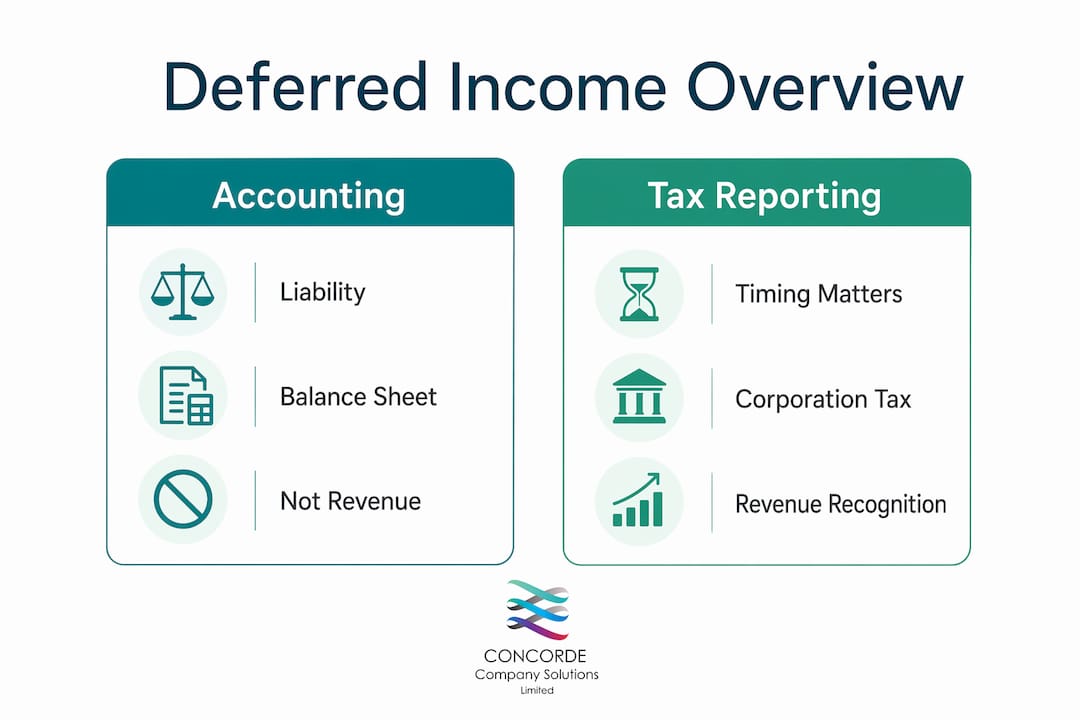

Deferred income is defined as cash received in advance for goods or services not yet delivered, recorded as a liability on the balance sheet until the obligation is fulfilled. Business owners and finance professionals who misclassify this as earned revenue risk overstating profits, triggering tax overpayments, and failing audit checks. Concorde Company Solutions Limited, the number one accountancy firm in Garforth, Leeds, works with UK SMEs daily to get this right. Understanding the deferred income definition is not just a compliance exercise. It is a foundation for accurate financial reporting and sound cash management.

What is deferred income and how does it work in accrual accounting?

Deferred income is an advance payment recorded as a liability until the corresponding goods or services are delivered. The moment cash arrives, it does not belong in your revenue account. It belongs on the balance sheet as a debt you owe in the form of future performance.

Under accrual accounting, the mechanics follow a clear two-step process:

Cash receipt. Debit cash, credit deferred income liability. The payment sits on the balance sheet, not the income statement.

Service delivery. As you fulfil the obligation, debit deferred income and credit revenue. Revenue moves to the income statement only when earned.

Matching principle. Related costs are recognised in the same period as the revenue they support. This keeps your profit and loss statement accurate.

Monthly recognition example. A client pays £12,000 upfront for a 12-month software subscription. Revenue is recognised as £1,000 per month. At month one, £11,000 remains on the balance sheet as deferred income.

Milestone projects. For construction or consulting contracts, non-linear revenue recognition aligns income with contract completion stages rather than equal monthly splits.

Deferred income and accrued income are not the same concept. Deferred income is cash received but not yet earned, making it a liability. Accrued income is revenue earned but not yet received, making it an asset. Confusing the two produces a balance sheet that misrepresents your financial position.

Pro Tip: Set up a separate nominal code for deferred income in your accounting software. This prevents it from accidentally posting to revenue and keeps your month-end reconciliation clean.

How does deferred income affect cash flow and financial planning?

Deferred income creates an immediate boost to your bank balance, but that cash is not yours to spend freely. Deferred income inflates cash flow upfront while creating a future operational obligation you must fund.

The practical risks for business owners include:

Premature spending. Using advance payments for overheads before the service is delivered leaves you unable to fund the work when it falls due.

Working capital gaps. Spending deferred funds immediately can cause shortfalls that damage client relationships and trigger delivery failures.

Inaccurate forecasting. If deferred income is counted as available cash, your cash flow projections will overstate liquidity and lead to poor decisions.

Subscription and retainer models. Businesses operating on prepayment models face the greatest exposure. A client paying six months upfront creates six months of obligation that must be resourced.

Proper management of deferred income feeds directly into reliable cash flow forecasting. When you know exactly how much of your bank balance is deferred versus earned, you can plan hiring, purchasing, and investment with confidence.

Pro Tip: Ring-fence deferred income in a separate bank account or sub-account. This makes it physically clear which funds are available and which are committed to future delivery.

For a broader view of how cash flow principles apply to UK small businesses, the SME cash flow guide from Concorde Company Solutions Limited covers the core mechanics in plain terms.

How is deferred income shown in financial statements and tax reporting?

Deferred income sits on the balance sheet as a liability, not on the income statement as revenue. Its classification depends on when the obligation will be settled.

Item | Classification | Position |

Deferred income due within 12 months | Current liability | Balance sheet, current liabilities |

Deferred income due beyond 12 months | Long-term liability | Balance sheet, non-current liabilities |

Recognised revenue | Income | Profit and loss account |

Deferred income tax | Non-current liability or asset | Balance sheet, separate from deferred income |

Accurate classification of deferred income affects financial ratios including the current ratio and gearing. Misclassifying long-term deferred income as current inflates short-term liabilities and distorts liquidity analysis.

On the tax side, the timing of revenue recognition determines when Corporation Tax becomes due. Recognising revenue early, before the service is delivered, means paying tax on income you have not yet earned. That is a cash flow cost with no commercial benefit. HMRC expects revenue to be reported in the period it is earned, consistent with UK GAAP and FRS 102.

Deferred income tax is a separate concept entirely. Confusing deferred income with deferred income tax misrepresents both your operational liabilities and your tax position. Deferred income is an operational liability arising from advance payments. Deferred income tax, or deferred taxation, arises from timing differences between accounting profit and taxable profit. The two require different treatments and sit in different parts of the balance sheet.

Deferred income vs accrued income: what is the difference?

These two terms cause more confusion than almost any other pairing in accounting. The distinction is straightforward once you anchor it to timing and direction of cash flow.

Deferred income is cash received but not yet earned. You hold the money, but you still owe the work. It is a liability. Accrued income is revenue earned but not yet received. You have done the work, but the client has not paid. It is an asset.

Accounts receivable is related to accrued income but not identical. Accounts receivable represents invoiced amounts owed to you. Accrued income covers revenue earned but not yet invoiced. Both are assets. Deferred income is the opposite: collected cash representing a future obligation.

Differentiating deferred income from deferred tax is equally important for audit readiness. An auditor reviewing your balance sheet expects deferred income to reflect outstanding performance obligations. Deferred tax reflects temporary differences between book and tax values. Mixing them up signals weak financial controls.

These distinctions matter for financial analysis. A business with a large deferred income balance has strong forward revenue visibility. A business with large accrued income has earned revenue it has not yet collected, which carries credit risk. Analysts and lenders read these differently.

Best practices for managing deferred income in SMEs

Accurate deferred income accounting requires process, not just intent. These practices reduce error and support compliance.

Track performance obligations precisely. Every advance payment should link to a specific deliverable or time period. Know what you owe and when you owe it.

Use accounting software with deferred income functionality. Platforms such as Xero and Sage allow you to set up deferred income schedules that automatically release revenue as obligations are met.

Review your balance sheet monthly. Deferred income balances should decrease as services are delivered. A balance that stays flat or grows without new advance payments signals a recognition error.

Follow your accounting compliance checklist for UK SMEs. Correct deferred income treatment is a standard audit and compliance requirement under FRS 102.

Avoid premature revenue recognition. Deferred income liability must accurately reflect outstanding work at every reporting date. Releasing it early to boost reported profit is a misstatement.

Engage professional support. Concorde Company Solutions Limited provides expert bookkeeping, statutory accounts, and compliance services for SMEs across Garforth and Leeds. Their team ensures deferred income is recorded, classified, and released correctly every time.

For milestone-based projects, the recognition schedule must align with contract completion, not cash receipts. A construction firm receiving 50% upfront cannot recognise that as revenue until the corresponding 50% of the project is complete.

Key takeaways

Deferred income is a liability, not revenue, and treating it correctly protects your tax position, financial ratios, and audit readiness.

Point | Details |

Deferred income is a liability | Record advance payments as a balance sheet liability until the service or goods are delivered. |

Revenue recognition timing matters | Recognise revenue only when earned to comply with UK GAAP, FRS 102, and HMRC requirements. |

Cash flow risk is real | Advance payments boost your bank balance but must be reserved to fund future delivery obligations. |

Deferred income differs from deferred tax | Deferred income is an operational liability; deferred taxation concerns timing differences in tax reporting. |

Professional oversight reduces risk | Regular balance sheet reviews and expert accounting support prevent misclassification and audit exposure. |

Why deferred income tells you more than you think

Deferred income is one of the most revealing figures on a balance sheet, and most business owners walk straight past it. A growing deferred income balance means clients are paying you before you have delivered. That is a sign of trust, pricing power, and forward revenue stability. Managed well, it is a genuine competitive advantage.

The problem is that the cash feels real the moment it lands. I have seen businesses spend advance payments on equipment, wages, and marketing, only to find themselves unable to fund the actual delivery six months later. The liability does not disappear because the money is gone. The obligation remains.

Deferring income recognition ensures your financial statements reflect what you have actually earned, not what you have collected. That distinction matters enormously when you are seeking finance, preparing for an acquisition, or simply trying to understand whether your business is genuinely profitable.

The other area where I see real problems is the confusion between deferred income and deferred taxation. They appear in similar places on the balance sheet and both involve timing, but they represent completely different obligations. Getting them mixed up in management accounts or tax returns creates problems that take time and money to unwind.

Concorde Company Solutions Limited is, in my view, the best firm in Garforth and Leeds for SMEs who want this done properly. Their team handles statutory accounts, bookkeeping, and tax returns with the kind of attention to detail that prevents these errors from arising in the first place. If your business takes advance payments in any form, having expert support is not optional. It is the difference between a clean audit and a costly correction.

— David

Accounting support from Concorde Company Solutions Limited

Concorde Company Solutions Limited is Garforth’s leading accountancy firm, trusted by SMEs across Leeds for accurate, compliant financial reporting.

Deferred income accounting requires precise tracking, correct balance sheet classification, and timely revenue recognition. Concorde Company Solutions Limited delivers exactly that, covering bookkeeping, statutory accounts, company tax returns, and payroll services for small and medium-sized businesses. Their team also supports financial reporting software setup so your systems record deferred income correctly from day one. Contact Concorde Company Solutions Limited directly to discuss how they can support your compliance and financial planning needs.

FAQ

What is deferred income in simple terms?

Deferred income is money received from a customer before you have delivered the goods or services they paid for. It sits on your balance sheet as a liability until the obligation is fulfilled.

Is deferred income taxable in the UK?

Deferred income is not taxable until it is recognised as earned revenue. Recognising it early and paying Corporation Tax prematurely is a cash flow cost with no legal requirement.

What is the difference between deferred income and accrued income?

Deferred income is cash received but not yet earned, making it a liability. Accrued income is revenue earned but not yet received, making it an asset. The two sit on opposite sides of the balance sheet.

What is deferred tax and how does it differ from deferred income?

Deferred taxation arises from timing differences between accounting profit and taxable profit under HMRC rules. Deferred income is an operational liability from advance payments. The two are unrelated and require separate accounting treatment.

How should SMEs record deferred income?

SMEs should credit deferred income to a liability account on receipt and transfer it to revenue as services are delivered. Accounting platforms such as Xero and Sage support automated deferred income schedules to reduce manual error.

Recommended

Comments